How is inflation affecting the big investment themes of the future?

Schroders looks at what the resurgence of inflation means for thematic investing.

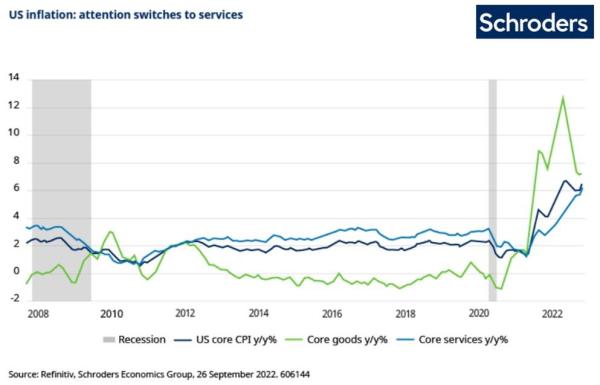

This time last year, many central bankers were talking about the “transient” inflation being experienced by the global economy as the imbalances caused by the Covid-19 pandemic unwound. But any thoughts that inflation may be temporary have long since been banished, especially as inflation broadens out to affect not just goods, but services too.

Schroders’ economists are forecasting global inflation of 7.2% this year, up from 3.4% in 2021. They forecast a moderation to 4.3% in 2023 but this is still above many central banks’ targets and well above the level experienced in most major economies in recent years.

Different geographies are experiencing inflation in different ways. After a protracted period of deflation, Japan’s current 3.0% inflation (y/y, as of August 2022) is welcome news for policymakers. That’s not the case in the eurozone where the 10.0% inflation rate (y/y, as of September 2022) is largely the result of soaring power prices and is now causing worries about imminent recession.

But what of different investment themes?

David Docherty, Investment Director – Thematics, said: “Thematic investing offers precise exposure to powerful, long-term global trends which are transforming the world. But each theme is different, so they won’t all be affected by inflation in the same way.

“What’s important to remember is that the most powerful themes have a very long duration. A theme like energy transition, for example, is an investment opportunity for the next 30-40 years, and the same goes for other themes that are shaping the world around us.”

Schroders’ experts explain how the return of inflation is impacting some of our favoured themes: global cities, digital infrastructure, energy transition, food & water, and smart manufacturing.

Global cities and digital infrastructure

Property is a sector where investors can often benefit from rising inflation. In part, this is because rising costs of building materials or labour hold back new construction, making existing properties more valuable. But many types of property have direct links to inflation.

Portfolio manager Tom Walker said: “Many leases across all types of sub-sectors have explicit commitments to rental increases tied to inflation. In some instances, there are also leases with fixed escalators or rent reviews at specific times.

“These all give investors the opportunity to ensure their income generates a real return; that is, one that is above inflation.”

However, not all real estate assets are the same. Investors need to pay close attention to the specific type of property they are investing in. Some types of real estate – housing, hospitals – are essential. Others are benefitting from strong demand and limited supply, such as data centres or student accommodation. But other segments are both inessential and experiencing weaker demand.

Tom Walker said: “The Covid-19 pandemic has accelerated a number of trends, such as e-commerce and working from home. These long-term structural issues have weakened the pricing power for owners of property assets such as retail and office space. Consequently, the ability to pass on inflationary increases to tenants in these buildings is severely limited.”

Location is also crucial when investing in property given that assets in more desirable locations can command higher prices.

“Focusing on locations where economic growth is consistently the strongest means that investors can maximise their chances of being able to pass on increased costs to their tenants,” Tom Walker said

Energy transition

The energy transition theme is one that has witnessed a significant impact from inflation in the past two years.

Portfolio manager Alex Monk said: “From an earnings perspective, companies have seen their profitability decline as their costs have increased. And from a valuation perspective, the higher interest rates required to tame inflation have decreased the value of future cashflow growth.

“It's with respect to this threat that companies in some of those higher growth areas - such as renewable energy, energy storage, and hydrogen - have felt the most pain. This is because the value of their earnings is far further out in time, and they've also been more exposed supply chain shocks.”

Companies making large items such as wind turbines have been among those most severely affected. This is not only because of the rising price of raw materials like steel and other metals, but also the higher cost of shipping. Factors ranging from disruption in Chinese ports as a result of Covid-19, to the temporary blockage of the Suez Canal in March 2021, all put upward pressure on freight costs.

There are signs that some of these factors are easing, and prices for metals have been falling. But the energy transition theme remains in the inflation spotlight because of the sharply elevated power prices in Europe as a result of the reduced supply of Russian gas.

Alex Monk said: “With energy prices being one of the main causes of inflation, which in turn may cause a recession, it is absolutely vital that more energy supply is brought on.

“Given the speed at which we can increase renewables capacity compared to some of the conventional forms of energy, the need for more supply plays into the structural opportunity behind the energy transition space. We are going to need lots more renewables, lots more energy storage, and even hydrogen to solve the energy crisis that we have today, particularly in Europe.”

Food and water

Higher food prices have been a substantial component of higher overall inflation this year. As with energy, this is due in large part to Russia’s invasion of Ukraine, which has pushed up prices for some agricultural commodities.

Wheat prices in particular have soared given that Russia and Ukraine together accounted for c.25% of global wheat exports prior to the invasion.

This situation may well persist, according to portfolio manager Felix Odey. “Tightness in supply and demand may even worsen in 2023 and beyond,” he said. “That’s because unpredictable weather patterns are adding to supply uncertainty, alongside the possibility of continued disruption to production in Ukraine.”

Higher agricultural commodity prices may be beneficial for farmers and investors in those commodities, but they feed into food price inflation all along the chain to food producers, retailers and ending up with consumers.

“There is a lag between agricultural commodity prices going up and those rises being passed down the chain,” Felix Odey said. “What we’ve seen so far is that food producers have been quicker to put up their prices than the retailers.

“Partly this is because of an awareness of other price pressures facing consumers, and the possibility of negative publicity for a supermarket raising prices.”

Rising food prices can mean consumers trading down, meaning they buy cheaper products such as supermarket’s own ranges, rather than branded products. However, the fact food is essential means demand will never drop very far. Food retailers may even benefit as consumer spending patterns change.

“Higher prices in restaurants may mean people are less likely to eat out, preparing more meals at home instead”, Felix Odey said. “It’s not only the supermarkets who could benefit from that trend, but also firms like the meal kit providers, who offer a break from home cooking without the expense of dining out.”

Smart manufacturing

The smart manufacturing theme is about innovation driving a digital industrial revolution to manufacture better goods, and to manufacture better.

Technologies that help improve energy efficiency are an integral part of this.

Portfolio manager Dan McFetrich said: “In Europe, industrial energy consumption amounts to 26% of total European usage. Clearly, at a time when gas supplies are precarious and energy inflation is high, we would expect demand to increase for technologies that enable electrification and energy savings.”

But there are manufacturing trends that are also sources of inflation, rather than solutions to it. Re-shoring – or the trend for companies to move production closer to demand – is an example of this. It has partly been driven by the pandemic when goods needed in Europe or the US were held up by prolonged lockdowns in China.

“Re-shoring is inherently inflationary,” Dan McFetrich said. “It’s about companies pursuing the ‘best cost’ rather than the lowest cost option. For example, this may imply higher labour costs or costlier components as businesses move production to more expensive regions. But the upside is more resilient supply chains, reduced logistics costs, and lower carbon emissions from transportation.”

And a further aspect of smart manufacturing – automation - has the potential to ease the cost of re-shoring. The cost of robots is falling due to economies of scale and rising adoption of automation across a range of industries. But many industries are facing labour shortages - which will only worsen due to ageing populations in developed countries – and are having to lift wages to attract workers.

Dan McFetrich said: “For all industries, automation can result in higher productivity, reduced labour costs and greater energy efficiency – all of which is an extremely attractive proposition at a time of rising inflation.”

Inflation impact is not uniform

What’s clear is that the inflation impact on different themes is very diverse. Even within a single theme, the investment opportunities are not all affected in the same way.

David Docherty said: “While the strongest themes are about global transformation, that doesn’t mean all the investment opportunities within each individual theme are simply plays on long-dated growth. Within food & water, for example, supermarkets and other food retailers represent more defensive opportunities that may be attractive in times of higher inflation and/or lower growth.

“Then there are the inflation ‘shocks’ such as the energy price spike caused by Russia’s invasion of Ukraine, that highlight the necessity of the energy transition. For investors who can look through the short-term volatility caused by inflation, such themes remain extremely attractive.”