Investing in an infected world

Friday marked day 126 of lockdown in South Africa. For many, the days and weeks are blurring into one another and the end of the month might have gone by unnoticed. But here we are at the start of a new month, August, and investors have an opportunity to reflect on how returns are shaping up after seven rather crazy months.

Once again, the overall assessment is simply that returns have been surprisingly good given the extent of the economic damage here and abroad, as well as the deep uncertainty still caused by the coronavirus. Its spread continues unabated, even in places like Spain, Australia and of course the US that enjoyed initial success in flattening the infections curve.

In South Africa too, the national curve is still rising, but in the Western Cape the worst appears to be over. While there is no vaccine yet, we know a lot more about treating and preventing Covid-19 than a few months ago, and this should prevent further hard lockdowns here and abroad.

Economic damage

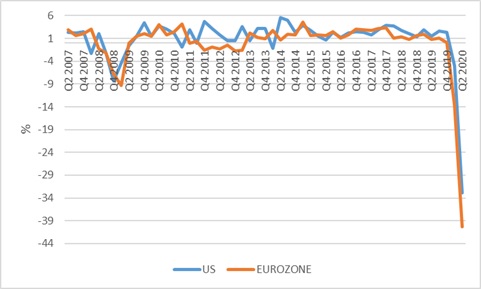

We also now have a good idea of the economic damage caused by Covid-19. Broad economic activity (as measured by gross domestic product) collapsed in the US and Europe in the second quarter. In both the US and Eurozone, GDP declined at the record-breaking annual pace of 32.9% and 40% respectively. (Notice on chart 1 how the so-called Great Recession of 2008/09 pales in comparison). We can expect to see declines of a similar magnitude when the South African data is released next month.

Chart 1: Annualised quarter-on-quarter economic growth

Source: Refinitiv Datastream

What matters now is the shape of the recovery, since activity bottomed in April or May in most countries with the lifting of stay-at-home orders. In the US, Federal Reserve Chair Jerome Powell noted that with concern evidence that the initial bounce had run out of steam largely due to the renewed outbreaks. He was speaking after the US central bank kept its ultra-accommodative policy stance unchanged. He noted that the Fed was not even “thinking about thinking about” raising interest rates from near-zero levels, and this would remain the case until convincing evidence of a sustained rebound in growth and inflation.

Together with his peers at other major central banks, Powell’s actions intervention stabilised markets after the chaotic sell-off in March and set the stage for a recovery. Large doses of fiscal support – governments injecting money into the economy – have also played a key role. Some of that support (an additional $600 per week unemployment benefit) lapsed in the US last week, which is a concern to Powell and most economists, but support is ramping up in Europe and is maintained elsewhere.

With central banks providing a backstop, and with little competition from the miniscule yields on bonds, the recovery global equity markets have been impressive even though the past week has been wobbly. The overall market is pricing in the recovery of earnings to pre-pandemic levels next year, ignoring the intervening months of earnings declines. This might be an ambitious assumption. Having said that, the usual suspect US mega tech stocks reported blockbuster earnings in the past few days. For instance, Amazon doubled its after-tax profits in the second quarter to $5 billion. Apple also had a record quarter in terms of revenues, up 11% from a year ago.

Clearly the pandemic has created winners and losers. The shares of companies that facilitate working, shopping and playing at home surged, and those dependent on people being out and about are still well below pre-pandemic levels.

While the MSCI All Country World Index returned 5% in July in US dollars and -1% year-to-date, the leading IT sub-sector returned 5.8% in the month and 21% year-to-date. In contrast, the energy sub-sector is still down 37% in the first seven months of the year.

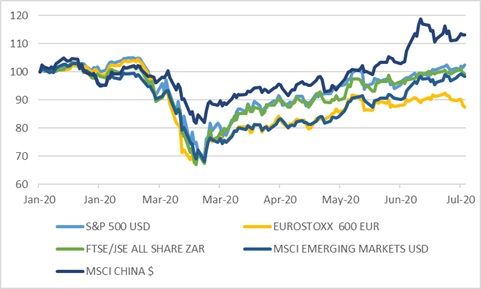

Chart 2: Major equity indices in 2020

Source: Refinitiv Datastream

Among major economies, the US market continues to lead the pack. The S&P500 returned 5.6% in July in US dollars and is positive year-to-date with a 2.4% return. European equities were apparently hamstrung by a stronger currency in the month, with the Eurostoxx 600 marginally negative in July in euros, and still -12.6% year-to-date.

Led by China, the MSCI Emerging Markets Index returned 9% in dollars in July, and have clawed back most of the losses of 2020.

Golden moment

To this list of winners and losers, we can now also add gold to the former column and the US dollar to the latter column. Gold spot prices surged 10% in July, surpassing the previous record set in 2011 to close the month at $1955 per ounce. Collapsing real yields make gold a more attractive asset, but we can also assume that more investors are drawn to the yellow metal simply because it has done well. In real terms, the price is still below 2011 and 1980 peaks, so it is too early to describe it as a bubble. It is also means, however, that gold is not as fantastic an inflation hedge as many believe.

The dollar lost 5% against the euro in July – an unusually large move – while the trade-weighted dollar index has pulled back to 2018 levels, but remains strong relative to its long-term history. The weaker dollar might just be a temporary reflection of America’s shambolic handling of the coronavirus (the latest in a long list of Trumpian debacles), but a number of long-term supports have folded. Most notable is that the interest rate gap between the US and its partners has largely disappeared, while the Fed has been more aggressive than most of its peers in supplying dollar liquidity to the markets through bond purchases. This while the already-large US budget deficit is growing faster than that of its peers. However, the greenback retains its status as the ultimate safe-haven and should benefit from any renewed bouts of risk aversion or crisis.

Chart 3: Trade-weighted US dollar index

Source: Refinitiv Datastream

If the dollar was to further weaken substantially, it should be positive for the world economy in general, and emerging markets and commodities in particular. The world still largely runs on dollars and funds itself in dollars and therefore a shortage of dollars (as indicated by a strong exchange rate value of the dollar) constrains economic activity.

On the home front

While South Africa no longer features as a top gold producer, there is perhaps still a bit of a halo impact. Still, stronger commodity prices and the weaker dollar supported the rand during the month, gaining as much as 4% against the dollar in the month, before retracing somewhat to close at R17.03 or 2% stronger. It lost 3% and 4% respectively against the euro and the pound in July.

The rand is still 21% weaker year-to-date against the greenback and 20% over one year, boosting offshore returns for local investors. However, the gap between the rand returns of local and global equities is closing.

Local equities also had a positive month, despite the absence of much good news during July. A 25bps interest rate cut is not going to move the needle, and despite much gnashing of teeth, the $4.2bn IMF loan finalised last week was pretty much a formality. It has been on the cards for the last three months at least and makes sense given the low interest rate. In the current emergency we face ourselves, worsened by a decade of poor fiscal choices, pride should not stand in the way. The only pity is that the money flows at a stronger exchange rate compared to a few months ago. All an all, the economic news has been poor, though we are only getting a sense now of the deepest point of the recession, given the lags in data releases. It will take some time to get a sense of how well the economy is busy climbing out the Covid hole.

The FTSE/JSE All Share Index returned 2.6% in July and has clawed back most of the year-to-date losses. In dollar terms, local equities have beaten global equities by some distance. As with global markets, there have been winners and losers. Unsurprisingly, resources have led the way with a 9% return in July, lifting year-to-date gains to 15%. The JSE’s gold mining index has more than doubled in 2020, and is up almost 200% over the past year.

Industrials increasingly have little to do with industry and indeed with South Africa, as the sector is dominated by global consumer companies. As is the case with its US counterparts, Chinese tech giant Tencent has benefited from stay-at-home activity and its dollar share price has surged. This has boosted its minority shareholder Naspers. It and rand hedges have benefited from currency weakness too.

In stark contrast, financials were flat in July and are still down 31% year-to-date. Financial shares tend to be more focused on the domestic economy than industrial or resources.

Bonds were marginally positive in the month and, despite the dramatic sell-off in March and accompanying foreign outflows, clung on to a 1% positive year-to-date return. That is the benefit of the high starting yield: the interest income has offset capital losses on the All Bond Index. The 10-year government bond yield ended the month virtually unchanged at 9.4%.

Yields elevated

Bond yields remains elevated, compared to recent history, other developed and developing countries and also compared to short-term rates which have declined as a result of the Monetary Policy Committee’s 300 basis point in repo rate cuts this year.

While cash has beaten bonds in 2020, looking ahead it might not be the case given that returns are drifting lower due to the rate cuts.

Inflation in June was 2.2%, a touch higher than in May. This was largely expected given the somewhat higher petrol price. However, core inflation, which excludes volatile food, fuel and energy prices, declined further to 3%. A big driver was lower housing costs, measured as both actual rental inflation and 'owner's equivalent rent,' i.e. the rent homeowners implicitly pay themselves. Rental increases have slowed to below 2% from a year ago, and could well turn negative, given an expected increase in vacancies. Inflation is likely to average around 3% this year, rising somewhat next year. It means the real yield available from long bonds is substantial.

Thinking about the future

The great Howard Marks once observed that investing’s central problem is that all our knowledge is about the past, but all our decisions about the future. How can knowledge of the (recent) past inform our decision-making today? Three things stand out: there is no reason to expect the Covid-related political, economic and financial uncertainty to decline any time soon However, we’re unlikely to experience anything as jolting as that initial February/March shock.

Secondly, while central banks cannot prevent recessions and job losses and have no business eliminating market volatility, they have shown a determination to prevent financial market calamity. Lastly, for all our problems here in South Africa, global market conditions will dominate domestic financial markets. For the most part, the outlook for rand, the JSE and bonds depends on global risk appetite. Local asset classes offer value and, with a supportive global backdrop, can deliver real returns.