Life and times of K

When the Covid-19 pandemic shocked the global economy back in the first quarter, there was a lot of discussion as to what the shape of the eventual recovery would be.

Commentators debated whether it would be a quick V-shaped bounce, a dragged-out U-shape, or a W caused by a second wave of infections. While there have been second waves in several countries, including the US, Australia and Spain, resulting in the re-imposition of some restrictions, a return to the hard nationwide lockdowns we saw early on seems unlikely.

Doctors now know much more about how to treat the disease, and it is quite frankly hard to imagine people accepting it. A global double-dip W seems unlikely. Finally, there is the dreaded L-shaped recovery, which does not really count as a recovery at all, since there is no return to previous levels of economic activity.

Where we are now, there is evidence of all these types of recoveries, depending where you look. In other words, both the economic recovery and market reaction have diverged across sectors, regions and countries as well as individual firms and households.

Therefore, it is the K-shaped recovery that is being discussed more and more. It reflects a cycle where the winners keep winning, and the losers keep losing. In other words, it indicates a deepening inequality.

Some of this reflects pre-existing trends now put on steroids. Some of it is a complete break from the past in our new reality. Some of it can reverse when vaccines and effective treatments become widely available. Some of these changes might be permanent.

Inequality might be a natural outcome of capitalist economies, but that doesn’t mean it’s an outcome everyone accepts or should accept. The question then moves into political terrain, whether it is struggling industries lobbying for protective tariffs, workers pushing for greater benefits or the have-nots agitating for a stronger safety net.

The winners are increasingly looking very conspicuous in an unequal world, and all but inviting a backlash. The divergence between the stock market and the economy in many countries has been striking and widely discussed. In the case of the US, the S&P 500 hit new records last week even as another one million Americans joined the ranks of the unemployed. Less widely discussed is that only slightly more than half of Americans are invested in the stock market, according to Gallup polls. Federal Reserve data, meanwhile, shows that the top 10% of the income distribution owns 87% of outstanding shares. It is the rich who have benefited from the rally, while the poor and even many middle-class families have seen no benefit or experienced financial setbacks.

Amazon founder Jeff Bezos last week became the first person worth $200 billion (just about enough to cover the South African government’s outstanding debt). Even before the pandemic, the likes of Amazon, Facebook and Google were being viewed as unhealthy monopolies in some quarters, with increasing pressure on the US government to regulate them, or even break them apart, as was done with Rockefeller’s Standard Oil in 1911. These calls are likely to grow.

As if on cue, one of the Standard Oil successor companies, ExxonMobil, fell out of the Dow Jones Index last week, having been a member since 1928. In the broader S&P 500 index, the weighting of energy companies has shrunk to less than 2.5%, making it the smallest of the 11 subsectors. It was 13% in 2011.

Commodities with a K

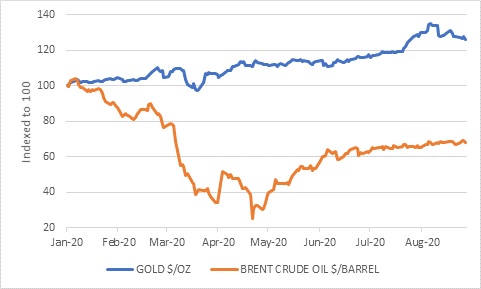

This of course reflects another widely discussed divergence within commodity markets. The energy complex (oil, coal, gas) is still trading well below pre-pandemic levels, while gold is near record highs. Industrial metals such as iron ore, copper and platinum are somewhere in between, which is somewhat surprising given that global industrial activity has not fully recovered yet. When it comes to commodities, low prices normally lead to high-cost producers falling out, eventually limiting supply. Similarly, high prices encourage new supply. The demand and supply cycles often lag each other by several years, leading to pronounced price cycles. However, if the shift towards renewable energy accelerates (as it must if we are serious about dealing with the climate crisis), oil and coal demand might end up permanently impaired in the coming years.

Chart 1: The K in commodity markets – gold and oil

Source: Refinitiv Datastream

Below are further examples of the K-shape, starting with global equities. By now it is well known that the biggest winners on equity markets in the pandemic era (and before) have been the five biggest companies in the world by market value: Apple, Amazon, Microsoft, Alphabet (Google) and Facebook. These can all be described as technology platform companies, meaning that as big as they are now, they can potentially leverage their enormous user base even further. They are also companies that facilitate people playing, working and shopping at home, and have therefore benefited from the pandemic. The divergence between their share prices on the one hand, and airlines, hospitality companies and operators of shopping malls on the other hand, is stark.

Also notable is that they are all US companies, and it is no surprise that comparing the US market with many other countries also looks like a K. This is a pre-pandemic trend dating to the end of the 2008 Global Financial Crisis, but has now been pushed to an extreme. Goldman Sachs estimates that the performance of European stocks relative to US is now at the lowest level since 1919.

Could this be a repeat of the tech bubble of the 1990s? There might be some element of speculative frenzy, particularly with a new breed of day trader lured to the market by the loss of casinos and sports betting as forms of entertainment. However, unlike in 2000, these are real companies with real profits, and investor enthusiasm is centred on these very specific business models, not just anything with .com in its name. These companies can grow their earnings even while economic growth is soggy, Most other companies, especially ‘value’ stocks, depend on a strong economy to grow earnings and therefore have been less profitable.

The divergence in profitability between US and non-US companies and tech and non-tech sectors is also notable. It becomes even more important in this age of near-zero nominal interest rates and negative real interest rates (whereas real interest rates in the 1990s were positive and quite high).

Philips curve flattened

Rates are not going higher anytime soon. In what is likely to be viewed in coming years as a pivotal moment in the history of central banking, Federal Reserve chair Jerome Powell announced that the Fed would shift its target from 2% inflation to an average of 2% over time.

While this might sound too subtle a change for anyone but die-hard market geeks, what it implies is that interest rates will remain lower for longer. Since inflation has long been below 2%, the Fed will have to tolerate inflation above 2% to raise the average. It will not hike rates at the first sign of inflation or falling unemployment, and has now given up the so-called Philips Curve, the idea that low unemployment would lead to higher inflation. Powell explicitly tied this back to inequality, noting the importance of a strong labour market to deliver meaningful benefits to lower income households and racial minorities. The goal now is not just low unemployment, but a ‘broad-based and inclusive’ recovery.

Not mentioned, of course, is that if the Fed has so far failed to get inflation to 2%, there is no reason to believe it will succeed in getting inflation above 2%. It will not stop trying however, but this causes another form of inequality: conservative savers in low-risk money market and bank products are all but guaranteed to lose wealth in real terms. The equity market, meanwhile, is flying.

Gini in the bottle

Locally, we are unfortunately very familiar with inequality. Indeed, we have the highest level of income inequality among sizable economies as measured by the Gini coefficient, while wealth (asset) inequality is equally stark. There are plenty of factors that could worsen this situation. Skilled white-collar workers who can work from home can still earn a salary. Those who work in service sectors dependent on movement and face-to-face contact (waiters, shop assistants, hairdressers) have taken a huge blow. The toll is even worse on informal service providers such as car guards and hawkers. While these sectors are now recovering, if haltingly, international tourists seem unlikely to return to South Africa this year. A whole industry remains on its knees, and with it thousands of unskilled and semi-skilled jobs are being lost.

The full political and social implications remain to be seen. The recent uproar over corruption might well be linked to the increasing hardships of ordinary South Africans.

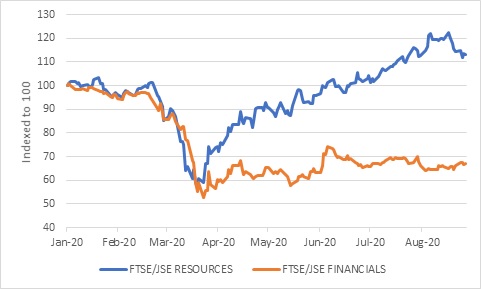

Chart 2: The K on the JSE – resources and financials

Source: Refinitiv Datastream

We have a similar divergence between the depressed economy and a reasonably robust stock market, though the JSE is nowhere near as perky as its American counterpart. Domestically focused companies (banks, insurers, REITs, construction firms) form the bottom leg of the K. Sasol also sits there, having experienced pretty much everything that could go wrong with a company this year, including a hurricane barrelling down on its new plant in Louisiana. The top leg of the K is comprised of the rand hedges, including Naspers and the mining companies.

As noted above, one saving grace for South Africa is that our main export commodity prices are doing quite well. Another is that our agricultural sector is recovering from last year’s drought conditions, with 2020 crop estimates well above 2019 levels for maize and wheat and several other smaller crops. Both mining and farming are plagued by policy uncertainty, which in turn is a consequence of politicians struggling to decide how best to address the unequal ownership patterns in these two sectors. But if they are to thrive and lead the recovery, a way forward has to be found to encourage investment.

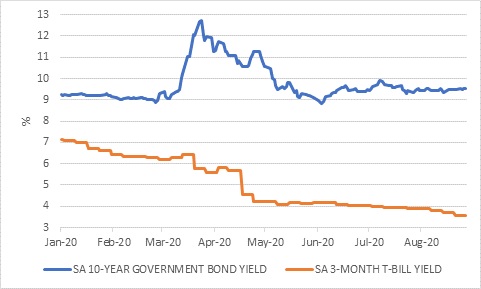

Chart 3: The K in local fixed income — Long- and short-term yields

Source: Refinitiv Datastream

A final, persistent K worth mentioning is the bond market. In the local market, long-term government bond yields remain elevated as the market focuses on fiscal risks, while short-term yields have declined due to Reserve Bank interest rate cuts. Local investors need to decide where on the K they want their fixed interest exposure. Inflation is not a concern for the bond market. Though it ticked up in the latest reading to 3.2%, consumer inflation is still likely to remain near the bottom end of the Reserve Bank’s 3% to 6% target for some time. It might even cut rates again, dragging the bottom leg of the K even lower.

Looking across countries, there is also a K shape. Other emerging markets have seen their bond yields decline. Ours remain sticky.

Investing in a world of K

A world with so much diverges (and there are many more examples we don’t have space to mention) creates challenges for investors. The first is to work out whether the deviation in each case is structural and likely to persist, or cyclical and subject to mean reversion. The second challenge is then to work out what other investors think. In other words, what kind of future is being priced in? Even a great company can turn out to be a lousy investment if you pay too much for its shares. Similarly, a lousy company can be a great investment if its shares are bought cheaply and its fortunes improve only slightly. The same is true for equities collectively as an asset class, and also for bonds, currencies and property.

What we can take from the above, including the Fed’s policy shift, is that global interest rates look set to remain very low for a long time. This means global fixed interest is an unattractive asset class, but also that it should be possible for South Africa to fund its deficits as long as we can demonstrate progress with economic reforms. Expectations are so low that the possibility of an upside surprise is higher than the pessimists realise.

Investors should also be careful in trying to back only one of the legs of any of the Ks. The future remains uncertain and things can easily take an unexpected turn, as we saw again this year. Therefore, an appropriately diversified strategy that takes personal financial goals and circumstances into account remains the answer.