Lessons from a shifting investment landscape

The past two years have been challenging for investors globally. Markets, by their very nature, are unpredictable, but some important insights emerged from this watershed period that will continue to shift the investment landscape going forward. While it’s not an exhaustive list, here’s what we’ve learnt so far in terms of how the market has surprised us, and how it framed manager selection and asset allocation decisions.

During 2021, there was a clear shift in the key drivers of portfolio returns, compared to 2020. Property and domestic equity markets delivered strong returns during 2021 compared to the muted returns delivered in 2020. Financial markets have positively rerated companies outside of the larger capitalisation stocks that had been penalised through much of 2020. There have also been signs of a reversal of the significant underperformance of value shares relative to growth shares. It’s therefore not surprising that we’ve seen strong performance from managers that lagged their peers in 2020, given their investment approach and resulting positioning. The decision not to make changes to our mix of managers and to stick with the managers that did not benefit from the environment in 2020, added value to portfolios in 2021. This demonstrated the diversification benefit of having exposure to a broad mix of managers that think differently about the world.

As a multi-manager, we spend a substantial amount of time engaging with the asset managers in our portfolios. Two manager engagements stand out for 2021 as among some of the most interesting.

The first is with Baillie Gifford around their belief in the importance of outliers. Their global equity strategy remains completely benchmark agnostic and unconstrained, with key aspects being the long-term time horizon of the manager and a culture that focuses on finding outlier companies that generate extreme returns. This approach emphasises optimism rather than pessimism and loss aversion, while the ‘hold’ discipline is considered more important than the ‘sell’ discipline.

The second is with Capital Group, our partnership manager in the PPS Global Equity Fund, around their unique approach to portfolio construction. The approach allows for effective succession planning and smooth transitioning; they are currently on their third generation of portfolio managers in this strategy. The strategy is managed by a team of portfolio managers, who are not only given discretion in terms of stock selection and positioning but are also expected to manage their portion of the portfolio in line with their own investment style. Capital’s approach allows each of the portfolio managers to play to their strengths while leveraging off their in-house research capability. The portfolio construction has been deliberately designed to achieve cognitive diversity and ensure a well-diversified portfolio.

In our view, the key characteristics displayed by asset managers during the period was collaboration and effective engagement. The competitive nature of the asset management industry does not easily lend itself to effective collaboration. But early in 2021, we witnessed an unprecedented move where about 40 asset managers acted together to raise their concerns about the proposed share exchange between Naspers and Prosus. In addition, a collaborative effort involving asset managers, asset allocators and regulators will be required to successfully transition to a greener economy. It is becoming increasingly important for the industry to come together to deal with these material issues.

In terms of asset allocation decisions, one of the debates in our team last year was whether to increase exposure to South African equities and where to fund it from. Compared to the end of 2019, we have a higher allocation to both South African equities and South African bonds indicating a more attractive investment landscape for the South African investor. South African equities are inexpensive while South African bonds offer the prospect of higher-than-normal returns, adequately compensating investors for their associated risk.

Our portfolios have long been overweight global equities, which we believe present a much broader opportunity set compared to the investment universe available locally. A supportive economic environment and favourable valuations relative to global cash and global bonds remain tailwinds for this asset class. However, the valuation of South African equities looks compelling relative to its own history and even more so relative to global equities, which have become more stretched. Additionally, South African bonds continue to offer attractive yields in absolute terms and relative to cash. The emphasis is on finding the right balance between our exposure to growth assets given the supportive macro environment and the need to diversify some of the South African specific risks.

We have been deliberately increasing our domestic equity exposure since November 2020 and our positive view on foreign equities benefited our portfolios up to end December 2021. Within the interest-bearing composite of our portfolios, our decision to be maximum overweight bonds relative to cash and to maintain a meaningful allocation to inflation-linked bonds also contributed positively to performance over the period.

During last year, what surprised us most in markets was the continued steepness of the yield curve and no meaningful yield compression despite various encouraging developments, which we believe improves South Africa’s risk profile compared to the recent past and our emerging market peers. We have also been surprised by how long it is taking for the climate transition to be reflected in asset prices despite greater urgency in dealing with climate change.

In conclusion, we believe that 2020 and 2021 was a stark reminder of the importance and benefit of remaining invested in a well-diversified portfolio and having exposure to a broad mix of managers that think differently about the world. This combination has historically proven effective in our portfolios over the long term.

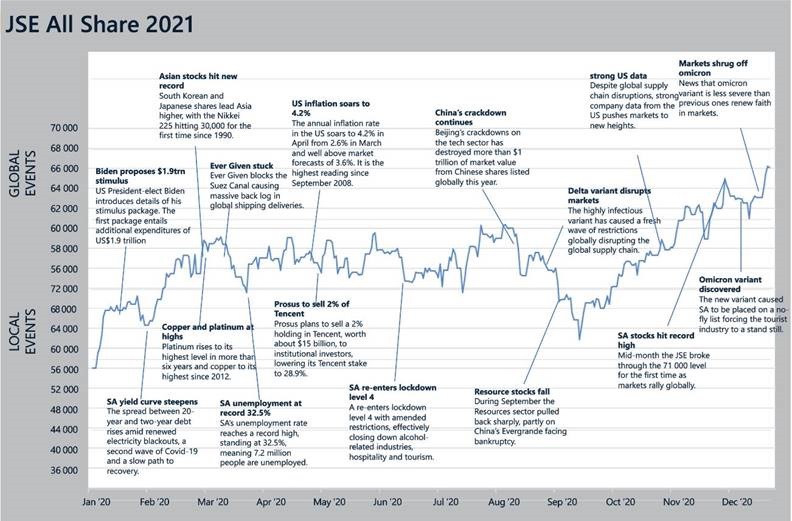

Infographic – 2021 in review