Investing amidst persistent uncertainty

“Read last year’s market predictions and you’ll never again take this year’s predictions seriously.” – Morgan Housel

2023 is certainly proving to be a year that no one anticipated, with global equity markets – led by the US – producing returns that not many saw coming. In fact, at the beginning of the year, the consensus view was that the US would enter recession later this year or early in 2024. Yet, a week or so ago, JPMorgan changed its view from one of US recession to no recession. If market commentators are to be believed, Jerome Powell and Co are likely to pull off the impossible by raising rates at the most aggressive pace in modern history while avoiding a recession – a feat that has never been achieved.

If anything, this year reinforces the view that short-term forecasting is a fool’s game. And for those who are still not convinced and are wanting to forecast where markets are going from here, it would be relatively easy to argue both sides of the coin. On the one hand, equity market returns have been good, economic growth has been surprisingly resilient, unemployment remains low, consumers are in good health, and inflation continues to fall. The counter-argument largely looks to forward-looking indicators and valuations – markets appear to be expensive as a result of pricing in good news, manufacturing PMIs are showing weakness lies ahead and the Fed continues to tighten monetary policy. Consequently, sales growth is likely to stall and since we are at peak margins, earnings will also come under pressure.

Needless to say, choosing a side is difficult. The doom and gloom scenario has been touted since the beginning of the year but is yet to materialise. This has led to a sense of heightened uncertainty. However, the reality is that we live in a world of constant uncertainty and today is no more uncertain than it was five years ago. It just feels that way because we are living it today.

HOW WE GOT HERE

Understanding the drivers of the market through the course of 2023 provides a sense of how we arrived at this juncture. The regional banking crisis in the US in early March proved to be a pivotal point. The US Federal Reserve showed its hand by abandoning its quantitative tightening policy, pumping liquidity into the system to avert a banking crisis of greater proportions. The Bank of England came to rescue in similar fashion last year. Markets saw this as confirmation that central banks would come to the rescue at the first signs of strain. Additionally, the collapsing banks also created expectations that the hiking cycle would end sooner than anticipated. And with that, markets were off to the races, with the Magnificent Seven (large capitalisation technology stocks) doing the heavy lifting. Importantly, it is worth noting that research shows that over time, a disproportionately small portion of the market drives overall returns. Very often, these businesses are multi-national companies that are more linked to the global economy as opposed to the economy within which they are headquartered. Since the beginning of June, the broader market has played catch up. Perhaps a sign of overexuberance?

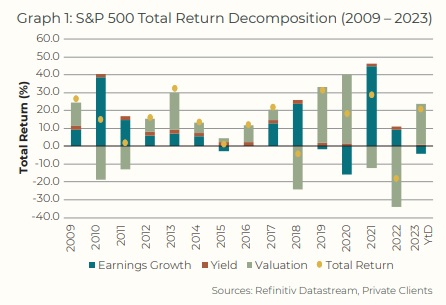

Given the above, it is not surprising that valuations have driven market returns this year. Graph 1 breaks down the S&P 500’s return into the three underlying drivers i.e. valuations, earnings and yield. As the second quarter earnings season comes to an end, it is clear that earnings growth has stalled and is now going backwards, a statistic that is skewed by energy and commodity companies. Nonetheless, it is clearly evident that valuations have widened significantly, and now we have to ask, what next?

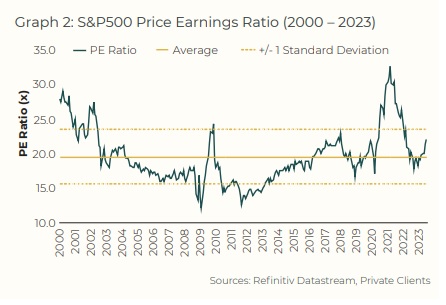

Graph 2 highlights the current US market valuation using the price-earnings ratio. Despite the limitations of such a valuation multiple, it does give one the sense that the US market is trading well above its long-term average. Coupled with the fact that the economic outlook is muted, with a soft-landing being the best-case scenario and interest rates unlikely to come down quickly in the foreseeable future, one has to conclude that the US equity market is looking vulnerable.

With the US market now accounting for 70% of global developed markets, it is easy to overlook many other parts of the world. Both Europe and Japan have performed well through the course of this year too. After many years of deflation, Japan inflation has been above 3% for the past 12 months. The Japanese equity market has been buoyed by the Bank of Japan maintaining its accommodative monetary policy through ongoing yield curve control. Meanwhile, European markets have been assisted by a strong euro, boosting dollar returns.

Furthermore, there are a number of longer-term thematic themes that are evolving around the world, which will have a significant impact on global equity markets in the fullness of time. The unexpected story of 2023 is the rise of artificial intelligence (AI). And while companies at the coalface of AI have benefitted so far this year, many other businesses that operate further along the technology chain stand to benefit as companies digitise and realise the full potential of AI.

Another story that is quietly developing is that of emerging markets. While the headline numbers show that emerging markets continue to lag their developed counterparts, an analysis of the individual countries tells a very different story. Similar to the US dominating developed markets, China dominates emerging markets. Exclude China and emerging markets appear to be doing quite well. Since the beginning of 2022, the bond and equity markets in Brazil, Mexico, Chile, Indonesia and India have all produced respectable returns, with a number of them outperforming their developed market counterparts. At the same time, their currencies have strengthened relative to the US dollar. In light of this, global investors should certainly be taking a closer look at emerging markets.

THE BOTTOM LINE

In closing, the global market is dominated by the US and from a bird’s eye view, the US market does appear to be vulnerable based on extended valuations and our current position in the economic cycle. However, the market has been narrow, with the broader market only recently starting to catch up. It is therefore important to look beyond the largest companies that dominate the headlines, as there are other themes, countries and businesses that also warrant investors’ attention.