Investing for income and growth amid increased risk

South Africans have seen exceptional investment growth in the recent past, but the benign market environment is not likely to continue, according to Coronation Fund Managers.

As valuations appear stretched and the risk of volatility increases, the focus for investors close to retirement should be on managing risk, says Charles de Kock. He co-manages Coronation’s flagship income and growth funds, Coronation Balanced Defensive and Coronation Capital Plus with Henk Groenewald. Balanced Defensive1 is a multi-asset fund for cautious investors requiring stable returns, while Capital Plus2 is focused on maximising long-term returns while minimising short-term risk.

The domestic equity market is looking expensive. The JSE’s price earnings ratio is currently close to 19 times, compared to the past 55-year average of 12 times. Historically, investors who bought the market at an average of more than 17.5 times earned a negative average return over the following year.

Income assets are also likely to deliver a weaker performance, with cash already yielding a negative real return. When bonds and preference shares are taken into account, inflation plus 2% may be the best return to be expected from an income investment for the foreseeable future.

While foreign equities still appear comparatively cheaper than the domestic market, future returns from these assets may also be weaker than in the recent past. The dramatic decline in the rand has bolstered foreign returns, but another sharp currency slump is not expected.

Against this background, Coronation’s income and growth funds (Balanced Defensive and Capital Plus) are further reducing risk and diversifying across asset classes. Says Groenewald: “We carefully consider all scenarios and look at the potential downside of investments.”

For the first time in the past five years, the funds are investing in government bonds. Cash holdings have also been increased, which will allow the funds to invest in favourable opportunities should they arise.

While local equities are expensive, both funds have invested in a number of shares that offer defensive qualities and very sound business cases. These include Old Mutual, Pioneer Food Group and Spar. Both funds have also increased their holdings in the property group Attacq, as well as in selected banks. (As low-risk portfolios, neither the Coronation Balanced Defensive fund nor Coronation Capital Plus had any exposure to African Bank.) Holdings in Anglo, BHP Billiton, MTN and AVI have been reduced.

1. The Coronation Balanced Defensive Fund has delivered an average return of 11.6% per annum since its launch in 2007.

2. The Coronation Capital Plus Fund has yielded an average of 14.7% per annum since its launch in 2001.

Performance figures quoted for the period ending 30 June 2014.

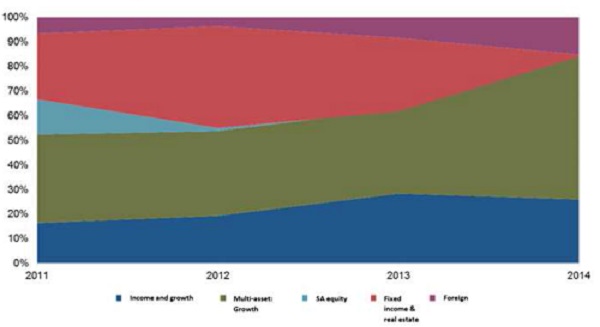

Given the prospects of lower investment returns and increased volatility, investors – particularly those close to retirement - should take note that the current environment makes the case for a more conservative asset allocation, says Pieter Koekemoer, Head of Personal Investments at Coronation Fund Managers. However, the recent buoyant market returns have seemingly whet investor appetite for riskier assets. Industry figures show a sharp increase in the share of living annuity portfolios that are not compliant with Regulation 28 (from 19% in 2012 to 25% to 2013), indicating a greater-than-permitted exposure to equities. This is consistent with the trends seen in cash inflows across the unit trust industry. Investments in fixed interest funds have dwindled and investors seemingly skipped the next risk bracket (income and growth funds) to invest instead in high-equity multi-asset growth funds. (See figure 1.)

It bears reminding that these multi-asset growth funds are focused on long-term gain and not mandated to manage volatility through bad years, says Koekemoer. In contrast, income and growth funds offer a balance between reasonable long-run expected returns and near-term capital stability. The latter is particularly relevant for the retirement class of 2014 and 2015, who will be most vulnerable to any possible market loss in the coming months.

Figure 1: Share of net inflows by mandate type in the SA Collective Investment Schemes (CIS) industry

Source: Morningstar, ASISA, Coronation Research