Has value's ship sailed?

Value’s recent strong performance has led many investors to question whether they’ve missed the boat. Here’s why we think they haven’t.

The last six months have seen the value style of investing stage a very welcome comeback which has had value managers breathe a sigh of relief.

Since Pfizer’s successful vaccine announcement at the beginning of November, we’ve seen previously unloved sectors of the market rally quite strongly. These included the likes of banks, energy, automotive and advertising dependent businesses.

Value’s recent outperformance is a tremor, not an earthquake

But it’s important not to focus too much on short-term percentage price moves because when you zoom out and look at the bigger picture, you can see that many shares are still trading on deeply depressed valuations.

The below chart shows that valuation dispersion within the market – the gap in fundamental valuation between the most highly rated and the least highly rated shares globally – remains at extreme levels.

The opportunity is still substantial

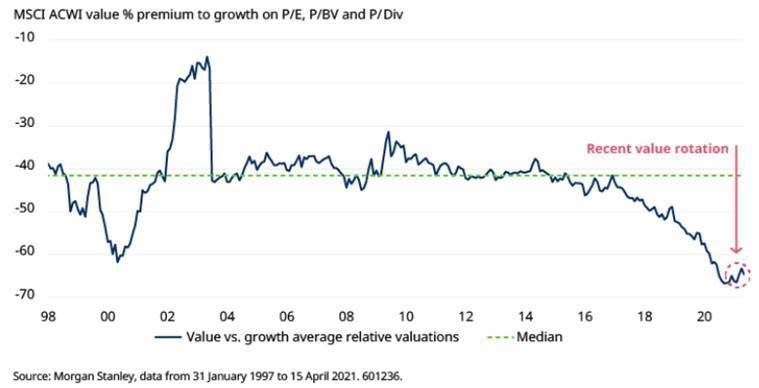

Valuations of value vs. growth are still near all-time lows

The latest bounce in value performance is barely visible at the end of this chart.

The moves we’ve seen in recent months may feel dramatic but we think we’re looking at a tremor of performance rather than a real earthquake. If valuation gaps in the market are to return to something more like normal in the context of long-term history, there seems to be a long way to go.

But we’d also sound a note of caution.

In the last couple of years, we’ve begun to see the sort of crazy market behaviour that typically occurs at the top of market cycles. In fact, this is exactly the sort of behaviour that characterised the peak of the dotcom mania in 1999/2000.

We think the parallels between that period of market history – when bullishness got seriously out of control – and today are increasingly plain to see.

Rebutting the “this time it’s different” argument

But there are those who disagree. They argue that this time the companies attracting really high valuations are genuinely exceptional businesses with solid fundamentals that are changing the world.

In other words, their eye-watering valuations are justified and this is simply a new reality.

Our response is based on two observations:

1) Investors thought the same thing in 2000 too! The top four largest tech companies at the height of the boom were Microsoft, Intel, IBM and Cisco. These were genuinely high quality businesses that delivered exceptional growth in profits and high attractive returns.

They were great businesses but they also proved to be terrible investments if you bought them at the wrong price. Over the following three years from the peak of the dotcom boom, they fell by an average of 60%. Just because these tech giants are big, innovative and growing fast today doesn’t mean people can’t lose money investing in them.

2) Even if you exclude the exceptional impact of the big tech winners at the top of market indices, valuation dispersion is still a long way above historically normal levels.

The below two charts show that if you exclude either the top 5% of megacaps or the most expensive 10% of the universe, you get a similar picture: the difference between the most and least loved parts of the market remains big, by any historical standard.

The higher ‘the quality this time’ argument sounds persuasive

But valuation dispersion is much broader than that

This suggests to us that the trend of the last few years isn’t something that can be explained away as rational market behaviour in the face of the emergence of a handful of exceptionally valuable business.

This looks to us like the market has, once again, abandoned the idea that fundamental valuation is important.

What happened when the music stopped last time?

So, what if we’re right and we’re looking at an eerily similar market backdrop to the one in 1999/2000?

What happened when the music stopped and the hangover from the speculative growth party kicked in?

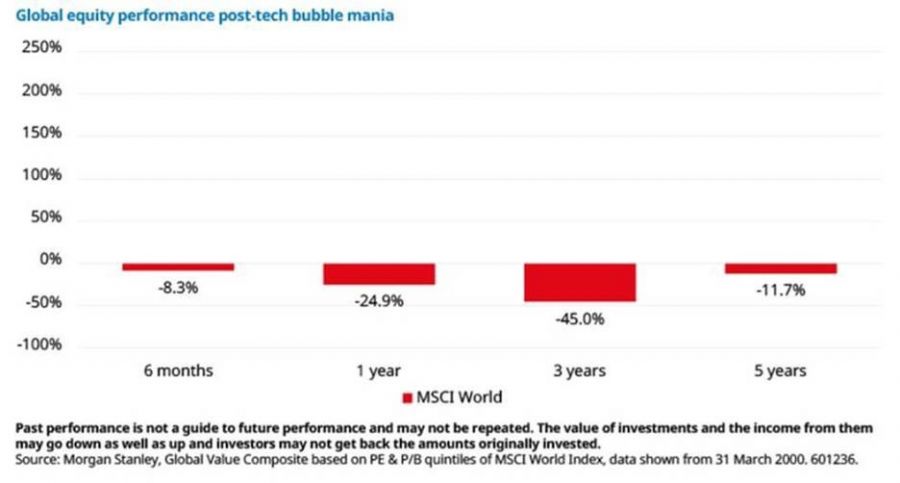

From the peak of the market cycle in March 2000, global equity indices entered a painful, drawn out bear market. Even five years on from the peak, the MSCI World Index was still under water in absolute terms as you can see on the red bars below.

What happens when the music stops?

5years on from dotcom peak, Global indices were still in red

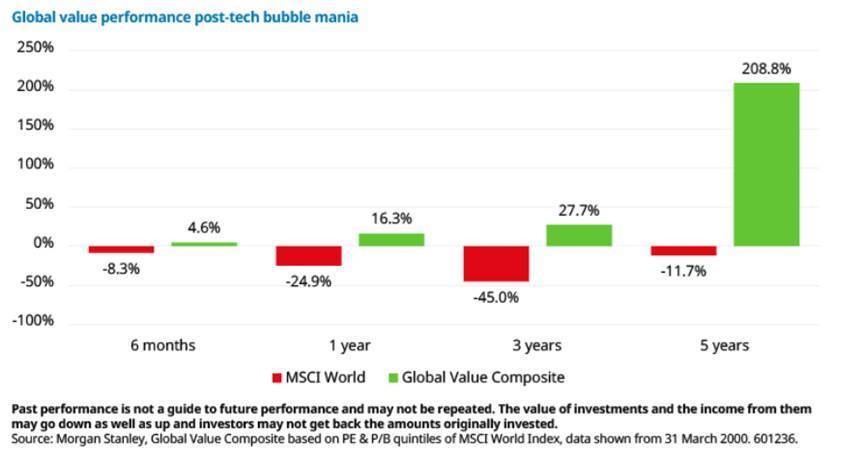

During that same time period, global value delivered a very strong period of both absolute and relative performance as you can see in the green bars below.

What happens when the music stops?

But value behaved very differently from the broader market

Systematically avoiding the most egregiously overvalued stocks in the years leading up to the peak had left value investors chastised and mocked by many in the investment community.

But in the fullness of time, sticking solely to the cheapest areas of the market stood them in good stead.

It is worth emphasising that value as a style often underperforms into the tail end of a bull market. Fashionable areas of the market soar and value investors are often left behind.

But when financial gravity starts to bite, value often does pretty well. And it is during the periods of irrational exuberance that markets will present some wonderful contrarian opportunities for investors that are willing to swim against the tide.

Finding value in unexpected places

Some of those contrarian opportunities can be found in obvious parts of the market such as in the banking and energy sectors.

We think banks are very attractive, not least because they have record high levels of capital, have spent a decade reducing risk and are part of the solution to the crisis (as opposed to the cause of it as was the case in the global financial crisis).

Energy companies are another posterchild value area. At last they’re showing capital discipline, focusing on costs and returning capital to shareholders. This, in combination with exposure to potentially rising oil prices, makes for a compelling opportunity.

We have also found that a handful of attractive opportunities in Japan. In the past we’ve avoided Japanese stocks on the basis that many of them were value traps. But the stocks we currently like have compelling valuations, present relatively low risk and have historically showed little correlation to other stocks we hold.

Then there are those parts of the market that were hit during the pandemic panic. Some high quality businesses were unfairly sold off during the eye of the storm and this allowed us to pick up some exceptional purchases which we expect to rebound as the world recovers from the pandemic.

These vary from the “tortoise stocks” (i.e. likely to be slow and steady winners like food retail and telecoms) to “turnaround stocks” (i.e. businesses that have endured a rough patch but are in the process of being turned around and recovering).

Not too late to embark

It’s clear that there are plenty of places to find genuine value in today’s market for the active investor and that it’s not too late to get involved.

We believe value has plenty of upside given current levels of valuation dispersion and that it can offer powerful protection in otherwise “bubbly” markets.

We continue to think value should have a long-term place in every client portfolio.