Investment outlook – major themes for 2015

Tristan Hanson, Head of Asset Allocation at Ashburton Investments.

The dawn of a new year brings with it many traditions and so too in the investment world, when strategists, economists and fund managers alike look forward to what might or might not happen in the year ahead.

Should we need any reminder, 2014 illustrated how much of what happens is unexpected: how many forecasters this time last year predicted the Ukraine crisis, the emergence of ISIS, a far-reaching Ebola virus scare, a collapse in the oil price and the US 10-year bond yield ending the year over 80bps lower?

So things will almost certainly pan out differently to how we expect, sometimes very much so.

But acknowledging this is not a reason for inaction, nor is a new calendar year different to any other time: investing is always about considering what the future could hold and how various risks (scenarios) are priced. A fund manager’s job is to generate investment returns, not predict future economic events (there is an important difference). His or her primary concern is therefore to assess what risks are already priced and how markets might react to various scenarios were they to occur.

And so, in accordance with New Year tradition but in full knowledge that the future is highly uncertain, we provide our thoughts as to what may be some of the major themes in the year ahead. Note that we have excluded geopolitical events but with tensions evident in many countries (and just below the surface in others), geopolitics is likely to remain a risk factor to watch closely.

We conclude with our current asset allocation stance, which represents our best investment view today in the world as we see it.

1. Low inflation, reasonable growth & low interest rates

2. Monetary policy divergence

3. US dollar strength

4. Moderating Chinese growth

5. Delivering the promised reforms

6. Consequences of a lower oil price

7. Political risks in Europe

8. UK general election uncertainty

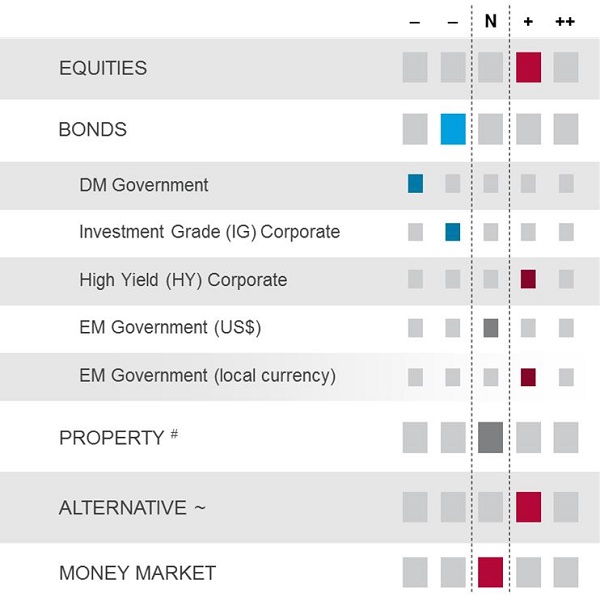

Asset Allocation

Table 1 below provides an overview of our main asset allocation views.

We continue to favour equities over bonds within our Multi Asset Fund range, although we expect overall global equity returns to be more muted in the next five years compared to the previous five when they averaged around 10% (nominal USD terms).

Reasonable global GDP growth, low inflation and loose monetary policy continue to provide support to the equity market. On the flipside, after considerable gains in recent years valuations are not depressed (as they once were) and the process of US interest rate normalisation may create bumps in the road. The increased volatility experienced in the second half of 2014 may provide something of a broad roadmap – while global equities make upward progress in local currency terms the journey may be far from comfortable at times.

Developed market government bond yields at current levels are very unattractive for the medium-term investor. German bonds already price in an interest rate environment very much like that which Japan has endured for more than 15 years. Meanwhile, the sovereign spread of European periphery government bonds is the lowest since the Greek crisis first erupted. US yields remain higher in absolute terms but do not offer value, in our view.

Corporate bond spreads widened in the US in 2014, especially in the High Yield sector where energy companies have a larger weighting. With yields now higher we retain an overweight position in US High Yield. The outlook for defaults in the energy sector (where the majority of spread widening has occurred) will most likely determine returns for the overall US index, with default rates likely to be low elsewhere. This issue remains a key focus for us and we retain the flexibility to change our views if our analysis warrants it.

Emerging market bonds exhibited considerable volatility in December, first selling off then rallying strongly back to close to previous levels. We retain positions in Indian and Mexican local currency bonds, where we think yields look reasonably attractive given expected interest rate and exchange rate dynamics. We have limited exposure to dollar denominated EM sovereign bonds and we await tactical opportunities that periodic weakness may throw up.

In terms of currencies we expect the US dollar to appreciate against the other major developed market currencies (yen, euro and sterling) for the reasons cited above. The euro remains under pressure given fragile economic conditions and likely further monetary stimulus. Sterling is likely to be weighed down by election uncertainty and the drag exerted by the euro since the euro area remains the UK’s largest export market. Many EM currencies depreciated sharply in late 2014. From current levels, the higher yield on offer in some countries may provide a positive total return for US dollar-based investors even if the nominal exchange rate depreciates modestly. India is a country where we think this is a reasonable expectation, for example.

Table 1: Asset Allocation Views

# Relative to strategic internal benchmarks

~ Specifically refers to UK infrastructure assets

Source: Ashburton