Highly Strung Markets

Early morning on 7 August 1974 – fifty years ago – New Yorkers noticed a strange sight on their famous skyline. A young French artist named Philipe Petit had snuck up onto the roof of the South Tower of the World Trade Center.

Using a bow and arrow, he shot fishing line across to the North Tower, which his accomplices used to guide a tightrope between the two skyscrapers, then still the tallest buildings on earth. Petit carefully walked across six times with nothing but a balancing beam to assist him, the giant city awakening 400m below, and only summer sky above. It was an act that was at once crazy and captivating.

Walking a metaphorical tightrope remains a daily duty for most investors, though admittedly the stakes aren’t as high, nor is the backdrop as spectacular. It is a balancing act between the need for inflation-beating returns over time, and the risk that comes from equity investing. True, there are times when cash returns are high – in fact, South African cash currently yields 3% in real terms – but this rarely lasts as interest rates are cyclical. Therefore, wealth creation comes ultimately from investing in companies that grow their earnings in excess of inflation over time. Unfortunately, their share prices can be very volatile in the short term. This trade-off between short-term volatility and long-term growth never really goes away. And while it sounds simple in theory, in practice the emotional response to falling prices often overwhelms the rational.

Don’t look down!

The events of the past two weeks are a case in point. Having ended the month of July on a high, global equity markets corrected sharply in the first few days of August. Several crowded trades, some of them leveraged, reversed sharply. Picture a small rowing boat where several occupants are sitting on the same side. It is unstable and at risk of tipping over as soon as it hits a wobble. Heading into August, popular trades included “short volatility” strategies, like the Artificial Intelligence (AI) theme (aka the Magnificent Seven), and the Japanese yen “carry trade,” a version of which involves borrowing cheaply in yen and investing elsewhere for a higher return. There is some speculation as to which of these is the real culprit, but what is ultimately important is that each amplified the shock on the others as they were being unwound.

Moreover, all of this happened during the Northern Hemisphere summer holiday, when liquidity is typically thinner.

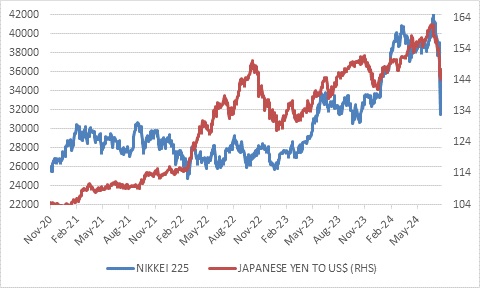

The biggest victim so far has been the Japanese equity market, where the Nikkei Index slumped 12% on Monday, the worst decline since Black Monday in 1987. The next day, it jumped 10%. Clearly, economic fundamentals did not change in the space of two days. But risk appetite swung massively.

Chart 1: Japanese equities and the yen

Source; LSEG Datastream

In fact, the October 1987 Black Monday crash is a useful example. In a well-known study, Robert Shiller, who later won a Nobel Prize for his work, sent a questionnaire to nearly 1 000 individual and institutional investors as the market was crashing. He found that respondents largely did not sell stocks in reaction to news or rumours, but basically sold because prices were falling amid a sense that the market was overvalued. Most investors interpreted the crash as a psychological reaction from other investors, and few pointed to a change in economic fundamentals as the reason for the sell-off as it was happening. Of course, after the fact, there were many rationalisations from amateurs and professionals alike, as well as hearings in Congress. But in the end, Professor Shiller’s work showed simply that selling begat selling.

Slowdown versus slump

Returning to the idea of the crowded and imbalanced rowing boat, in the end it doesn’t really matter what causes it to capsize, since it is a near-inevitability. To switch metaphors from water to fire, when there is much dry kindling about, a spark from any source can ignite a blaze.

In this instance, however, the nature of the spark does matter, since it concerns growth prospects for the US economy. If the US was to enter a recession, it would have a much greater market impact than the volatility of the past two weeks.

Here’s what we know. The US economy is slowing, which is perfectly normal after a period of strong growth. To put it slightly differently, when unemployment is already near record lows, it can really only rise. However, nothing screams recession or a substantial rise in unemployment yet.

It was weak manufacturing data from the Institute of Supply Chain Management (ISM) that ignited the August growth scare, but the latest services ISM Index, covering a much greater portion of US economy activity, was in positive territory above 50 points though clearly not as strong as a year or so ago. Similarly, though the US government’s monthly labour market report for June was weaker than expected, one should never draw big conclusions from a single data point. These are often revised later, and any single monthly number can be subject to noise. A broader range of labour market indicators tells a story of a slower pace of job creation and less job switching, but no surge in layoffs. Slower wage growth does imply slower consumption growth, but it also reduces upward inflation pressure – a positive from the Federal Reserve’s point of view.

Click here to read more...