Investment Note: Deciphering Dollar Declines

Apart from a brief slump in April, global equity markets have mostly taken the policy chaos coming out of the US in their stride.

The US benchmark S&P 500 is back at record highs, in part due to AI optimism, and also because investors still think that President Trump’s tariff threats are just bargaining chips. The trade deal with Japan and the EU is case in point, lowering tariffs from the 25% he had threatened to 15%. However, 15% is still very high, and if this is where US tariffs will settle across the board, it will raise the effective tariff rate on US imports to a level last seen in 1930.

It is notable that the US dollar has continued falling even as equities and to some extent bonds, recovered. This is despite economic theory suggesting that the currency of a country imposing high tariffs should strengthen since it will be importing less.

Why is this the case and what does it mean? We all know that the dollar is not like other currencies and there are at least three important lenses through which to think about the dollar’s relative position: its role as global reserve currency, its day-to-day use in global finance and commerce as well as its value in foreign exchange markets.

The demise of the dollar has long been foretold and feared, often in somewhat conspiratorial terms. As far back as 1968, an author by the name of William F. Rickenbacker published a book called the Death of the Dollar. It was not the last in a genre that often blames inflation and government borrowing for the impending disaster, but these days a deliberate policy of “de-dollarisation” by US opponents also figures prominently.

Reserved

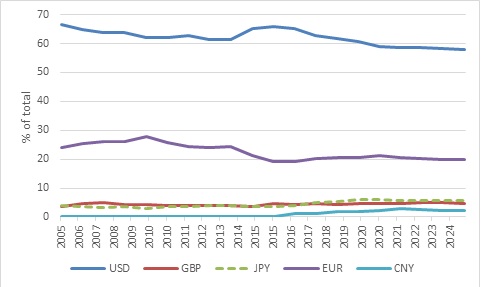

Let’s start with the dollar’s role as a reserve currency. This simply means it is the main currency of foreign exchange reserves held by central banks and other monetary authorities. Countries hold foreign exchange reserves, including gold, as a sort of rainy day fund to ensure continuity in their international economic relations. This includes being able to service foreign debt, import necessary goods and services, such as fuel, and maintain confidence in the exchange rate. For instance, if importers cannot source dollars they need privately, or if a bank struggles to find dollars to repay a foreign loan, the central bank should be able to sell them the dollars (or euro or yen) in the interest of broader economic stability. With a stockpile of dollars, a central bank can also stabilise its own currency by buying it on foreign exchange markets.

It makes sense, therefore, that the composition of foreign exchange reserves should broadly match a country’s international economic relationship. The dollar maintains the largest share of reserves, even though the US only accounts for around 9% of global trade. This is partly because a large percentage of global trade is still conducted in dollars (notably commodities), and partly because US capital markets are simply larger and more liquid than anywhere else.

Chart 1: Composition of global foreign exchage reserves

Source: International Monetary Fund

The accumulation of reserves globally increased dramatically in the wake of the Asian Financial Crisis of 1998 when countries in the region, spooked by massive capital outflows and economic devastation, started building up a stockpile of US dollars to ensure that their currencies would not come under speculative attack again. China, in particular, also accumulated dollars to prevent the yuan from appreciating too much, thereby undermining its export machine. However, the rapid growth in foreign exchange reserves has largely petered out since 2013. This is partly because the major central banks now offer swap lines to other central banks, meaning that the Federal Reserve, for instance, will swap dollars for other currencies in times of crisis, reducing the necessity for hoarding dollars.

Limited competition

The obvious competitors for the dollar as reserve currency, the Chinese yuan (also known as the renminbi) and the euro, each suffers from a major flaw, limiting their potential role. In the case of the euro, it is the lack of a large and liquid common bond market. Each of the 19 members of the euro have their own relatively small bond market and investors take on national credit risk in the process (Germany’s has a different risk profile to Greece and Italy, for instance). While there is a market for bonds issued by the European Union and backed by the joint fiscal capacity of member states, it remains relatively small. China, on the other hand, has a big bond market. The problem is that the yuan is not fully convertible and getting money in and out of China is not straightforward. As much as the Chinese government talks about a global role for the yuan, its policies still have the opposite effect.

Central banks have increased gold holdings, but the gold market is also relatively small. All of this suggests that the ongoing decline in the dollar’s share of foreign currency reserves will be gradual. But does this matter? Over the past 12 years, the dollar’s share of global reserves fell and total reserve accumulation slowed. Nonetheless, the dollar’s exchange value increased as chart 2 shows, suggesting that reserve currency status has not been a major factor driving the dollar’s value. A gradual loss of reserve currency status could have an impact, but it also might not.

Click here to read more...