Infections and inflections

The world passed two notable Covid-19 milestones in the past week, one good and one grim. The good news is that a billion vaccine doses have been administered. It is simply staggering to think that in the space of only 15 months, scientists went from barely knowing anything about the new coronavirus to developing effective vaccines.

While the vaccines are not fool-proof, the evidence so far suggests they are doing a pretty good job. The world is unlikely to ever eradicate this coronavirus altogether, but if catastrophic surges that overwhelm hospitals can be avoided, it will be a massive win. Needless deaths can be avoided, as can further economic shocks. The main challenge now is logistical, securing enough supplies and getting jabs in arms as soon as possible. South Africa still lags on that score, with only 300 000 doses administered, but things should pick up pace in the coming weeks. Fortunately, there is no sign yet of a third wave here.

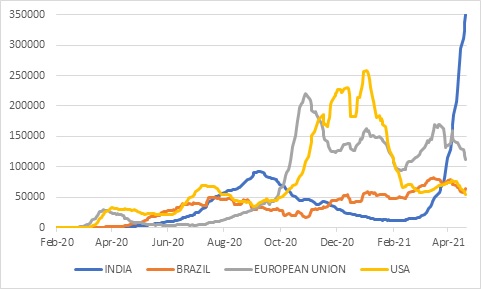

The bad news is that the daily rate of new global Covid-19 infections hit a new high in recent days. In other words, more people are currently being infected than at any stage in the past year. Yet optimism for global economic growth is also at a high, and stock markets have barely budged. What is going on?

Chart 1: Daily Covid-19 new infections

Source: Refinitiv Datastream

Indian nightmare

The surge in new cases is driven almost entirely by India, where a devastating second wave is now firmly underway. New infections in the US and Europe are reducing, but in India they are gathering speed. South America is also still struggling with high infection rates.

India was expected to be the fastest growing big economy this year, with the IMF forecasting 12.5%. That is now in doubt even though its government has announced few formal lockdown measures, unlike a year ago when Prime Minister Modi abruptly issued very strict lockdown orders, leading to millions of migrant workers having to walk back to their rural homes.

Unfortunately, it appears India’s government celebrated too soon after the end of the first wave, allowing massive gatherings and not preparing for a second wave. Nor has it placed much emphasis on vaccinations, despite being a major producer of coronavirus vaccines. Vaccinating hundreds of millions of adults across a vast sub-continent with patchy infrastructure is going to be challenging, to say the least.

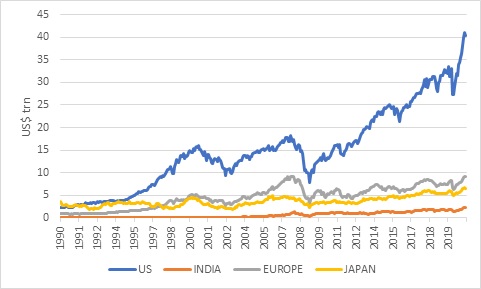

Although India is a big country, its impact on the global economy is less than that of Europe, the US or China. Its impact on financial markets is even smaller. The US accounts for more than half of global stock market capitalisation; Refinitiv puts the US market cap at around $41 trillion, compared with India’s $2 trillion. In other words, the entire Indian market is only as valuable as Apple.

Chart 2: Equity market capitalisation in US dollars

Source: Refinitiv

So what really matters for markets is first and foremost what happens in the US, followed by Europe, China and, to a lesser extent, Japan.

Humming

The US economy is humming. It grew at an annualised pace of 6.8% in the first quarter. In real terms, the economy is now slightly larger than a year ago before Covid hit. This is quite extraordinary and driving a massive profit recovery.

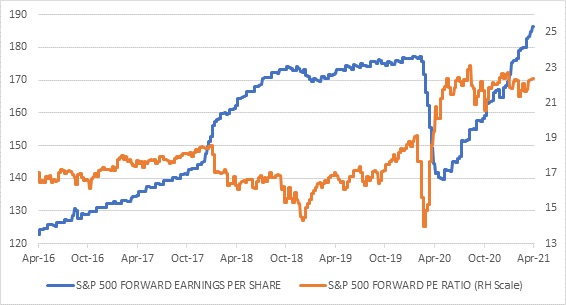

Corporate earnings in the first quarter are expected to rise 33% from a year ago. Most of the S&P 500 companies that have reported on their earnings are so far exceeding expectations. As you would expect, it is the more cyclical companies that are leading the earnings recovery, having been hardest hit a year ago. The consensus forecast for earnings per share over the next 12 months is $186, which would be well above pre-pandemic levels.

It helps that policy support is still extensive. The Federal Reserve reiterated a low-for-longer stance last week, noting that while the economic recovery is gaining momentum, the healing process still has a long way to go. This is particularly true for the millions of people who are still out of work or who have dropped out of the labour market entirely.

Headwinds

Apart from lingering Covid-related concerns, particularly the potential for nastier variants of the virus to emerge as it rampages along, there are three possible headwinds in the near term.

The global economic recovery is placing immense pressure on supply chains everywhere. Demand is overwhelming supply, partly because production was interrupted by lockdowns, and partly because producers probably did not foresee and therefore did not prepare for the boom. The result is rising input prices, particularly for raw materials. The copper price shot up to a 10-year high last week. Car companies cannot complete vehicles weighing hundreds of kilograms because tiny microchips are as scarce as hens’ teeth.

Input prices have to go somewhere. In the absence of rising productivity, they are either absorbed into margins, with shareholders and/or workers taking the knock, or they lead to higher selling prices, with consumers bearing the brunt (or some combination of the two).

So far, it is margins that face the squeeze, though consumers are also having to cough up more in many cases. Whether this will result in sustained higher inflation depends largely on whether companies can shift the burden from shareholders to customers on an ongoing basis without losing customers to competitors.

This has proven virtually impossible in the past decade or two and is likely to remain difficult. Consumers just have so many options today, and so many ways of instantly comparing prices at virtually no cost. Of course, in some categories, consumers have little choice. But this still doesn’t mean that prices over a broad spectrum of goods and services will rise at the same pace next year or the year thereafter. In other words, inflation rates should stabilise and are unlikely to continuously escalate.

Of course, companies that supply the inputs, particularly commodities, are laughing all the way to the bank. According to MSCI, the materials and energy sectors comprise 8% of global equity market caps, less than half of the sectors that typically use those inputs, namely utilities, industrials and consumer staples. Services – IT, health, financial and communication –dominate global markets with a combined share of more than 55%. This is because most mature economies are services led. Most of the scare stories about inflation relate to goods prices, but this is a relatively smaller component of consumer inflation.

The other headwind is proposed tax increases to fund US President Biden’s ambitious social and economic agendas. Partly it would entail raising the US corporate tax rate, which would affect American companies. But there is also a proposal for greater global cooperation to ensure multinationals pay their fair share wherever they operate, limiting the ability to book profits through tax havens.

This would be a positive development from a societal point of view, but society’s gain will be some shareholders’ pain. The proposed numbers are not massive, however, and analysts expect a single-digit knock to overall corporate earnings. Overall, the tax burden for US companies is still expected to be lower than four years ago, with then President Trump’s tax cuts not fully reversed. Some sectors will be harder hit than others. The big technology companies in particular have a reputation for profit shifting and utilising tax havens.

The last is simply valuations. Despite the strong profit recovery and healthy-looking underlying economic conditions, especially in the US, much of this was priced in some time ago. The US market trades at historically elevated multiples, putting the current index value over that $186 expected earnings over 12 months to a forward price earnings ratio of 22. Other developed markets are cheaper but not cheap. The best value is in emerging markets, including South Africa. But valuation is a poor guide to near-term returns. An investment can stay expensive or cheap for a long time. Valuations are much more useful at predicting longer-term (five plus years) returns. Nonetheless, current multiples suggest much of the returns have probably been front-loaded and we shouldn’t expect the juicy returns to continue indefinitely.

Chart 3: US S&P 500 12-month forward earnings and price earnings ratio

Source: Refinitiv Datastream

Set against that, of course, is what other asset classes offer. Central banks are promising to keep interest rates low, so cash is best avoided. The easy money has probably been made, but equities remain the place to be, given how low interest rates are across the world. Cash is still trashy, though when there is a correction it will shine for a brief moment. The one exception to this is South African longer-term bond yields, which remain very elevated, more than double the Reserve Bank’s targeted inflation rate of 4.5% over the next few years.

South African equities are also attractively valued, but we are a small market in the global scheme of things with concentrated exposure to commodity prices and Chinese technology in particular.

Sell in May and go away?

At the end of April, 12-month returns were still very strong. The best asset classes in rand terms has been local listed property with 41% and local equities with a 32% return. South African bonds returned 14%. The recovery in the rand over this period has put a lid on the strong dollar returns from offshore asset classes from the point of view of local investors. Global equity delivered 14% and global property 5% in rands.

These returns are unlikely to repeat, given that they are still measured off a fairly depressed base at the end of April 2020, shortly after the market’s inflection point. If we take a two or three year view that smoothes out the crash and the recovery, the picture is different. SA property is the one outlier on the downside, its problems clearly predating the pandemic. Global equity is the other outlier on the upside, led by the persistent outperformance of the US. Other asset class returns are decent but unspectacular. Nothing to suggest excess.

However, equity markets don’t move in a straight line, and therefore we should expect wobbles and corrections from time to time. Sometimes these are driven by new information that causes investors to change their assumptions, and often for no particular reason at all. The one lesson from all the craziness of 2020 is that these moves cannot be timed, and therefore trying to sell now with the hope of buying in after the market has dipped is not a good idea. These big inflection points can be predicted.

A better idea is to be properly diversified and rebalancing back to a well thought-through asset allocation. In that way, the winners are automatically trimmed, but you remain invested. Selling in May and going away has worked in the past sometimes, most notably in 2008, but usually it doesn’t. Staying invested does a better job over time, and it certainly did over the last year.