Knowing and not knowing

The chaotic world we live in today is to an extent a product of the American invasion of Iraq in 2003 and its disastrous aftermath. One of its architects was Donald Rumsfeld, who served two terms as secretary of defence, being both the youngest and oldest person to do so.

Infamously, trying to explain why the weapons of mass destruction that justified the war in the first place had not been found, he said,

“Reports that say that something hasn't happened are always interesting to me, because as we know, there are known knowns; there are things we know we know. We also know there are known unknowns; that is to say we know there are some things we do not know. But there are also unknown unknowns - the ones we don't know we don't know.”

Amid another war, investors and policymakers are also grappling with known knowns, known unknowns, and unknown unknowns, particularly when it comes to inflation. This makes policymaking and investing very difficult. And because investors scrutinise central bank policy, and central banks keep a close eye on markets, there are all kinds of feedback loops that complicate things.

Known knowns

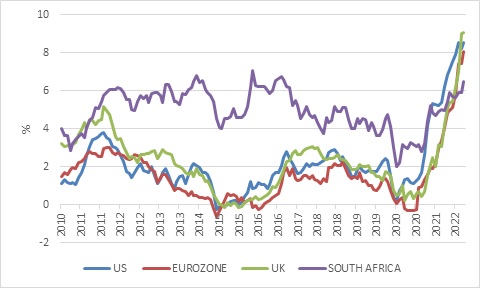

Let’s start with the known knowns. We know that inflation has exploded higher in the last year, notably in developed countries such as the US where people really aren’t used to rapid price increases. While high inflation initially seemed to be transitory, it has not only increased but also significantly broadened out. Indeed, the word “transitory” now sits somewhere between a punchline and a swearword among financial commentators.

Chart 1: Inflation in selected countries

Source: Refinitiv Datastream

So how did we get here? With the benefit of hindsight, it appears to be the perfect storm of factors.

In response to the Covid lockdowns, governments and central banks launched major monetary and especially fiscal policy stimulus measures. This was particularly true in the US, where ample fiscal transfers meant that for the first time during a recession, household incomes increased instead of falling. Fiscal policy probably played a bigger role than monetary injections in causing the inflation surge, but it is also clear that the Federal Reserve left policy too loose for too long. For instance, it was still buying mortgage-backed securities as recently as March even with an epic property boom well underway. This surge in property activity was fuelled by the shift to remote work, but interest rates near record lows clearly also played a role. Since actual and implied rentals form a big part of consumer price indices, hot housing markets contribute directly to inflation.

With so many people spending more time in their larger homes, the demand for goods – furniture, electronics, exercise equipment and also cars – surged even as the capacity to produce, ship and deliver those items were severely constrained by the pandemic. Predictably, the prices of these items jumped. Of note was a global shortage of microchips.

Commodity prices also jumped. At first it was just a recovery from the initial lockdown slump, but soon it became clear that demand was strong and supply constrained. The invasion of Ukraine put significant further upward pressure on commodity prices, especially food and energy. This had a broad impact since the need for food and travel is universal but played a particularly big role in the inflation surge in Europe as many countries rely heavily on Russian gas.

The biggest surprise was probably changing labour market dynamics. Many people, particularly in the US, stopped working. The reasons vary from long Covid to early retirement to lack of childcare options, but the net result is a shortage of workers even though employment has not quite recovered to pre-pandemic levels. Immigration has also declined. Therefore, there are more job openings than unemployed people in the US today (i.e. people who are actively looking for work but can’t find it). Other developed economies also have very tight labour markets. In such an environment, price shocks can reverberate through the economy, rather than being absorbed. Businesses can maintain margins and pass on costs to consumers, and consumers have sufficient income and savings (for now) to keep spending. This is why central banks are acting now: they can do nothing about supply-side shortages, but they can cool demand.

Inflation is still very likely to start declining as some of the Covid-related distortions wear off. Indeed, commodity prices are already well off their highs, while supply chain bottlenecks and backlogs are easing. Some big retailers are now reporting that inventories are too high, having been too low for a long time, and this means manufacturers are seeing declining orders. And because price increases were pronounced in the second half of last year, and early this year, that creates a high base for the year-on-year comparisons later in 2022 and into 2023. However, the unknown known is what happens after inflation starts declining later this year.

Unknown knowns

Will inflation return to the 2% most developed central banks target within a reasonable time frame? If so, some of the interest rate increases that are currently priced in might not happen. It seems difficult to imagine a scenario where inflation declines without severe economic weakness, but such a soft landing is not completely impossible.

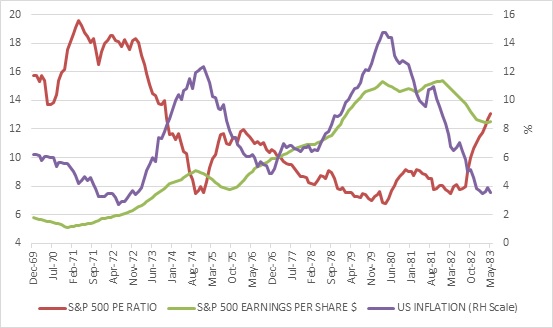

Or does inflation start rising again, reminiscent of the dreaded 1970s? In the 1970s inflation came in waves, with each peak and trough higher than the last, until the Fed under Paul Volcker bludgeoned the global economy into recession between 1980 and 1982, finally ridding it of entrenched inflationary pressures. Such a scenario is likely to coincide with the kind of volatile interest rates and disappointing growth that was experienced in the 1970s – stagflation – and probably similarly disappointing returns from risk assets. This is not because companies won’t be able to make profits, but because investors will probably demand a substantial risk premium in the form of very low ratings.

Chart 2: 1970s earnings, ratings and inflation

Source: Refinitiv Datastream

There is also a scenario where inflation simply keeps falling. This might sound crazy given where we are now but remember that the big problem in the 2010s was that inflation was too low. If globalisation really does go into reverse, security concerns overwhelm efficiency requirements and the world starts splitting into US and China-dominated blocs, a return to such “lowflation” is unlikely. However, if the factors that contributed to persistently low inflation such as technological disruption, excessive debt levels and slowing population growth dominate, and are combined with excessively tight fiscal and monetary policy, it is not impossible that inflation again undershoots central bank targets while interest rates eventually fall back to near-zero levels. If that scenario plays out, it is a very different investment environment.

Unknown unknowns

Unknown unknowns are also sometimes known as black swan events. They are things we can’t predict because we aren’t even aware they could happen, but nonetheless have a big impact. The Covid 19-pandemic is an obvious example. Yes, experts warned that a global pandemic could happen at any point, but no-one could know that it would emerge in Wuhan in late 2019 and spread the way it did. Russia’s invasion of Ukraine was possibly also a black swan, though Putin did run a dress rehearsal in 2014 and European leaders should not have been nearly as surprised as they were.

Such events can still play a big role on how the inflation picture changes. Covid was initially deflationary, but the policy response turned it into an inflationary event. In fact, this is often how inflation regimes change, when policymakers try to soften the blow from some external shock rather than letting the shock be absorbed. This is not to say that the gain of low inflation is better than the pain of absorbing the shock. Rather, that there are always difficult trade-offs to be made, often under conditions of huge uncertainty, while the law of unintended consequences always lurks in the background.

The response to the current inflation shock could therefore worsen it. For instance, fuel subsidies would simply make people use more fuel, when clearly we should be encouraging spare usage. In the 1970s, for instance, some governments responded to inflation by introducing price freezes. That offers short term relief to consumers but discourages the supply response meaning that the inflation problem hasn’t gone away. It only does when supply and demand are better matched, and price and wage-setting decisions are not influenced by the expectation of high inflation persisting.

Now and later

In other words, investors face two different but interrelated problems. In the short term – over the next 12 months or so – the problem is knowing whether inflation can moderate sufficiently for the Fed (and other central banks) to back off from aggressive interest rate hikes before their economies are tipped into recession. How this plays out will have a big impact on how asset classes behave. But that still leaves the medium-to longer term question intact: how to position portfolios for the next three to five years when we don’t know what inflation regime we will be living under? We could have a situation where inflation falls in the short term but remains sticky over the longer term. Or vice versa.

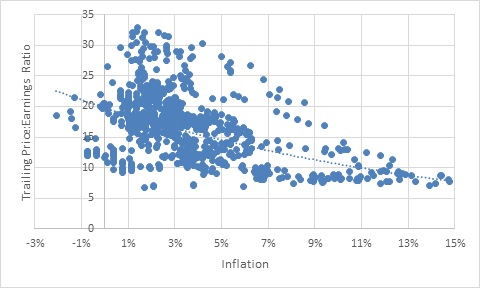

And it is not just an academic question: history shows that markets trade at lower valuations (price: earnings ratios) when inflation is higher. In other words, investors demand a greater margin of safety when inflation is high, while interest rates are also typically higher. As Chart 3 below shows, there is a clear inverse relationship between inflation and valuations. The sweet spot is inflation between 1% and 4%. In other words, inflation doesn’t necessarily have to be very low, but if inflation is above 5%, the rating investors put on each dollar worth of earnings declines noticeably.

Chart 3: S&P 500 PE ratios and inflation since 1950

Source: Robert Shiller and Refinitiv Datastream

Unknown knowns

Finally, unknown knowns were not in Rumsfeld’s original schema, but it can refer to knowledge we don’t realise we have. This is common in large organisations where executives often pay consultants a lot of money for insights that already sit a few layers down in the hierarchy. It can also refer to knowledge we have but don’t pay attention to or ignore in the heat of the moment. In investing, we all “know” not to buy high and sell low, we all “know” not to make decisions based on fear and greed, and we all “know” to diversify and spread our risk. Yet, time and again people act against this common knowledge. We all know that the stock market declines from time to time and yet people still bail out at the first sign of volatility. The way ahead is uncertain. We may or may not be settling into an entirely new global inflation regime. Navigating these changes will require a degree of nimbleness but tried-and-tested investment principles remain extremely important.