Is the relative return argument for EMs becoming less of a draw card for cheap capital?

When the US Federal Reserve made its quantitative easing outlook announcement in June this year, global markets traded in negative territory, with emerging economies feeling the impact most significantly as the developed world again looked to more familiar investment avenues.

Although the US Federal Reserve (Fed) has subsequently indicated that US economic growth remains "modest" and pledged to maintain its aggressive bond-buying programme, questions relating to the future of quantitative easing (QE) and its ramifications for emerging markets (EMs) remain. Improving housing and labour market conditions in the US make it likely that the Fed will see the current level of monetary stimulus as no longer appropriate for the prevailing realities in the economy and, as such, start to reduce QE towards the latter part of this year.

The relative return argument for EMs thus becomes less of a draw card for the cheap capital currently in circulation. The hunt for yield and growth markets that has characterised the investment landscape over the last few years has seen international investors and companies becoming more adventurous and seeking a new repository for their investment monies in Africa. With this ‘cheap' money possibly not being as readily available in the medium-term future, investors may now look to unwind their interests on the continent.

Fortunately for EM equities, declining valuations in recent years have already discounted at least some of this deterioration in EM macro drivers. "Improved business operating environments and legislative regimes, resilient economies and flat to declining soft commodity prices keeping inflation levels in check on the continent may likely continue to make Africa an attractive investment destination,” says Fungai Tarirah, head of Africa investments at Momentum Asset Management. "Of The 50 most improved economies for doing business in between the years of 2005 and 2012, almost half (42.9%) were in Africa, according to the World Bank Doing Business Index. These factors will likely keep real economic growth rates in many African countries reasonably high, allowing robust growth in company earnings that will support share prices.”

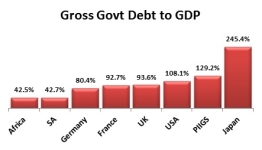

Although a withdrawal from EM and frontier market (FM) bonds could see yields pick up in the various countries, many have low government debt to gross domestic product (GDP) ratios, which afford the economies room in a rising yield scenario. Africa's median debt/GDP ratio stands at just 40% and even South Africa's, at 42.7%, is lower than that that of the US (108%), UK (93.6%) and France (92.7%). Rising debt repayment interest rates will therefore not hamper these countries' ability to grow their economies, affording governments the ability to implement countercyclical measures aimed at offsetting the effects of a possible withdrawal of QE.

Source: IMF

WEO April 2013, Momentum Asset Management

Foreign direct investment (FDI) flows into the continent continue to increase. Legislative changes aimed at promoting international investment interest in the continent are reducing business start-up times, accommodating dividend repatriation and increasing public-private partnership. African Countries are also building their foreign currency reserves, providing a further cushion.

"Although South Africa faces economic, policy, infrastructure and labour challenges and possible credit rating downgrades, demand for African bonds remains reasonable and, in the equity market, it's ‘business as usual',” concludes Tarirah.