How do interest rates affect my investments?

Gerbrandt Kruger, Associate Portfolio Manager of Morningstar Investment Management SA

In 2020, the South African Reserve Bank (SARB) dramatically cut the country’s interest rate by 3%, lowering the repo rate to a historic low of 3.5%. The SARB initially started to cut interest rates in response to declining inflation, which was sitting towards the bottom-end of the inflation target band (of between 3% and 6%). In mid-2020, the SARB cut the repo rate even further, in response to the COVID-19 crisis, to provide relief to consumers and businesses and promote economic growth. By cutting the interest rate, the SARB intends to provide a helping hand to the economy, by freeing up more capital for lending (by financial institutions) to households and businesses.

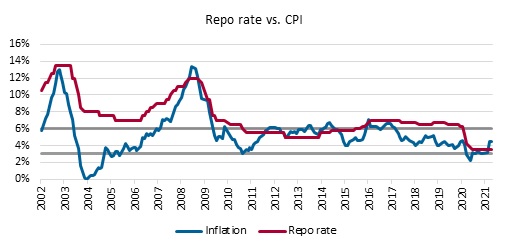

In South Africa, the standard measure of inflation is Statistics South Africa’s (Stats S.A.’s) consumer price index (CPI). This index represents a typical basket of goods and services used by South African households, comprising everything from lottery tickets to petrol and life insurance. Stats S.A. monitors these prices throughout the year and reports any changes each month.

As can be seen in the below graph,the repo rate tends to track inflation. While inflation has been sitting at the bottom of the inflation target band, we have seen a small up-tick over the last month.

Source: South African Reserve Bank and Stats S.A. Data as of 31 May 2021.

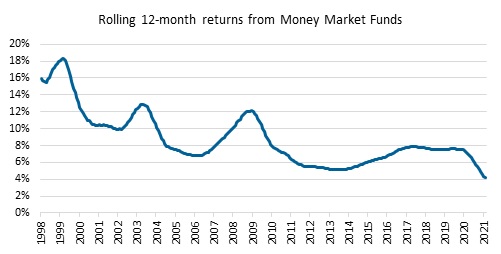

In the words of Isaac Newton – “Every action has an equal and opposite reaction”. In the case of interest rate cuts, repaying debt becomes cheaper, however, the interest earned on savings is also discounted. While we have all welcomed the perks of the lower repo rate (for example a lower monthly home loan or car repayment), a lower interest rate is the kryptonite to fixed income investments. As can be seen in the below graph, investors in money market and income funds have seen the yield on their investments decrease in line with the lower interest rates and short duration bond yields.

Source: Morningstar Direct. Data as of 31 May 2021.

Over the past year, money market fund returns dropped to between 4% and 5%, depending on fund fees. This is far from the 8% investors became accustomed to historically. We are currently also experiencing negative real cash yields. So, not only have investors’ returns halved, but inflation has also started to overtake their returns from cash.

Provided there are no major crises or shocks to the economy, we are at the end of the rate-cutting cycle. The next move will be a rate hike, however, there is still a lot of uncertainty on when this will take place. At the last Monetary Policy Committee (MPC) meeting in May, the decision to keep interest rates unchanged was unanimous. The MPC members still believe that inflation will be contained for the remainder of the year, reaching the mid-point of 4.5% in 2022. Inflation expectations have remained stable. While a stronger rand has been putting downward pressure on inflation, higher water and electricity tariffs will be included in the July/August figures, which will push inflation upwards.

A low interest rate is not bad for all investments. There tends to be a 12-month lag between interest rate cuts and seeing the widespread impact on the economy. A lower interest rate increases the supply of money, making it cheaper to borrow and provides increased disposable income. This leads to increased spending and consumption. In periods of low interest rates, we typically see the earnings of companies increase, while their borrowing costs decrease. The market then starts to re-evaluate the companies and we typically see a rally in the equity market. For the 12 months ending 31 May 2021, the South African equity market has returned 38%, compared to 4% from cash.

What will happen to my investments when interest rates start to increase?

The MPC will likely look to hike interest rates when inflation expectations start to breach the upper end of the inflation target band. How aggressively they hike interest rates will be dependent on what the inflation drivers are and how the economy is doing. The yield on money market funds will increase in line with the hikes. We will see some negative returns in the bond market as yields increase to accommodate the expected hikes and inflation increases. Long duration bonds will be affected more than short duration assets due to their higher interest rate sensitivity. There is no guarantee that a rate hike will negatively impact equity markets, however historically the cheaper/value areas of the market tend to outperform the growth areas of the market in a rising interest rate environment. Typically, rising interest rates occur during periods of economic strength. In this scenario, increased rates often coincide with a bull market.

Investors should remain focused on their long-term investment goals, even amid changing interest rates. In a world of many unknowns and uncertainties, we continue to do what we do best: follow our in-depth disciplined research and portfolio construction process to find the best possible opportunities and outcomes for our clients. This means building a diversified portfolio made up of quality stocks, bonds, cash and cash equivalents that will pay dividends and interest through the ups and downs of the market and the global economy at large.

Time in the market remains superior to timing the market. Markets keep moving up and down, and so too do investors’ emotions. This is understandable – it is, after all, their hard-earned money we’re talking about. At this stage, the best thing investors can do is to remain patient. While noise and speculation can act as an emotional rollercoaster, your goals are unlikely to have materially changed and, therefore, your plan shouldn’t either.

The smartest thing investors can do is manage their portfolios to limit the downside and increase potential upside as interest rates and the market fluctuate. Diversification is the best way to do that — regardless of where interest rates are heading in the short- or long-term.