How to think about SA Inc. – Why perspective matters

Dirk Jooste, Fund Manager at PSG Asset Management

It can be extremely challenging for South Africans to distance themselves emotionally from debates around local investment.

Protracted loadshedding continues to weigh on the economy, the South African Reserve Bank (SARB) has slashed growth forecasts in response, and tax receipts are likely to be negatively impacted, putting further pressure on the fiscus. The political landscape remains volatile and uncertain, and the rand remains weak. There seem to be precious few positives that would indicate that improvement is possible any time soon, if at all. Amid all this negativity, why do many fund managers (of which PSG Asset Management is only one) continue to favour investment in SA Inc. stocks?

Viewing SA in isolation can cause a skewed perception of risk and reward

The noise levels facing local investors can be overwhelming. It is no wonder then that investors tend to focus on what’s wrong with SA: the list of issues facing the country is both long and very well documented. With danger signs posted everywhere, many conclude that the best course of action is to avoid investing locally and rather invest offshore.

However, focusing on risk to the exclusion of all other factors is dangerous. Investing is never devoid of risks. It is always a matter of ensuring that you are adequately rewarded for those risks, and that your holistic portfolio is robust and diversified enough to ride out the inevitable ups and downs. One of the most dangerous mistakes in investment is misconstruing a lack of volatility for a lack of risk. We see this repeatedly when investors flee to ‘safe’ cash investments during times of market upheaval but forget about inflation (a far greater risk for most!) in the process. In the fixed income markets in particular, we believe some have conflated lower volatility with lower risk in certain instruments that we would argue are, in fact, potentially far riskier than many realise.

Identifying risk correctly allows investors to price assets correctly. In our view, when you buy quality assets at depressed prices you have the best chance of long-term outperformance. Conversely, overpaying for assets – even if they are great companies – handicaps your ability to deliver outperformance in the long run. Thus, the key for us when it comes to investing in a risky asset, is:

• Ensuring risks (and potential surprises to the upside) are identified correctly.

• Focusing on the price paid: our 3M philosophy highlights the importance of investment at a margin of safety.

• Constructing portfolios in such a way that they benefit from diverse drivers of return and deliver sustained performance.

Considering the case for SA assets in a global context

As global managers, we highlight that emerging markets have experienced a decade without a positive cycle. The local equity market has also not fared well – not only due to idiosyncratic factors, but also because developed markets have been the investment of choice. This has been driven by very accommodating monetary policy and a decade of ‘easy money’. As market distortions associated with accommodative monetary policy and low interest rates globally unwind, we expect that the tailwind developed markets have enjoyed will start to evaporate. Investors buying into expensively valued global stocks are likely to discover that overpaying for assets – even if they are great companies – often leads to significant under-performance over the longer term. Investors often forget that US equity markets have previously traded sideways for a decade or longer – and can do so again. Not even global assets can escape the valuation reckoning indefinitely!

How best to approach investment in SA Inc. companies

We are deeply aware of the challenges facing SA. Since we run a globally integrated process, any allocation to SA must pass a potential return hurdle analysis. In multi-asset portfolios, cash returns are the starting point for our asset allocation process. Any instrument included in the portfolio has to be additive to a cash return on a risk adjusted basis. Whether this is a trade-off between cash and bonds, or between local and global assets, we believe that any investment is only merited when the rewards potentially outweigh the risks.

While the overall answer is “yes” to SA Inc. investments, we have not taken a blanket approach to the opportunity set and have carefully curated our exposure. We have chosen to favour companies that we deem to be resilient, competitive, producing good cashflows and that have strong balance sheets. This means we are not leaning heavily on a macro normalisation or the timing thereof, while being acutely aware that a normalisation of growth is likely to surprise investors given that valuations currently reflect almost no probability of an improved environment.

Also, the backdrop is not new: this tough macro environment has been around for more than a decade. The companies that have managed to survive and adapt have proven themselves to be very resilient. Those that have fallen by the wayside have exited the market which bodes well for the competitive landscape for the survivors. Coupled with this, SA has seen little capital investment meaning the profit pool or opportunity set is shared among fewer and fewer competitors, which bodes well for companies’ return profiles, and again should surprise on the upside.

Lastly, valuations are cheap. While the SA country-specific risk premium is appropriate, our assessment is that risk premia reflected in valuations in certain areas of the market are excessive.

To be sure, the energy situation is acute, but as the saying goes, necessity is the mother of invention, and we are starting to see a highly creative response from the private sector (households and corporates) in the form of non Eskom dependent solutions which are only starting to accelerate now. In the next two to three years this is also likely to surprise to the upside and alleviate some of the acute issues. It is to be expected in this challenging environment that investors are focused on the negative, and extreme narratives like a complete grid-collapse are testament to this. The odds of a more normalised scenario should also be considered. It is not unfathomable that the private sector builds energy solutions equal to 15% or more of total grid capacity in the next three to five years, significantly reducing the need for loadshedding.

Local opportunities abound

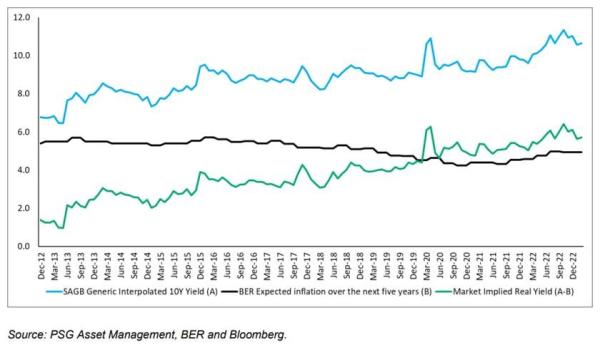

Investors looking to take advantage of the SA opportunity are spoilt for choice. With the 10-year government bond yield hovering around the 11% level and medium-term inflation expectations anchored at 5%, investors can get a real return of 6% from a risk-free investment – very high relative to longer-term averages of closer to 3%. Should yields normalise to a more sensible 9% level in one year (in line with where yields were two years ago), investors will receive a total return of nearly 25%, which is very much equity-like. Local equities do compete against this high hurdle for inclusion in our portfolios, but we are still finding many equity opportunities that comfortably do so.

Figure 1: Market implied SA government bond real yield

CPI expectations are anchored, and real yields are at an all-time high

Given our relative size, a sweet spot for PSG Asset Management has been the mid-cap sector, which has been largely ignored when looking at sell-side analyst coverage and representation in mainstream portfolios. Companies like the JSE, AECI and Sun International jump to mind.

As a parting thought, it is worth reiterating that, as John Gilchrist mentioned last week in his article, not all SA companies are created equal (or, are indeed, even truly SA Inc.). We believe investors wanting to exploit the opportunities need to be sure that they are getting truly differentiated exposure via a manager that is willing to look beyond the large index constituents to find opportunities for their clients to build wealth in the long run.