In search of Goldilocks

Over the past 15 years, the idea of a ‘Goldilocks’ global economy – not too hot, not too cold – has been on investors’ radar screens. In this environment, there is enough economic growth to keep company earnings ticking over, but there is no overheating that results in elevated inflation, forcing central banks to hike rates.

Clearly, Goldilocks has been absent of late, with the pandemic causing wild swings in economic activity, company profits, inflation and eventually, a surge in interest rates. Along the way there have been simultaneous bear markets in global bonds and equities, a rare occurrence. Could we be re-entering Goldilocks territory? Or are the bears about to return from their walk in the woods?

The rule of three

In storytelling, a ‘rule of three’ often applies. It is the idea that we understand concepts, situations, and characters better when they are grouped in three. Hence The Three Little Pigs, The Three Billy Goats Gruff, The Three Musketeers, The Lion, the Witch and Wardrobe and so on. In Goldilocks, there are three bears, obviously, but also three scenes of action: the kitchen, the living room, and the bedroom.

Let’s consider at a high level our own rule of three for macro analysis: the outlook for growth, inflation and interest rates.

Global growth

By far the biggest risk to investors with an equity-heavy portfolio is a global recession, more specifically a recession in the US, the most important economy for markets. Therefore, gauging the likelihood of a severe slowdown is priority number one. There is good news on this front.

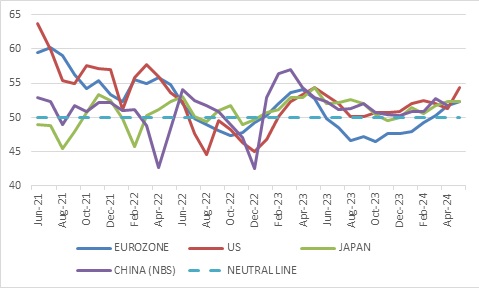

One of the timeliest indicators of global growth is the purchasing managers’ indices (PMI) produced by S&P Global. These are also constructed to be easy to read, with a level of above 50 indicating expansion.

S&P Global released the latest composite (manufacturing and services) PMI for the US last week, and it rose sharply from 51.3 in April to 54.4 in May, the highest level since April 2022. This suggests business activity remains healthy and risk of an imminent recession is low. The Eurozone PMI similarly rose to 52.3 in May, up from 51.7 in April. Japan’s PMI points to the fastest expansion in business activity in nine months. China’s latest PMIs will only be released in the coming week, but these too have risen in recent months, pointing to improved business conditions.

Chart 1: S&P Global Composite Purchasing Manager’s Indices

Source: LSEG Datastream

While one should consider a broad range of indicators to make a judgement over the health of the economy, the snapshot picture provided by these PMIs point to ongoing global economic resilience. Particularly important is that other major economies seem to be closing the gap with the US.

When the US is the strongest among major economies, it tends to result in a strong dollar which depresses growth elsewhere. When the growth momentum is more balanced between major regions, the dollar tends to ease and this in turn reduces pressure throughout the global financial system. Remember the dollar remains the international currency of choice for denominating debt contracts. The Bank for International Settlements estimates that dollar-denominated lending to non-banks outside the US amounts to around $12 trillion. When the dollar is strong, it effectively increases the burden of servicing this massive pile of debt.

Inflation

Inflation continues to decline in major economies, but unevenly so, with signs of stickiness in places. In particular, US service inflation remains elevated. This is partly because of strong demand for services, and partly because service prices are more exposed to wage pressures (wages are proportionally a bigger input cost for a restaurant than a factory, for instance). A third reason is simply that rental and insurance inflation as measured by the official numbers reflect the lagged effect of pandemic disruptions. Therefore, they should decline in the months ahead though it is taking longer than expected.

The pandemic also distorted labour markets, leading in the case of the US to the fastest wage growth in decades. This too is easing off as the market normalises. Further cooling will be necessary for the Fed to gain confidence that the inflation will indeed improve further.

Click here to read more...