Implications of China's currency move poorly understood

26 February 2014 | Investments | General | Steen Jakobsen, Saxo Bank

The market seems to be very sluggish in picking up on the implications of China's recent move to weaken its currency, with the Yuan now suddenly trading at its lowest level in months versus the US dollar.

My conclusion is this:

• China will slow down to 5 percent growth over the next two to three years;

• China will start devaluing its currency in response to Abenomics and China's weaker terms of trade;

• China will no longer be the world’s biggest investor and importer of investment goods.

This will have huge implications outside of China and in 2014; these developments will likely mean the following:

• Germany growth will turn negative (quarter-on-quarter) in the fourth quarter relative to the third quarter;

• World growth will come down from its recent 3.7 percent to less than 3 percent;

• The recovery projections will once again be postponed and the out-of-synch monetary policies of the major central banks will be questioned, leading to all-time new lows in interest rates;

• Deflation will take hold in Europe and become a major risk in the US;

• Equity markets need to be sold off. This comes after commodities sold off after the US banking and housing crisis, followed by fixed income during the late stage European debt crisis. Now I see a 30 percent correction in the second half of 2014 after a high is registered between current levels of 1,850 and 1,890 in the S&P 500.

China leads the world economy. It took the burden of supporting world growth in its hands during the peak of the crisis in 2008/09, with the largest fiscal expansion ever seen (nearly USD 600 billion). China also increased its investment-to-GDP ratios, which brought export orders for major European and US exporters until late 2013. But since the Third Plenary Session of the 18th CPC Central Committee in November 2013, the main objectives for the political elite in China have changed from growth for its own sake to rebalancing, fighting graft, reducing pollution and hoping that they can engineer a transition of their economic growth model with a smaller crisis now rather than a bigger one later.

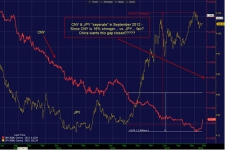

I have already spent some effort explaining why China is proactively seeking a small crisis rather than a big one and how China can no longer afford to keep its investment-to-GDP levels at excessive levels. Now, China seems to have embarked on a fundamental change to its currency policy with its move to weaken the renminbi. It's worth noting that China has been a strong critic of Abenomics and the resulting JPY devaluation as Japan and Korea remains its key export competitor. But until last week, China allowed its currency to continue higher in recent months — a side effect of a relatively tight monetary policy that was aimed at reining in bubbly credit markets. But now the focus has shifted back to the risks from a strong yuan and China's shift to weaken the currency is a pivotal new development:

Source: Bloomberg and Saxo Bank

With the present tensions between China and Japan, this chart is cause for concern for all of us: it now appears that China will no longer "play nice" and we have to wonder what this will mean for the US-China relationship. President Barack Obama's provocative decision to receive, once again, the Dalai Lama in the White House is not helping the situation. That the rally in USDCNY kicked off almost to the day Obama hosted the Dalai Lama is, of course, a pure coincidence (they met on Friday, February 20)!

China is not happy these days: the domestic economy needs rebalancing, with the risk that doing so upsets the population and those in the public sector who have benefited so handsomely from the status quo of the past several years. Overseas, Japan’s Abe is insisting on a stronger Japan, the US is "misbehaving" by talking to the Dalai Lama and the recent G20 meeting had the developed world blaming the recent slowdown on emerging markets.

It's certainly not been a good month for monetary policy coordination or friendly summits. The growing potential for a political crisis comes ironically at a time when stock markets across the world are reaching 7-, 14- or even all-time highs, as was the recent case of the US S&P 500 Index.

My old economic theory: The Bermuda Triangle of Economics remains in place. We've still got slow growth, high unemployment and high stock market valuations — all driven by a policy that only benefits the 20 percent of the economy that comprises large, listed companies and banks, who get 95 percent of all credit and access to policy subsidies. Meanwhile, the 80 percent of the economy that is the SMEs, who historically create 100 percent of all jobs, get less than 5 percent of credit and less than 1 percent of the political capital.

Markets and monetary policy

It’s the weather! The reason for the disappointing start to 2014 in the US is now all about the weather — well partly. I think most investors/pundits forget that the data for December and January was actually "born” three, six and nine months before due to impulses in interest rates and the overall cycle. As I have covered in the past, the slowdown in housing was "expected” in our models owing to the spike in mortgage rates between May and August 2013.

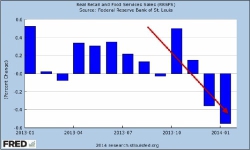

Elsewhere, the US consumer must have known the weather would be bad as far back as last summer judging by this retail sales (Mom) chart:

FRED Graph — retail sales US monthly change

US consumers remain two thirds of the economy, but they are still conservative: spending rose 2 percent in 2013 after 2.2 percent in 2012 and 3.4 percent in 2011. This is mainly due to low wage growth. Since 2010, the average after-tax income growth, adjusted for inflation, has only been +1.6 percent — to reach the magic 3 percent growth level, we will need wages to grow at least 3 percent on their own! This is not likely to happen in world of excess capacity, but nevertheless the pundits started the year with a 2.9 percent average expected growth for 2014. Now, one month into the year, the revisions are pouring in: the first quarter has already been reduced from 2.3 percent to 2 percent and the blockbuster Q4 growth of +3.2 percent is now expected to be revised lower to only +2.4 percent! Again, one has to laugh at how imprecise these measures are — we watch them, take decisions on them but ultimately their reliability is really only valid six months past the first announcement. Talk about looking in the rear-view mirror!

Strategy

Fixed income: still see new low yields in 2014 — mainly in Q4 — and into Q1 2015. ETF flows into fixed income are at USD 16bn year-to-date, which could be the largest inflow since 2002! Mainly prefer US and core Europe, although Italy's BTPs have done well with the political transition from Enrico Letta to Matteo Renzi as prime minister. My view on falling yields goes back all the way to last year.

Dividend yield is at 1.89 percent versus 2.72 percent and still attracts my money.

Equity: We have had a call for a peak in Q1 — admittedly I did not expect 1,850 to be broken, but my partner in Economo-physics still sees the chance of 1,870/90 before a top is in place. I submit our updated November 2013 forecast, which, slightly corrected, still stands. The risk reward looks compelling: the upside is perhaps 50 S&P 500 points versus 500 points of down-side potential. Remember that a 20 percent to 30 percent correction happens every four to five years — and a 10 percent correction occurs twice a year, on average.

FX: Overall, the USD should soon find support. The best long-term gauge of the USD is world growth minus US growth. Why? Because the USD is the reserve currency and often the currency of choice in trade. When world growth is slowing (now …) then the US and the USD need to pull ahead to fill the gap. We need to monitor the US Dollar Index over the next week or two as it's sitting on a major trend support line:

Conclusion

China has now joined the currency devaluation game as it jostles with others for some wind for its sails. But there is only so much wind to go around.