Is it time to panic?

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

For most of this year prior to September, global equity, commodity and bond markets were sending different messages.

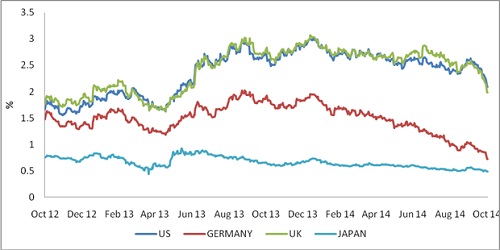

A strong equity market appeared to be pricing in decent growth, whilst a rallying bond market signalled weak growth and lower inflation. Commodity markets were generally weak but mixed. The message is now at least consistent: markets are worried about stalling global growth and deflation. Bond yields have fallen across the board, with German 10-year at 0.8% and US 10-year at 2%. Equity markets have given back much of their 2014 gains and commodity prices, especially oil, are plummeting. Volatility has returned after a long absence (but the S&P 500 Volatility Index (VIX) at 26 is by no means historically high).

Are market fears about global growth warranted? On the commodity side, price declines are due to increasing supply. Although the oil price does reflect softer global demand, the overwhelming factor is that there is a supply glut, with US production having surged over the past five years. Historically, the Organisation of the Petroleum Exporting Countries (OPEC) cartel would’ve reduced supply to prop up the price, but they’ve taken no action this far, with individual OPEC members fighting for market share rather than higher prices by keeping the taps open. A falling oil price is a great boost for consumers worldwide, but very bad news for oil producers, including listed oil companies (many of whom are highly geared).

US recovery still on track

The oil price itself is not the most reliable indicator of global growth. More accurate indicators such as purchasing manager indices and exports are still pointing to sustained, but by no means exciting, global economic growth. Last week for instance, the latest Chinese export data showed a 15% annual increase. China’s economy is growing slower than the break-neck rates achieved over the past decade, but still around 7% in real terms. More importantly, the US economy is still doing well, with the most recent data – weekly unemployment insurance claims – showing a continued improvement in the labour market. Coupled with lower fuel prices, it means the $11trillion US consumption machine is shifting its gears up, not down. Several members of the Federal Reserve’s (Fed’s) monetary policy body delivered speeches over the past week, and the general tone is still that the US economy is strong enough to absorb interest rate increases from mid-2015. The Fed can delay rate hikes, especially if inflation and inflation expectations keep falling below target.

Europe is the big worry

On the other hand, Europe is definitely looking weak and European equities have lost more than other main markets. Eurozone inflation came in at 0.3% in September, and lower commodity prices mean inflation rates could turn negative soon (Italy is already negative). Unemployment is stubbornly high, unlike in the US where it has fallen sharply. But unlike the US, the policy response in Europe has been inadequate at best and dysfunctional at worst. Europe needs the European Central Bank to launch an aggressive quantitative easing programme to achieve the 2% inflation target. It also needs its governments to ease up on fiscal austerity in order to revive growth. Both policy responses are blocked by German resistance. Perhaps now that Germany’s economy is also flagging, as the DAX is down 10% year-to-date, Berlin would be more amenable. European government bond yields seem to be converging on Japan’s yields, reflecting deflation fears. Spreads on high-yield corporate bonds are moving in the opposite direction; higher borrowing cost for companies is certainly not good news for economic growth.

Some perspective needed

While the Eurozone’s prospects have deteriorated, the mediocre growth outlook for the rest of the world is pretty much the same as two months ago, before the sell-off started. For individual investors, the sharp declines on markets are obviously worrying, but a few things need to be remembered. Firstly, markets never go up in straight lines. Since the current recovery started in March 2009, there have been 12 corrections of more than 5% on the JSE All Share. Over this period, the ALSI has returned 20% per year. It needs to be said again: equity investors need to be able to stomach this kind of volatility and keep a long-term view. Secondly, diversification has again proven to be a very useful strategy. Within equities, most of the pain has been felt by resource shares; financial shares are still up 9% year-to-date. Local bonds and listed property have held up well during the recent market turmoil. A weak rand this year has boosted offshore investments, irrespective of the underlying performance of the foreign assets. Thirdly, just as investors get excited when markets go up, many get scared when markets fall. This worsens the up and down movements of the market, tempting other investors to jump on the bandwagon. So no, it’s not time to panic. Selling after a market correction will only crystalise losses and likely put investors further – not closer - to achieving their long-term financial goals.

Chart 1: Developed market 10-year government bond yields

Source: Datastream

Retail sales reflect weak SA economy

The only local data release of note last week showed that retail sales remain weak but are not falling over. Real retail sales rose by 2.1% year-on-year in August, down from a 2.4% in July.

Month-on-month seasonally adjusted growth was 0.6%, down from 1.2% in July. Seasonally-adjusted real retail sales rose by 0.9% in the three months to end August compared to the previous three months. The categories with the largest weights in the index are general dealers (39%) and retailers of textiles, clothing, footwear and leather goods (22%). Both categories posted positive growth in August, with the former growing by 3.4% year-on-year and the latter by 0.2%.

The biggest annual decline was again posted by specialist retailers of food, beverages and tobacco, namely -1.4% in real terms due to higher food prices (growth was 6.5% in nominal terms). Retailers of household furniture, appliances and equipment experienced very modest nominal growth (2.1%) and real growth (0.3%), pointing to very low furniture inflation and volume growth. Overall nominal retail sales growth picked up to 8.3% year-on-year from 8.5% in June. This growth rate is slightly higher than the growth rates posted over the past year, implying that higher inflation is behind the slowdown in real sales.

Household finances to remain under pressure

The pressure on household finances keeps building due to higher inflation, rising interest rates, as well as general slowdown in job creation and income growth. While a petrol price cut can be expected next month, the weakness of the rand means South African consumers will not benefit as much as consumers in the US from lower oil prices. Consumers also have to contend with tighter monetary and fiscal policy next year (or sooner, depending on what happens with this week’s Mini-Budget and next month’s Monetary Policy Committee meeting). Meanwhile, annual growth in household credit is also below 5%, meaning that spending will not be propped up by borrowing. Retailers must be wondering if the traditional bumper Christmas shopping season will disappoint this year.

A soft economy still points to gradual rate hikes

Retail sales growth is by no means strong, and the weakness of household spending is confirmed by other surveys, i.e. motor sales, petrol sales, convenience stores, services and property. But retail sales are also not rolling over completely. Growth of around 2% in real terms and 8% in nominal terms appears consistent with the economy’s underlying growth rate.

These numbers are unlikely by themselves to influence the SA Reserve Bank’s (SARB’s) monetary policy decisions. The SARB has to balance inflation above the 3% - 6% target, a struggling economy and a currency that is very vulnerable to further weakening due to the large external deficit and the prospect of higher US interest rates. This still implies a very gradual rate hiking cycle.

Chart 2: South African retail sales growth

Source: StatsSA