Janu-worries

Anyone hoping for a quiet start to the year would be severely disappointed. Global markets have been stalked by immense volatility and major bond and equity indices ended the month in the red.

In fact, for some benchmarks, it has been the worst start to the year in a very long time. The main reason of course is that the US Federal Reserve (the Fed) is planning on raising interest rates. Investors are trying to price in the extent of these rate increases, which will largely depend on how inflation evolves in the US. For while the Fed is very much the world’s central bank in terms of its global impact, it is quite insular in its focus, basing its decisions on the domestic US outlook.

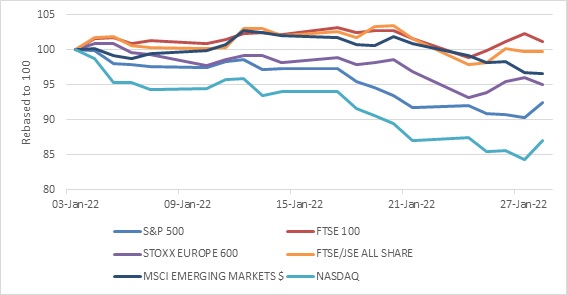

Chart 1: Global equities in January

Source: Refinitiv Datastream

Needless to say, there is always uncertainty associated with this outlook. Even the mighty Fed with its army of economists struggles to predict the future at the best of times. Making forecasts when the economy is still distorted by Covid is even harder. Inflation has certainly risen much more, and stayed high for longer, that it anticipated. Any talk of “transitory” is out the window. So as much as the Fed tries to give guidance to avoid any nasty market surprises, this guidance is subject to change. Life, the world, and markets, it is all unpredictable.

Adding to this uncertainty is the geopolitical backdrop. Russia is still staring menacingly at its neighbour Ukraine. War on the edge of Europe remains a possibility. The most immediate economic impact will be on Ukraine and Russia’s economies, with the latter likely to be subject to sanctions. However, having been subject to sanctions since the 2014 annexation of Crimea, the Russian economy is somewhat shieled. Russia can respond by cutting of gas supplies to Europe. Already, global oil and gas prices have increased, adding further pressure on inflation and squeezing household purchasing power further.

Strange as it might seem, however, the actions of the Fed matter more than soldiers and tanks unless the war is truly global and destructive as in the first half of the 20th century.

Jayhawk?

The Fed’s January policy meeting saw no change to its policy stance, but the statement noted that progress towards full employment and inflation well above its 2% target means it would raise rates soon, probably in March. This was all expected. What was not quite expected was that Chairman Jerome “Jay” Powell sounded quite hawkish in the post meeting press conference. He seems firmly behind a series of rate increases this year, and is more concerned about sticky inflation than in the past, and refused to rule out more interest rate hikes this year than the three that were originally pencilled in. Futures markets now price in five hikes this year.

This has put further pressure on bond and equity markets, but more dramatically so in the case of the latter, and more particularly on those shares and sectors whose extreme valuations were justified by low interest rates. It appears that equities will have to generate returns the old-fashioned way now, by growing profits. The economic environment is still very much conducive to this. The International Monetary Fund expects 4.4% global growth this year, 4% in the US and 3.9% in the Eurozone. This is above the long-term average in each case. We are still far from the point where interest rate increases hurt the real economy (though it is uncertain where exactly that point is). Therefore, even if equities derate with rising bond yields (as investors are prepared to pay less for each dollar’s profit) profit growth itself should still be robust and the net result can still be positive equity returns from a broad portfolio of stocks. Especially if you consider that not everything was expensive at the start of the year. European, Japanese and emerging market shares had underperformed the US for the better part of a decade.

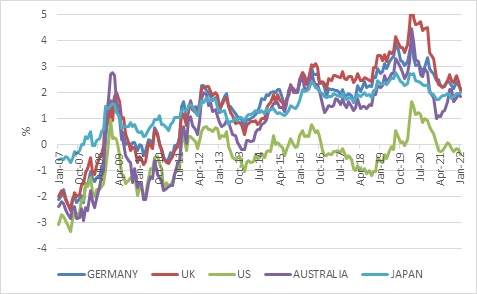

In the short term, anything can still happen and the derating can continue (i.e. declining price: earnings multiples). However, it is hard to imagine fixed income outperforming equities over the medium to long term in developed countries. That is even after projected increases, interest rates are too low. In most developed markets, dividend yields exceed 10-year government bond yields. In the US, they are similar, and you can earn almost as much from dividend income which grows with inflation, as interest income from a bond, which doesn’t. If you make the comparison against inflation-linked bond yields, which are still negative, equities are the clear winner.

Chart 2: Dividend yields minus 10-year government bond yields, %

Source: Refinitiv Datastream

Locally

Locally, equities have been somewhat shielded from the Fed-induced volatility. It helps that the local market was not expensive – unlike US tech – even after last year’s rally. It has been the blue-sky growth and speculative investments that have been hardest hit. There is very little of that on the local market. It also helps that global commodity prices have increased in recent weeks. (This in itself tells you that investors are not pricing in a global recession, but rather the equity volatility represents a recalibration of asset class valuations).

For SA bonds, the big question is firstly, whether there is spill-over from rising global bond yields, secondly whether fiscal metrics continue improving, and thirdly what the Reserve Bank’s own plans are.

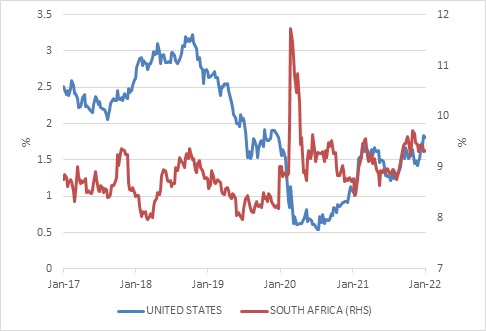

On the first question, the answer is not yet. SA bonds have in fact rallied in January even as developed market bond yields sold off. It helps that they were already very high. At the start of the year, the 10-year South African bond yield was 9.35%, substantially above a US equivalent of 1.49% (since up to 1.85%). Importantly, the rand has been relatively firm in the face of rising global risk aversion and a stronger dollar. While foreigners still own a large percentage of the local debt market - 28% in December – this is way down from the peak of 42% in March 2018. In other words, one shouldn’t expect massive capital outflows if there haven’t been major inflows.

Chart 3: SA and US 10-year government local currency bond yields, %

Source: Refinitiv Datastream

Secondly, new Treasury data suggests that tax revenues are still running ahead of projections, which means that the budget deficit for the current fiscal year should end up being smaller than estimated even as recently as October’s MTBPS. To be sure, the deficit is still large in absolute terms, but the market cares more about direction than levels. While South Africa is still a way away from ratings upgrades, it means that there shouldn’t be further credit ratings downgrades this year, especially since the global cycle of ratings downgrades has turned.

Thirdly, the Reserve Bank is also on a hiking path, with two 25 basis points increases under the belt already. As it noted in its statement, further gradual interest rate increases will be necessary to keep inflation expectations anchored and therefore avoid the need to slam the brakes later on.

Gradual cycle

Given higher fuel prices, the SARB’s raised its forecast of headline inflation for 2021 to 4.9% from 4.3%. It is expected to moderate to 4.5% in 2023 and 2024, smack bang in the middle of the 3% to 6% target range. Excluding food and fuel prices, core inflation is expected to only be 3.8% this year. However, prevailing risks suggest inflation is more likely to exceed these forecasts than undershoot them. On the growth side, it is a muted medium-term outlook. The economy is expected to expand around 1.8% for each of the next three years.

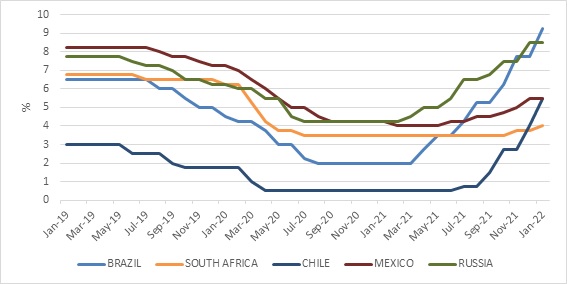

Therefore, the gradual hiking cycle is not responding primarily to domestic factors, since there is no sign of typical overheating, speculative activity, labour shortages and rapid credit growth that would accompany an environment of excessively low interest rates. Rather, with global market conditions potentially becoming less favourable for emerging market economies as the Fed increases rates and ends its bond purchases, the SARB needs to build buffers. In this instance, it is by moving the repo rate back towards being positive in real terms. However, the SARB need not act as aggressively as other emerging market central banks. Just last week, Chile hiked rates by 150 basis points. Its policy rate has jumped from 0.5% to 5.5% in the space of seven months.

Chart 4: Emerging market policy interest rates, %

Source: Refinitiv Datastream

Gradual interest rate increases will cool domestic demand somewhat, but the repo rate is still likely to settle at a lower level than before the pandemic which means the interest burden on households should remain manageable and there should be some further growth in borrowing, including mortgage loans.

As for the impact on bonds, the yield curve remains very steep even after factoring in a series of rate increases. Therefore, the medium-term total return outlook for government bonds still exceeds that of cash (money market). Bonds are more volatile than cash, but the interest income from long bonds should more than offset price volatility over a medium-term horizon.

In summary

“As January goes, so goes the year” is one of those old market aphorisms that turn out to be true some years and false in other years. We simply can’t predict medium-term returns on what happened during a single month. Volatility can still persist for some time as investors grapple with the path of global inflation and interest rates, but there is still no reason to expect that an appropriately diversified portfolio will collapse in a heap. Enough assets are still priced for growth in an expanding local and global economy.