Introducing the new kids on the investment block

If building a diversified investment portfolio is high on your list of resolutions for 2025, you should familiarise yourself with the new kids on the investment block. There are currently only 26 in the country, but if international trends are anything to go by, this will likely change in 2025 and beyond.

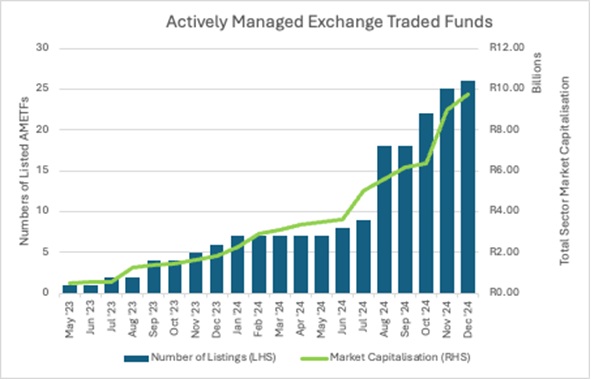

The first actively managed exchange-traded fund (AMETF) was listed on the Johannesburg Stock Exchange (JSE) in May 2023, following amendments to the JSE Listings Requirements.

As the name suggests, these new instruments are exchange-traded funds (ETFs). However, while a traditional ETF aims to mirror the performance of its benchmark index, the goal of an AMETF is to outperform the index. The AMETF asset manager strives to achieve this by cherry-picking shares.

At the beginning of August 2024, 10 AMETFs were listed on the JSE.

“By the end of 2024, the number of AMETFs available to local investors had more than doubled to 26, and this new type of investment vehicle is expected to continue to proliferate,” says actuary Mark Randall, a member of the Investments Committee of the Actuarial Society of South Africa (ASSA).

While AMETFs listed on the JSE held assets of R9.7 billion at the end of December 2024, assets in global AMETFs crossed the US$1 trillion threshold in August 2024.

Growth of AMETFs in South Africa

Source: Johannesburg Stock Exchange (JSE)

New-generation building blocks

Randall describes AMETFs as new-generation building blocks for investment portfolios with the investor protection that traditional collective investment schemes (CIS) such as unit trusts are known for.

“An AMETF is an innovative wrapper that combines the investment flexibility offered by CIS portfolios with the efficiency and transparency of listed securities. It is simultaneously a CIS and an Exchange Traded Fund, harnessing aspects of both to showcase manager expertise in a transparent and efficient structure.”

He points out that an AMETF must be registered as a CIS under the Collective Investment Schemes Control Act (CISCA), is governed by the JSE listing requirements, and can only be offered by a licensed provider regulated by the Financial Sector Conduct Authority (FSCA). The key difference between AMETFs and unit trust portfolios is that AMETFs are listed on the JSE.

Randall says this means that investors can buy and sell shares in the AMETF throughout the day via a share trading platform. Units in a unit trust portfolio, on the other hand, can only be bought or sold via a unit trust company or a linked investment services provider (Lisp), priced at the portfolio’s Net Asset Value (NAV), which is determined at the end of each trading day.

“The appeal of AMETFs lies in the ease of access, the cost efficiency of a listed instrument, client liability management via STRATE and the absence of minimum investment amount requirements,” explains Randall.

“Any investor who currently trades on the JSE equity market can also access AMETFs. Some investors may prefer this way of accessing discretionary funds over traditional platforms that provide access to the CIS market, for reasons including intraday price formation, platform independence, administrative efficiencies and service consolidation.”

He says advisers may also choose to include these instruments in their model portfolios. “Including actively managed funds alongside single equities and passive products across asset classes can provide a diversified portfolio of listed instruments on a single platform. AMETFs with no performance fees could also qualify as a tax-free savings account investment.”

Randall says a number of the 26 AMETFs currently listed on the JSE are classified as Global Portfolios that invest at least 80% of their assets outside South Africa.

“The fact that AMETFs are Rand-denominated does not necessarily imply domestic exposure. AMETFs classified as Global Portfolios offer investors the opportunity to diversify offshore without utilising their foreign allowance, without an additional layer of costs generated by exchanging currency, and without foreign platform fees.”

Randall explains that investors can expect AMETF fund management costs to be higher than those charged by traditional ETFs, which are generally cheaper because they are passively managed. An AMETF is likely to have a similar fund cost structure to a unit trust, and both have to publish the Total Expense Ratio (TER) and Net Asset Value (NAV) of the fund each day. The difference in costs relates to access fees, which consist of brokerage and other trading costs for AMETFs, and potential platform or provider fees for a unit trust.

More flexibility and choice for investors

Randall notes that while AMETFs do not necessarily bring any unique new advantages to the investor, they combine the features of a CIS with those of a listed investment product.

“This means an actively managed fund with a professional asset manager and a licensed provider–the trusted bedrock of the South African CIS industry today,” concludes Randall.