Investment themes for 2019

Maitse Motsoane, Portfolio Manager at Prescient Investment Management

2018 was a challenging year for risk assets. In fact, the sell-off in financial asset prices was so broad that it virtually left no place to hide - apart from cash - as 90% of asset classes generated negative returns.

Each year around this time, there is a plethora of predictions from economists and strategists charting financial markets’ roadmap for the year ahead. Of course, predicting anything in the markets over such a short time frame is incredibly difficult. For example, at the beginning of 2018, a lot of these forecasts called for double-digit gains in stocks, supported by synchronised global growth, pro-cyclical fiscal stimulus in the US and a weakening US Dollar. However, with the benefit of hindsight, we now know that a lot of those forecasts couldn’t have been further removed from what actually transpired during the year.

So, we’ll resist the temptation of making predictions, focusing instead on understanding the key themes that will have a bearing on financial asset prices throughout 2019. In addition to regularly evaluating and testing the robustness of our investment strategies, at Prescient we carry out a risk survey that runs across teams to help us hone in on the themes we believe are worth paying attention to.

Slowdown in global growth

The US has experienced robust economic expansion in recent years - buoyed by the current administration’s looser fiscal policy stance . Should US growth continue on its current path through mid-year, this will become the longest stretch of uninterrupted expansion.

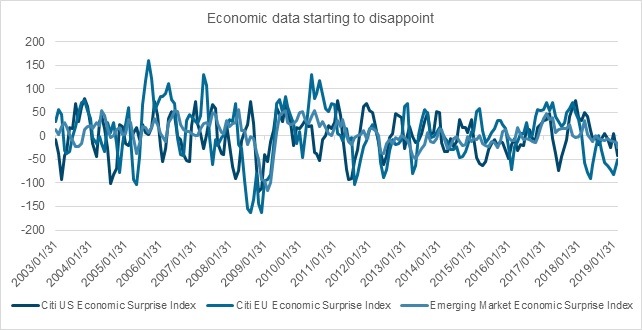

With the US unemployment rate sitting comfortably below the NAIRU (non-accelerating inflation rate of unemployment), and growth well beyond potential, late-cycle market tensions certainly will develop. That said, nascent signs of an impending slowdown in global growth are not in short supply. Evident from the graph below is that economic data prints have been disappointing across key regions including the US, Europe and China since 2018 – evidenced by the various economic surprise indices that have all but rolled over in tandem.

Source: Bloomberg

The fiscal impulse by way of tax cuts and spending increases that accelerated growth in the US is expected to wear off by 2020. And with a divided congress post the mid-term elections, additional growth-enhancing legislation that the administration might have hoped to pass will likely be thwarted by the Democrats in the House of Representatives.

In addition, China’s economic growth is also slowing down. Admittedly, the Chinese authorities have been pulling fiscal and monetary policy levers to support growth. However, one needs to appreciate that these policy measures are not designed to re-steepen the growth trajectory, but rather to cushion the blow of a slowdown. As such, the Prescient Economic Indicator that measures deviation from the long-term growth trend is also signaling softer global growth.

Figure 2:

Source: Prescient Research

The question then becomes; when does the music stop? As allocators of capital grapple with determining appropriate positioning for the current stage of the economic cycle, financial markets have started to signal poor global prospects. The indicator that has drawn the most attention as a precursor to recession is the US yield curve inversion. The lack of compensation for taking term risk highlights muted inflationary pressures and, by extension, expectations of slack economic growth going forward.

Transitioning to quantitative tightening

With the US Federal Reserve (The Fed) contracting its balance sheet, and the European Central Bank (ECB) halting asset purchases at the beginning 2019, the world is transitioning from quantitative easing (QE) to quantitative tightening (QT).

QE bolstered risk assets for a decade, suppressing volatility to historically low levels. With QE now drawing to an end, volatility has started to pick up once again. Last year was important in terms of Fed policy normalisation, but this is still work-in-progress. The retraction of the monetary largesse of the past decade implies normalisation of the pricing of risk. This will most likely result in wider credit spreads, the de-rating of equity valuations and tepid inflation.

However, softening global growth seems to have stymied major central banks’ ability to tighten financial conditions. Consequently, we’ve seen central banks capitulating on previous commitments to tighten policy, tilting to an easing bias or maintaining levels of accommodation that are already in place. Policymakers would certainly feel more comfortable going into the next recession with policy rates at higher levels – which would afford them room to lower borrowing costs as they attempt to soften the blow of an economic downturn.

We’re certainly in unchartered territory here, with no easy answers as to what the most appropriate course of action should be. Policymakers need to strike a delicate balance between policy normalisation and ensuring that their actions do not slam the brakes on global growth – a task that may very well prove elusive given the current stage of the global economic cycle.

The rise of populism

To an extent, the roots of the current wave of populism that’s sweeping across the globe can be traced back to the global financial crisis. Ten years ago, the Fed’s Ben Bernanke launched QE as the global economy faced the real prospect of another Great Depression. In essence, he was underwriting the wealth of the baby boomers.

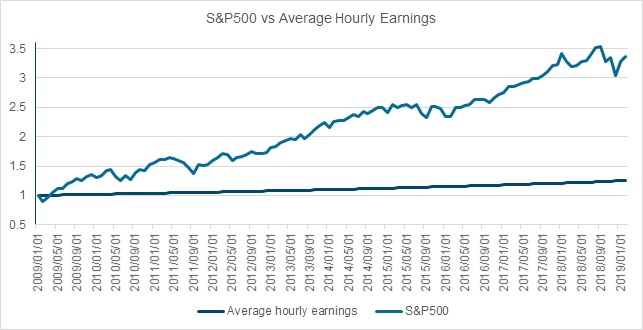

The subsequent rally in asset prices has meant that the asset-rich older generation benefitted at the expense of the those who depend on wages, generally millennials. With asset price growth far outstripping wage growth, it has become harder for millennials to acquire assets – weakening their stake in society in the process. This, in turn, threatens the tacit social compact, which is based on the notion that the faster the economy grows, the better off everyone becomes. The graph below illustrates month-on-month S&P500 growth versus average hourly earnings growth since the beginning of 2009.

Source: Bloomberg

From this, we can deduce that the classic demand-driven growth model – whereby productivity growth drives wage growth, which then fuels demand - has been fractured. It has become evident that economic expansion over the past decade was mainly a function of excess liquidity provided by major central banks. Put simply, taxpayers helped avert total calamity through the government’s bail-out of key financial institutions at the height of crisis, yet the subsequent expansion mostly benefitted the asset-rich minority.

Consequently, a rise in populism has rattled the global political establishment. From the Brexit referendum outcome and Donald Trump’s ascension to the White House, to Italy’s standoff with the EU commission over budget concerns, the man and woman on street are undoubtedly staging a pushback and challenging the status quo.

The key question that arises is whether these sorts of populist policies will gain legitimacy, or whether market participants will punish them by selling assets across the different regions that find themselves engulfed in this cloud of populism.

Trade conflicts and protectionism

The Sino-US trade dispute drew the attention of most market participants over the course 2018, and a lot of the weakness realised in cyclical assets’ performance is a direct consequence of that. Indeed, when the two largest economies in the world lock horns, it becomes difficult to paint a picture where the global economy emerges from the stand-off unscathed. Beyond tariffs, quotas and potentially even trade embargos cannot be ruled out over the long-run.

The US’s aspirations for its relations with China go far beyond trade. High up on the agenda, are issues like controlling China’s ability to challenge the US’s dominant global status, particularly as it relates to new technological development and concerns around intellectual property transfers by US companies operating in China. This complicates matters as the US attempts to address a myriad of issues in what is supposedly a trade negotiation.

Similarly, we’ve seen tariff threats levelled against automakers in Europe and Japan. And as negotiations between the US and China continue to ebb and flow, any form of resolution between the two countries will likely give way to a rise in trade tensions between the US and other high-surplus countries such as Germany and Japan.

With Donald Trump’s election as President of the US, protectionist rhetoric has become more threatening and strident. It therefore becomes imperative for those who wish to promote a sustainable, inclusive, dynamic global rules-based multilateral agenda to pull together and rally forces. This is a critical situation, not without the possibility of things getting much worse.