How China’s continued recovery could buoy EM assets

Despite underwhelming economic data for July, we think China’s economic recovery remains on track, which bodes well for emerging market assets.

An underwhelming set of activity data showed that China’s economy was still not firing on all cylinders in July. But with fiscal and monetary stimulus still working their way through the system, leading indicators such as retail sales suggest that the recovery remains on track.

The re-emergence of debt-fuelled growth will do nothing to soothe long-standing concerns about the structure of the economy and misallocation of capital. However, in the near term it should ensure that China will be one of the few economies in the world to grow this year. We forecast an expansion of just over 2%, with a further acceleration towards 7% in the pipeline for 2021.

The relatively good performance of China’s economy is likely to lend further support to the performance of mainland financial markets. An increasingly heated US presidential election campaign has the potential to rock risk appetite at any moment. However, there ought to be positive spill over effects from the economic recovery in China to the performance of equities and bonds elsewhere in the emerging world.

China’s rebound lost some steam in July

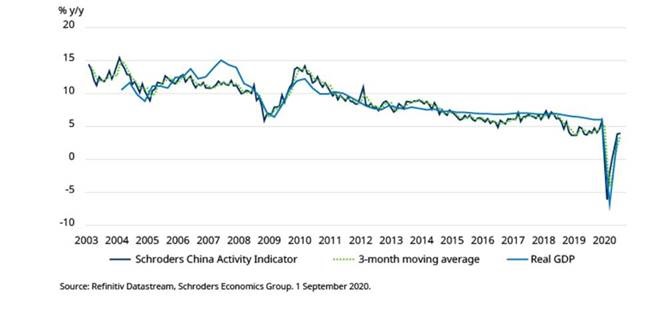

The latest batch of activity data suggest that, after staging an impressive rebound in the second quarter, the recovery in China’s economy lost some steam in July. Since the official national accounts have historically shown very little cyclicality, we use monthly data on trade, retail sales, industrial production and investment to estimate our own China Activity Indicator to track growth. Our gauge suggests that GDP growth increased only marginally in July, to 3.9% y/y from 3.8% y/y in June, as chart 1 shows.

Chart 1: GDP growth appears to have edgede higher in July

Consumers are still reluctant to hit the High Street

It is only natural that the rebound in activity will lose some steam. After all, China’s economy has already recovered much of the output that was lost during the most intense phase of the Covid-19 crisis, when GDP contracted by a seasonally-adjusted 10% quarter-on-quarter (q/q) in the first quarter. Once the government relaxed the most severe restrictions on activity that were imposed to contain the spread of the virus, GDP rebounded strongly by 11.5% q/q in the second quarter.

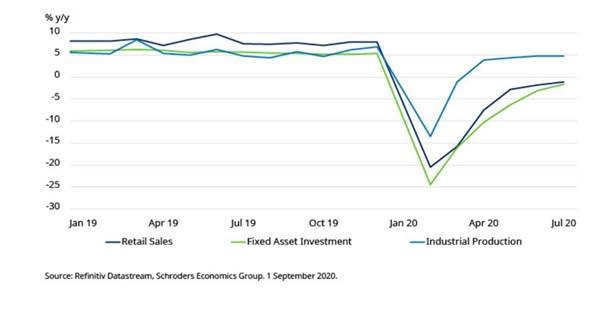

This release of pent-up activity is likely to have largely run its course. However, the recovery has been uneven with some parts of the economy clearly lagging behind. In particular, retail sales continued to contract in July, down by 1.1% from a year ago in nominal terms, as shown in chart 2.

Chart 2: Retail sales and investment are lagging behind industrial production

There are a couple of explanations for this. One is that the Covid-19 pandemic appears to have caused a change in the behaviour of consumers. For example, high frequency data show that passenger numbers on public transport in major cities in August were still 10-20% below the levels seen during the same period last year. This could be explained by a greater proportion of people working from home, or simply just concerns about contracting the virus.

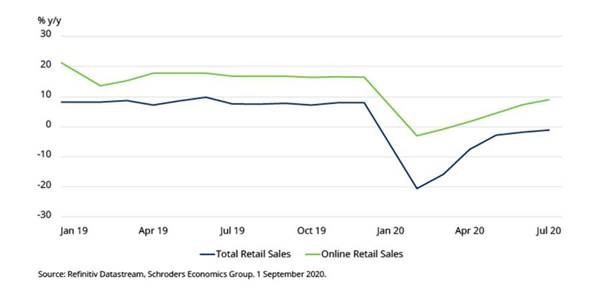

Whatever the explanation, this new pattern of consumer behaviour is a problem for service sector companies that rely on footfall; and it may persist, at least until a large proportion of the population has been vaccinated. This suggests that the relatively quick recovery in online retail sales will continue (Chart 3).

Chart 3: The relatively strong recovery in online retails sales is likely to continue

In addition, there is probably a second, more traditional economic explanation for the sluggish recovery in retail sales. The major shock that ripped through China’s economy earlier this year is likely to have caused a deterioration in the labour market, with subsequent negative effects on disposable income and consumer confidence.

It is not easy to gauge conditions in China’s labour market, but it is notable that the employment sub-components of the various Purchasing Managers’ indices have been slow to recover after plunging earlier this year. This implies that many lost jobs are yet to be replaced. Similarly, the employment and income of migrant workers was slow to recover in the first half of the year. The authorities will hoping that these labour market dynamics improve as the broader economy continues to recover.

Construction activity has rebounded

In this respect, it is good news that other parts of the economy are performing well. While fixed asset investment also continued to contract in July, by 1.6% year-on-year (y/y), it has been held back at the headline level by weak investment in the manufacturing sector. Investment in infrastructure and real estate has rebounded relatively strongly (Chart 4), corroborated by a surge in import volumes of industrial metals such as copper and iron ore, and sales of heavy trucks.

Chart 4: Policy support has underpinned a rebound in construction activity

Infrastructure spending has been buoyed by fiscal stimulus as local governments have issued various bonds and used the proceeds to fund projects. The government recently announced that it will strive to speed-up the implementation of projects, which ought to further lift infrastructure investment in the coming months.

Accelerating credit impulse should support activity and asset prices

At the same time, it seems that looser monetary conditions have begun to feed through to the real estate sector as housing sales and starts have rebounded. The authorities have been vocal in warning against property speculation after huge price increases in recent years, but the pick-up in real estate activity probably has further to run.

Monetary policy works with a lag and the current low level of interest rates is consistent with China’s credit impulse – that is the 12-month change in credit as a share of GDP – building more momentum in the months ahead (Chart 5). This would explain why the People’s Bank of China has been happy to adopt a “wait and see” stance in recent months with regards to setting policy interest rates, instead focusing on supplying liquidity to the financial system.

Chart 5: China’s credit impulse is building momentum

Turning back the clock to credit-fuelled construction growth will do nothing to solve China’s long-term challenges of high debt levels and the associated risk of misallocation of capital. However, those concerns are for another day and a rising credit impulse should aide the government’s near-term goal of reviving economic growth.

If we are right, then the recovery in China should continue to offer a fertile environment for emerging market (EM) assets in the near term. A rising credit impulse in China has historically been a good sign for the performance of industrial metals, along with EM equities and fixed income. Chart 6 highlights the correlation between China’s credit impulse and changes in the stripped spread of the JP Morgan EMBI benchmark for US dollar denominated sovereign bonds. A decrease in the stripped spread is indicative of a decrease in investor risk aversion. Our assumption that the credit impulse will build more momentum suggests that spreads will continue to tighten in the months ahead.

Chart 6: Emerging Market spreads usually as China’s credit impulse rises

Upturn in the industrial cycle is a positive sign for EM equities

Finally, China’s official statistics show that the industrial sector has so far been the key driver of the economic recovery, in part supported by surprisingly resilient exports. The official data for industrial production are suspiciously stable and until the recent crisis had shown very little cyclical dynamic as growth fluctuated in a narrow range of around 5-6% y/y for the past five years or so.

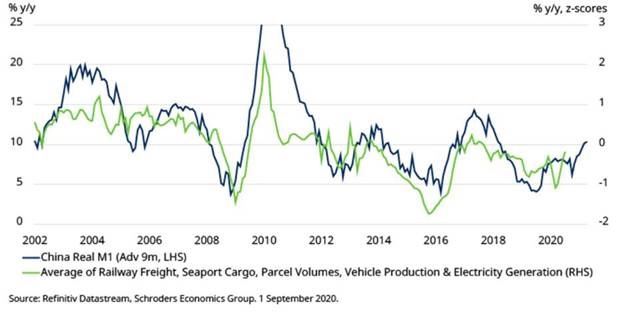

Other, lower-level indicators such as the volume of railway freight, seaport cargo and parcel deliveries tend to be far more cyclical. But even these measures of activity point to a strong recovery in recent months and leading indicators suggest there may be more to come.

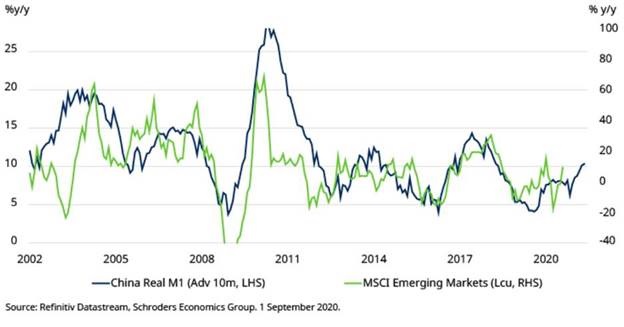

For example, these cyclical indicators have historically been fairly well correlated with growth in real M1 with a lag of about nine months. Here we deflate growth in M1 with headline inflation until March 2019, from where we use core inflation in order to strip-out noise caused by a spike in food inflation that followed the outbreak of African Swine Fever in pigs 2018. The lagged relationship suggests that there is scope for industrial and trade-related activity in China to further recover in the months ahead (Chart 7). And there is a good chance that growth in real M1 will accelerate in the months ahead as looser monetary policy passes through the economy and confidence improves.

Chart 7: The cyclical upturn in Chinese industry has further to run

China’s importance to global supply chains means that its industrial cycle has become inextricably linked to the fortunes of other, export-dependent EM in the region such as South Korea and Taiwan. As such, it is perhaps not surprising that leading indicators of China’s industrial cycle have also become a good barometer of the outlook for the performance of financial markets in the region – particularly Asian-dominated equity benchmarks such as the MSCI Emerging Markets Index.

There are many other factors at play that could dent the performance of EM corporates as a result of the Covid-19 pandemic, but taken at face value the historical relationship with growth in Chinese real M1 suggests that EM equities could get a further lift in the months ahead as analysts revise-up their expectations for earnings (Charts 8 & 9).

Chart 8: Analyst’s expectations for EM corporate earnings appear too pessimistic

Chart 9: Emerging Markets equities look set to rise further

China’s recovery is on track

The upshot is that in spite of a slightly underwhelming set of activity data for July, there are enough reasons to think China’s economy will continue to recover in the months ahead as large fiscal and monetary stimulus work through the system. As a result, we continue to expect GDP to expand by about 2% this year and 7% in 2021. That would be a relatively good performance when compared to the rest of the world, while the authorities still have room to further loosen policy if the recovery stumbles.

There are of course risks on the horizon. In particular, geopolitical tensions, which are likely to intensify yet further as the US presidential election draws nearer, and which could unsettle investors. However, a continued economic recovery in China should provide more near-term support to the performance of both mainland Chinese markets, and those in other parts of the emerging world.