How to make the most of tax incentives beyond TFSAs

Jaco van Tonder, Head of Advisor Services in South Africa at Ninety One

The media hype about tax-free savings accounts (TFSAs) may take investors’ eyes off the other tax incentives available to them. There are other ways investors can benefit, particularly if they start the new tax year with a clean slate that makes the most of available tax incentives for long-term savings products.

01 Don’t lose sight of the most important savings goal: retirement

The first, and by far the most important tax incentive, remains an investor’s contribution to a registered retirement fund (either through their employer or via a retirement annuity).

Retirement funds have been a major talking point in the advisor community over the last few years. Most of the debate focuses on whether the tax benefits of retirement funds are enough to compensate investors for the investment restrictions imposed by Regulation 28 – specifically the 30% offshore exposure limit and the three-year delay in accessing retirement assets upon emigration.

At the time, Ninety One did some modelling work to quantify the value of retirement fund tax benefits over the lifetime of a pensioner. In addition to the well-known estate duty benefits of retirement funds, we concluded that the tax savings typically accumulate to an additional investment return of 2%-2.5% p.a. over the lifetime of a retirement fund member.

This is a material performance advantage and, unless an investor is planning to emigrate soon, we believe there remains significant long-term value in contributing to a retirement fund every year.

Advisor takeaway: For most investors, contributing to their long-term retirement plan remains the priority.

02 Maintain an emergency cash fund, maximising your annual interest exemption

Investors should use their annual tax-free interest income exemption (currently R23 800 for individuals under age 65 and R34 500 for people aged 65 and older).

At expected money market rates of between 4% and 5% p.a., an investor can safely keep approximately R400 000 in fixed income investments before paying any tax on the interest earned. This can be used to set up an investor’s emergency cash fund.

Just remember to include the emergency fund in the overall portfolio asset allocation to verify that the emergency fund is not making an investor’s overall investment portfolio too conservative.

Advisor takeaway: Make sure the investor has an appropriate emergency cash reserve in place as part of their overall investment portfolio and use available annual interest exemptions.

03 Don’t forget about your annual R40 000 capital gains tax (CGT) exclusion

Due to its relatively small size, many investors forget that the first R40 000 realised capital gain in a tax year for an individual investor is excluded from the calculation of the investor’s CGT liability.

Most advised investment portfolios are rebalanced on an annual basis to keep the portfolio aligned with the investor’s risk profile. Ensuring that these annual rebalances happen in the correct tax year can save clients unnecessary CGT. Even though the maximum tax saving is only around R7 200 per year currently (R40 000 x 40% x 45%), the saving will compound to a reasonable amount of money over time. So, keep an eye on the date (relative to tax year-end) that you rebalance a long-term investment portfolio.

Advisor takeaway: An investor’s annual capital gain exclusion, whilst small, can compound to a meaningful amount over time.

04 Set up a TFSA for the long term

When TFSAs were first introduced, many investors and advisors underestimated the extent to which TFSA tax benefits need time to compound. This is because a TFSA contribution is not tax deductible upfront like a retirement fund contribution, which makes it difficult to calculate the rand value of an investor’s TFSA tax benefit in advance.

In addition, the lifetime TFSA contribution limit further delays the real tax benefit to the period when the investor has used their full lifetime contribution allowance.

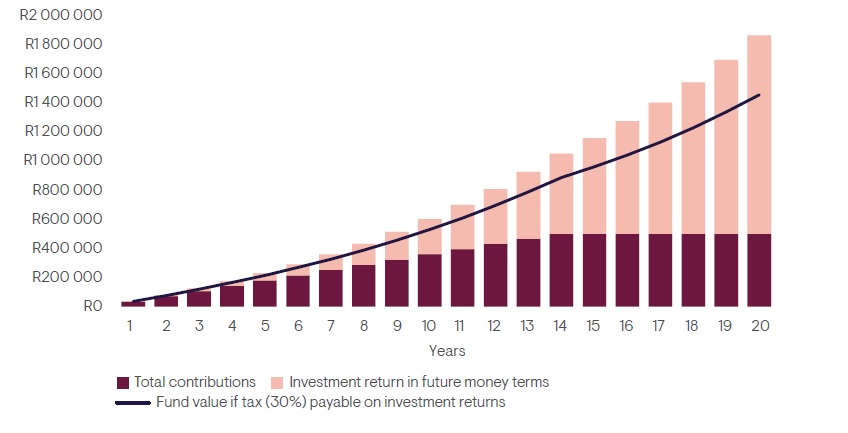

These points are best illustrated by an example. In Figure 1 we project a TFSA’s fund values over a twenty-year period, based on the following assumptions:

• An investor contributes the maximum annual amount of R36 000, and this limit is never increased by National Treasury.

• The R500 000 lifetime limit is never increased, and contributions cease when this limit is reached.

• Assume a 10% p.a. investment return and inflation of 6% p.a.

• Further assume a roughly 50/50 split in investment return between interest and capital gain, resulting in an effective combined tax rate of 30% on total investment returns.

Figure 1: TFSA value projection split between contributions and investment return

From the diagram there are three key points to note:

The investment return (the yellow bars) takes a long time to accumulate and only really becomes meaningful after about ten years. In the first five years the impact of the tax benefit is incredibly small. Yet after twenty years the tax saving represents more than 20% of the total fund value.

It is therefore clear that, from a tax benefit perspective, it does not make sense for an investor to utilise a TFSA for an investment horizon shorter than ten years. This picture changes dramatically after ten years due to the well-known compounding effect of long-term investment returns.

Advisor takeaway: TFSAs need to run for a minimum of ten years – otherwise the tax benefits are wasted.

05 Lifetime TFSA contribution limits are precious – don’t withdraw from a TFSA unless you absolutely must

Current TFSA product rules, as set out by National Treasury, do not allow an investor to recover any part of the lifetime TFSA contribution limit should they need to dip into their TFSA to fund an emergency expense. Every time an investor uses part of their TFSA contribution allowance, that allowance is gone forever.

Any redemptions from a TFSA therefore waste part of an investor’s lifetime contribution allowance –something to be avoided. For that reason, we believe that setting up a TFSA for an investor’s emergency short-term cash reserve is not a good idea.

Advisor takeaway: TFSA lifetime credits are very valuable – discourage investors from wasting their credits by dipping into their TFSA.

06 TFSA investment portfolios should be consistent with a long-term investment horizon

A final point for discussion is what represents the ideal investment portfolio for a TFSA. There really are two key considerations when deciding on an appropriate investment portfolio:

TFSA investments should be for ten years or longer for the tax benefit to compound meaningfully – investment portfolios should reflect this reality.

Since TFSAs do not attract income tax or capital gains tax, TFSA portfolios are neutral to whether returns come from capital gains, interest or dividends. Select investment options with the strongest long-term return potential.

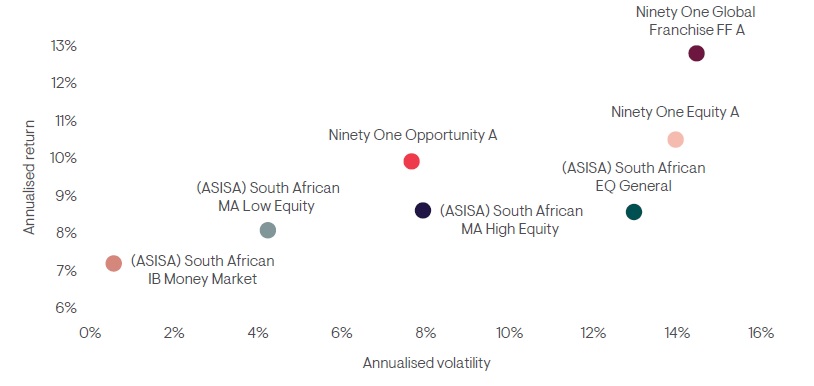

One way to illustrate these two points is to evaluate different investment strategies with reference to long-term returns and volatility measures. Figure 2 highlights the fifteen-year annualised returns and volatility statistics for a number of potential TFSA investment options.

Figure 2: Fifteen-year annualised return/volatility for various TFSA investment options?to 31 December 2021

Source: Morningstar Direct, as at 31.12.21. Performance figures are based on a lump sum investment, NAV to NAV, net of fees. Highest and lowest annualised returns since inception of the Ninety One Global Franchise Feeder, Opportunity, Equity and Money Market funds (12 month rolling performance figures) are: 45% and -40%; 43.8% and -15.7%; 65.8% and -34.8%; 18.8% and 3.8%, respectively. The total expense ratio of the Ninety One Global Franchise Feeder, Opportunity, Equity and Money Market funds (A class) are: 2.10%; 1.94%, 1.96% and 0.18%, respectively. Funds shown are for illustrative purposes only and are not necessarily the classes available on the Ninety One platform for TFSAs.

Figure 2 illustrates what most of us already know intuitively – when investing for the long term, conservative portfolio choices merely reduce the long-term investment return without really adding anything.

Fixed income investments in a TFSA can, however, appear attractive as they attempt to maximise the value of the tax saving (the logic being that interest is taxed at a higher effective rate than capital gains – therefore with a fixed income portfolio you maximise the value of the tax benefit). This logic is flawed as it is not only the value of the tax saving that matters, but the sum of the tax saving and the investment return achieved. As can be seen in Figure 2, fixed income investment returns disappoint over the long term compared to equity returns.

We would suggest a good starting point for most TFSA investors to be South African unit trust funds from the ASISA Domestic Multi-Asset: High Equity or similar category. These funds have historically produced very attractive long-term risk/return trade-offs, and work even better when tax does not affect the investment decision. One can comfortably move even higher up the risk curve, especially for longer investment horizons. For example, by far the most commonly selected investment option for the Ninety One IP TFSA has been the Ninety One Global Franchise Feeder Fund.

Advisor takeaway: TFSAs are long-term investments and should therefore have investment portfolios structured to maximise long-term investment returns. Cash and fixed income are poor long-term investments.

07 Conclusion

The introduction of TFSAs in 2015 has been a very successful initiative from government to encourage savings in South Africa. The initiative has really focused attention on the different tax incentivised savings vehicles available to SA investors. It is, however, important for advisors to review all the available options, and to not lose sight of investors’ other important savings goals – particularly saving for retirement.