Is it time to redefine benchmarks?

Lonwabo Maqubela, a portfolio manager at Perpetua Investment Managers.

One of the most complex aspects in investing, on the part of the investor and the investment manager, is that of benchmarks. In essence, a benchmark is commonly understood as the yardstick against which an investment manager’s return is assessed and measured. Benchmarks are usually quoted stock market indices or the average of peer returns. While the notion of a benchmark might appear relatively straight-forward, there are two key aspects which Perpetua Investment Managers believes creates real complexity surrounding benchmarks, and especially index benchmarks (FTSE/JSE Shareholder-weighted Index (SWIX) or FTSE/JSE All-Share Index (ALSI) being most popular in SA):

• The client effect: Does an index benchmark truly deliver the best outcome for a client?

• The investment manager effect: How does an index benchmark affect the actual behaviour of an investment manager?

The index benchmark tends to concentrate the client’s and the investment manager’s focus disproportionately on returns relative to the index and not enough on other critical aspects, especially the risk of monetary loss.

Bear in mind that with the stipulated goal of outperforming the stated benchmark being the foremost objective, the majority of investment managers tend to conclude that delivering a return that is conversely much lower than the benchmark over any time period will naturally increase the risk of losing that client (i.e. business risk). Accordingly, several investment managers determine that a far lower business risk strategy would be to use the benchmark as a default starting point in the construction of their client portfolios. Then these investment managers subsequently go overweight or underweight individual shares to varying degrees depending on their view on a specific share, but tend not to stray very far from the actual index weightings in their portfolios. This approach means that exposure to shares with large weightings in an index is retained even when the manager believes the share is fundamentally over-valued or expensive.

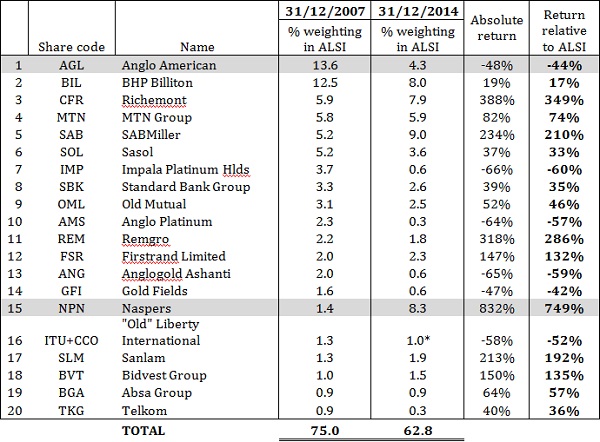

In a highly concentrated market like South Africa, this approach can yield some very interesting outcomes and pose some real risks. Table 1 below considers, for example, the largest 20 shares in the ALSI at the end of 2007 (the date was selected for being close to the previous peak in the ALSI in real terms) and their weightings at the end of 2014. The third column reflects the absolute return of each share and the fourth column the relative return of the share compared with the ALSI, over the same time period.

Table 1: The largest 20 ALSI shares over time (at calendar year end)

* Liberty International unbundled into ITU and CCO in 2010. This is the combined weighting.

Source: Data from I-Net Bridge

An example of one of the significant drawbacks of investing based on index weightings is revealed in this table. At one end, consider the largest-weighted share in the ALSI at the end of 2007, being Anglo American (AGL) with a weighting of 13.6% at 31/12/2007. If a benchmark-cognisant investment manager invested according to that benchmark weighting, the manager would likely have owned AGL as one of its largest holdings, even if it was held at an underweight position. Over this time period under consideration, AGL underperformed the market by more than 40% and the total return for the share was a negative 48%. In other words, owning any AGL over this seven-year period was an incorrect decision. Conversely, a share like Naspers (NPN) had a benchmark weighting of 1.4% at 31/12/2007, while at 31/12/2014, NPN was the second-largest share in the ALSI, with a weighting of 8.3%. During this time, as the weighting change indicates, the share increased by more than 830% in absolute terms and outperformed the ALSI by more than seven times. Today, many investment managers hold NPN among their largest five shares, often in part due to its large benchmark weighting – when Perpetua would argue the best time to have owned and held Naspers as one of their largest five shares was around seven years ago, not now.

The AGL and NPN example attempts to explain that investing according to benchmark weightings can often cause exactly the wrong positioning in portfolios at the wrong point in time, and especially at extremes (which Perpetua would consider end 2007 and end 2014 to be).

Perpetua agrees that clearly all investment managers need to be assessed against some measure. However, the excessive obsession with index benchmarks as that measure and, more importantly, the intended and unintended effects this has on an investment manager’s behaviour, seems to result in generally better outcomes for managers and their business rather than for investors and their long-term returns.