Keep calm and carry on investing offshore - why geopolitical tensions shouldn’t mean you dilute your offshore exposure

Duncan Lamont, CFA - Head of Strategic Research at Schroders

Kondi Nkosi - Country Head of Schroders in South Africa

Many money managers and investors would previously have jumped at the chance to increase offshore allocations after it was recently announced pension funds can now hold 45% offshore exposure, up from 30%. Some may now be questioning the decision to move more money abroad in the face of the tragic events in the Ukraine and their impact on markets.

But, diversification – including offshore diversification – and other basic long-term investing pillars should not be disregarded because of volatility caused by geopolitical events.

“The upsetting scenes in Ukraine have sent shockwaves through us all as individuals, and our first thoughts are with the people of Ukraine and the humanitarian crisis unfolding there. Investors will be well aware that global stock markets have been volatile but as tensions soar, it’s important to try avoid making rash decisions– including diluting offshore exposure.

“Although the JSE has been performing relatively well in the face of the current volatility with some proponents stating that prospects look positive; South African equities are not immune from international headwinds. With the number of listed companies dwindling locally, South Africans would do well – as always – to bolster their portfolios with offshore opportunities – including in times of international turmoil,” says Kondi Nkosi, country head of global asset manager Schroders, in South Africa.

Adding to this, Head of Strategic Research at Schroders, Duncan Lamont, points to four bite-sized pieces of research showing investors are best served not making impulsive decisions at times of heightened geopolitical tensions.

“Below are five pieces of data and analysis which I hope will help investors to see the longer-term picture and avoid rash decisions,” says Lamont.

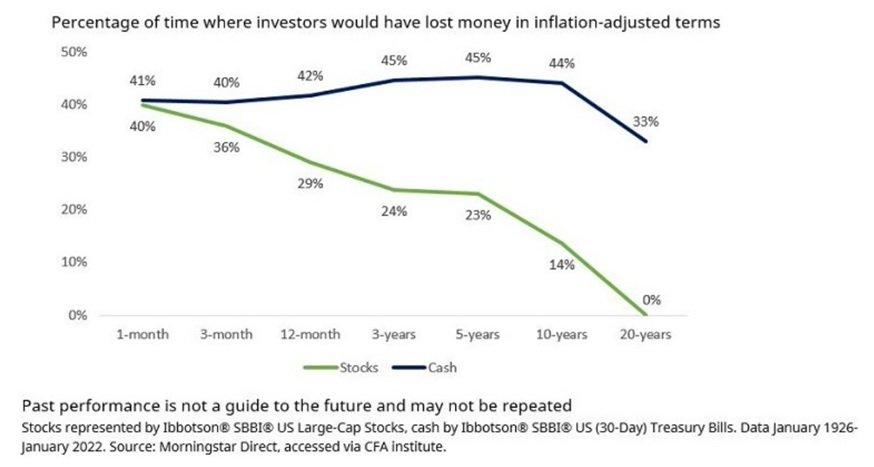

1. Stock market investing is very risky in the short run but less so in the long-run – unlike cash

Using almost 100 years of data on the US stock market, we found that, if you invested for a month, you would have lost money 40% of the time in inflation-adjusted terms i.e. in 460 of the 1,153 months in our analysis.

However, if you had invested for longer, the odds would shift dramatically in your favour. On a 12-month basis, you would have lost money slightly less than 30% of the time. Importantly, 12-months is still the short-run when it comes to the stock market. You’ve got to be in it for longer.

On a five-year horizon, that figure falls to 23%. At 10 years it is 14%. And there have been no 20-year periods in our analysis when stocks lost money in inflation-adjusted terms.

Losing money over the long run can never be ruled out entirely and would clearly be very painful if it happened to you. However, it is also a very rare occurrence.

In contrast, while cash may seem safer, the chances of its value being eroded by inflation are much higher. And, as all cash savers know, recent experience has been even more painful. The last time cash beat inflation in any five-year period was February 2006 to February 2011, a distant memory. Nor is that something that’s expected to change any time soon.

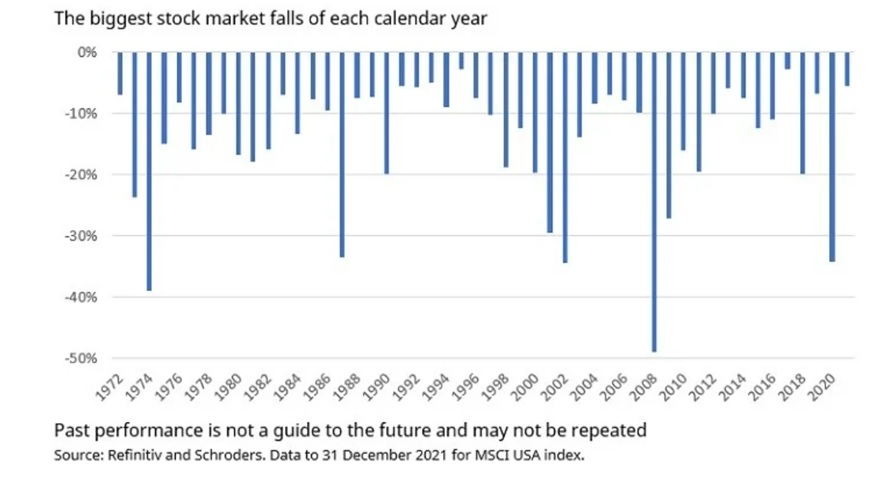

2. 10%+ falls happen in more years than they don’t – but long term returns have been strong

By Thursday of last week, global stock markets had fallen by 10% from their peak. They rebounded on Friday but are heading lower again early this week.

10% may feel like a big fall but it’s actually a regular occurrence. The US market has fallen by at least 10% in 28 of the past 50 calendar years i.e. more often than not. In the past decade, this includes 2012, 2015, 2016, 2018 and 2020.

Despite these regular bumps along the way, the US market has returned 11% a year over this 50 year period overall.

The risk of near term loss is the price of the entry ticket for the long term gains that stock market investing can deliver.

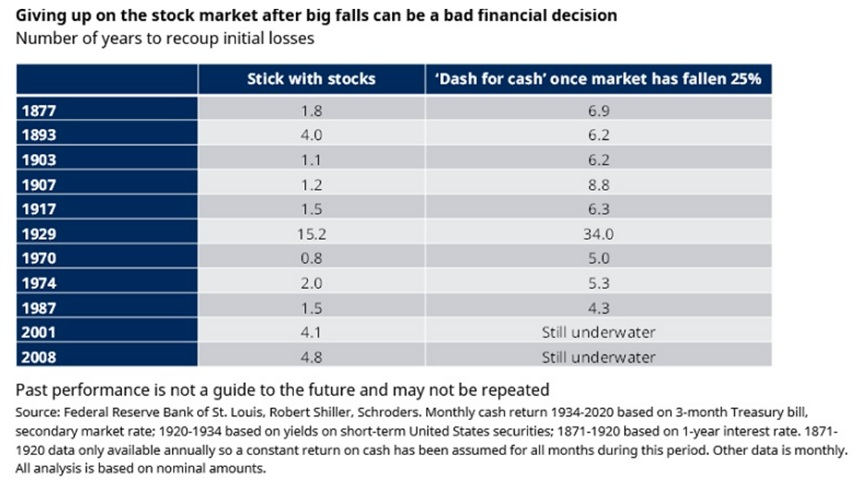

3. Bailing out after big falls could cost you your retirement

While the market hasn’t fallen too much so far, further volatility and risk of declines cannot be ruled out. If that happens, it can become much harder to avoid being influenced by our emotions – and be tempted to ditch stocks and dash for cash.

However, our research shows that, historically, that would have been the worst financial decision an investor could have made. It pretty much guarantees that it would take a very long time to recoup losses.

For example, investors who shifted to cash in 1929, after the first 25% fall of the Great Depression, would have had to wait until 1963 to get back to breakeven. This compares with breakeven in early 1945 if they had remained invested in the stock market. And remember, the stock market ultimately fell over 80% during this crash. So, shifting to cash might have avoided the worst of those losses during the crash, but still came out as by far the worst long-term strategy.

Similarly, an investor who shifted to cash in 2001, after the first 25% of losses in the dotcom crash, would find their portfolio still underwater today.

The message is overwhelmingly clear: a rejection of the stock market in favour of cash in response to a big market fall would have been very bad for wealth over the long run.

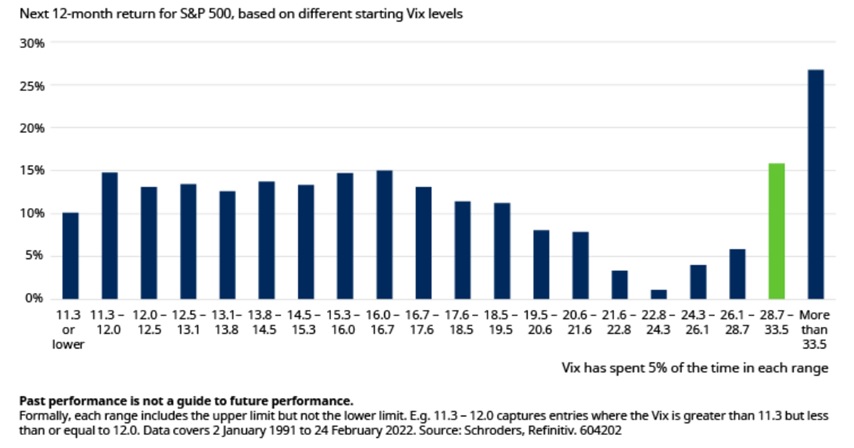

4. Periods of heightened fear have been better for stock market investing than might have been expected.

Escalating tensions between Russia and Ukraine have recently sent the stock market’s “fear gauge”, the Vix index, higher. The Vix is a measure of the amount of volatility traders expect for the US’ S&P 500 index during the next 30 days.

It has recently risen to a level of 32 on Monday 28 February, well above its average since 1990 of 19, and steeply higher than its start of year level of 17. It’s not hard to imagine a scenario where it moves even higher in the coming days as events continue to unfold.

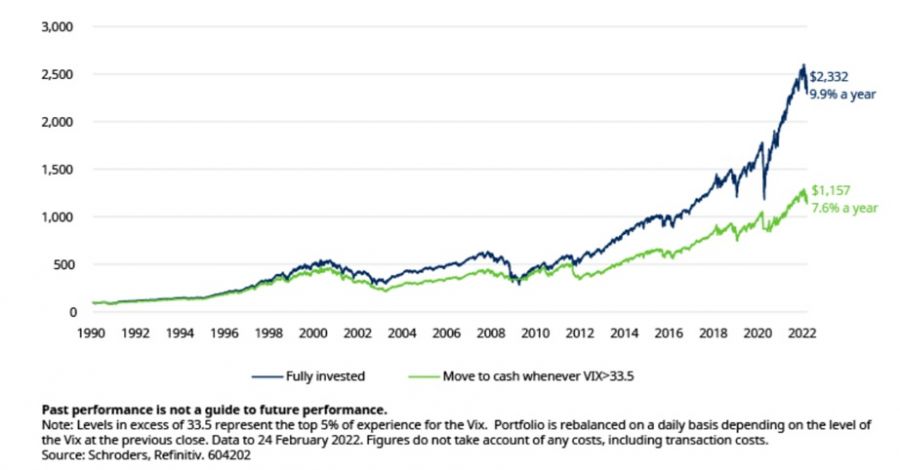

However, rather than being a time to sell, historically, periods of heightened fear have been when the brave-hearted have earned the best returns. On average, the S&P 500 has generated an average 12-month return of over 15% if the Vix was between 28.7 and 33.5. And more than 26% if it breached 33.5.

Markets have performed well when the Vix has been around the current level of 30, or higher

We also looked at a switching strategy, which sold out of stocks (S&P 500) and went into cash on a daily basis whenever the Vix entered this top bucket, then shifted back into stocks whenever it dipped back below. This approach would have underperformed a strategy which remained continually invested in stocks by 2.3% a year since 1991 (7.6% a year vs 9.9% a year, ignoring any costs).

A $100 investment in the continually invested portfolio in January 1990 would have grown to be worth twice as much as $100 invested in the switching portfolio.

Growth of $100 fully invested in stocks vs switch to cash when VIX was high

As with all investment, the past is not necessarily a guide to the future but history suggests that periods of heightened fear, as we are experiencing at present, have been better for stock market investing than might have been expected.

Duncan Lamont, CFA - Head of Strategic Research at Schroders

Kondi Nkosi - Country head of Schroders in South Africa