Investor roadmap for navigating post-downgrade market turmoil

Andrew Davison, a member of the Actuarial Society of South Africa’s Investments Committee.

Successfully navigating your way through post-downgrade market turmoil will require a clear head and a solid long-term investment strategy.

Andrew Davison, a member of the Actuarial Society of South Africa’s Investments Committee, cautions that now is not the time to panic, as knee-jerk decisions are likely to result in poor investment outcomes.

“If you have put in place a well thought through investment strategy based on your long-term goals, there should be no need for sudden changes to your investment portfolio,” he says.

He notes that investors who panic and try to time the market by switching their portfolios into cash are likely to lose out on periods of market recovery and growth. Timing the market means attempting to avoid losses by selling investments when markets are down, and buying shares when markets are running.

“Market timing hardly ever works. Typically investors panic and sell when volatility has already impacted negatively on performance, thereby locking in their losses.”

“During the lifetime of your investments there will be times when some of the investment vehicles underperform. That does not mean, however, that you have made a loss. Only when you sell your units do you realise any gains or losses. For the rest of the time these are only true on paper.”

Therefore, says Davison, make sure you have time on your side when building an investment portfolio. “Time buys you the luxury of absorbing short-term stock market volatility.”

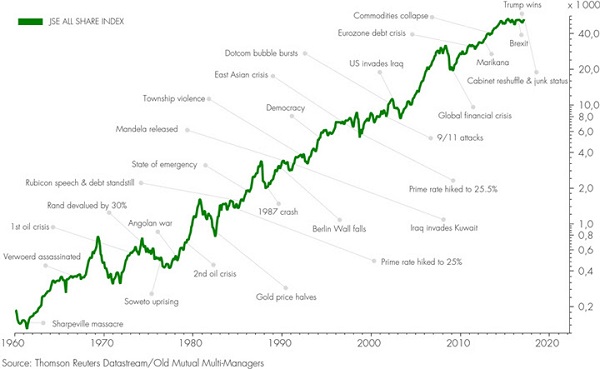

To illustrate, he points out that the JSE All Share Index (ALSI) delivered returns of 13% per year in the five years to the end of December 2016, despite economic weakness and events such as the removal of Nhlanhla Nene as Finance Minister and the shock Brexit announcement by the UK.

However, this return only benefitted those investors who stayed committed and rode out the volatility over the five-year period.

“This is not the first time we have been sub-investment grade, or faced investment risks. In the 1970s the market fell by as much as 60%, and it took almost a decade to recover. This can be uncomfortable and can test investors’ resolve, but the important thing to remember is that ultimately the market keeps grinding higher over time,” he says.

“If you don’t have a clear plan in place, then you should treat this as a wake-up call to set your investment goals and develop a sound long-term financial strategy. If you feel uncertain about how to do this then consult a financial adviser. It’s not too late to start now.”

Davison says that if you are saving towards your retirement for instance, you should have an idea of how much you need to accumulate and your time horizon.

“Remember that your time horizon is not to retirement, but should extend into retirement. The exact end date is uncertain because it is actually for your lifetime.”

“If you have a clear plan you will then have chosen specific portfolios for a reason, and when events such as a downgrade happen you will be able to remain focused on what you are trying to achieve,” he explains.

He notes that if you are concerned about the impact of the downgrade on your investments, your first move should be to contact your adviser.

“Good advisers play a valuable role in managing their client’s investment behaviour by taking the emotion out of investment decisions. If you are feeling uncomfortable, give your adviser a call,” he says.

He offers the following additional tips for successfully managing your investments and finances in the months to come:

1. Seize investment opportunities

Davison points out that weaker share prices may offer investors many value opportunities, enabling them to purchase more shares with any new contributions they make towards their savings.

He emphasises that if you are saving towards retirement then you are making a regular contribution from your salary every month. This means that you automatically benefit from Rand-cost averaging, buying more shares when prices are low, and fewer shares when prices are high.

“The turmoil associated with a downgrade may lead to volatility in various sectors and even without changing anything your monthly contributions may be buying stocks at more attractive prices. When these recover you are likely to benefit from the returns,” he explains.

2. Diversification is key

Diversification is key to achieving the best possible investment outcomes while minimising your investment risk, states Davison.

“This means diversifying between different asset managers with different investment styles, as well as between different asset classes, sectors and regions,” he explains.

He notes for instance that if you already had offshore exposure built into your investments, then you will have benefitted from Rand weakness.

He points out that many investors may have this exposure through portfolios such as Multi-Asset portfolios that can allocate assets to foreign stocks. Also, many companies on the JSE do have exposure to markets other than South Africa so this provides some additional diversification.

“If, however, you were invested predominantly in a portfolio with insufficient diversification, such as a sector-specific fund investing only in Financials or a domestic-only fund, then you should re-evaluate whether your strategy truly will be able to withstand significant turmoil. If you have doubts, contact your financial adviser to take the appropriate corrective steps,” he says.

He adds that while the downgrade initially impacted negatively on certain sectors such as Financials, other sectors such as Resources and Industrials (particularly the Rand hedges) have seen significant gains.

“Investors who are appropriately diversified are more likely to absorb the impact of the downgrades over time. If you weren’t already appropriately diversified, heed this as your wake-up call, check in with your adviser and adjust your financial plan accordingly,” he says.

3. Consider your retirement plan carefully

If you are nearing retirement, consider delaying your retirement if possible since each extra year worked is one year less to rely on your savings.

“Boosting your retirement savings and lessening the amount of time you will need to rely on these savings could have a profound impact on your retirement outcome.”

He urges investors with living annuities to ensure that they are maintaining a sustainable drawdown level, as preserving their retirement capital will increase their financial resilience to withstand lower returns.

“A sustainable percentage will depend on your age, gender and marital status, but should not be more than 4% for someone newly retired at the age of 65 years,” he says.

4. Boost your savings

With the cost of living expected to rise and interest rates likely to increase, Davison emphasises that it is vital that you build resilience into your finances by carefully managing your expenses and prioritising your savings.

“Pull back from spending to the limits of your income and save at least six months’ salary as a buffer against unforeseen expenses or financial shocks,” he suggests.

He warns that tax rates may also rise as a result of additional pressure on the government’s budget, and suggests taking advantage of tax incentives through additional contributions to your retirement fund or to a tax-free savings account.

He notes that the returns from tax-free savings accounts are exempt from income tax, dividends withholding tax or capital gains tax. The limits for contributions have also been increased to a maximum of R33 000 per year from 1 March 2017, with a lifetime limit of R500 000.

“With incomes likely to come under pressure, seize this opportunity to tighten the reins on your finances,” he says.