Halftime refresh

With the first half of the year behind us, what are the main items on the radar for the last six months of 2019? Before discussing these, it’s worth pointing out that markets are moved by surprises, and known risks tend not to cause big problems. It is the unknowns that hurt portfolios. In other words, investors should worry about what others are not worried about. However, when everybody is worrying about something, it often depresses the relevant asset price more than necessary, giving rise to buying opportunities.

Trade and manufacturing: unhappy twins

The euphoria around the trade truce between the US and China agreed to at the G20 Summit lasted exactly one day. The US government is now threatening tariffs on $4 billion European imports, accusing European governments of unfair support for Airbus, the big competitor of Boeing. This was followed by a tweet from US President Trump accusing Europe and China of manipulating their currencies lower to gain a competitive advantage against the US. He implied that the US should similarly intervene to weaken the dollar, something it has done only in extraordinary circumstances. The bottom line is that trade will be a source of uncertainty for the duration of the Trump administration, and possibly beyond. Linked to trade uncertainty is the weakness of global manufacturing. The JPMorgan Global Manufacturing Purchasing Managers’ Index (PMI) fell to a six-and-a-half year low of 49.4 in June. The PMI for manufacturers of consumer goods was in positive territory, as global retail sales remain firm. But the PMI for intermediate goods – inputs for other factories – was negative, reflecting global trade conditions, as was the PMI for capital goods, with business investment remaining soft. South Africa’s manufacturing sector is similarly under pressure, with the latest Absa PMI still stuck below 50.

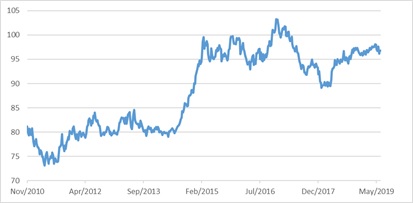

Manufacturing is a highly cyclical sector, and hence the focus of economists. The weakness cannot be entirely explained by trade wars; the world simply seems to have enough cars and smartphones to last a while. The nature of manufacturing is also changing. During the golden age of globalisation prior to 2008, companies extended their supply chains, outsourcing the production of components to far-flung but cheap corners of the world. The more recent trend has been to shorten some of these supply chains and bring production closer to the end customer, aiming for faster turnaround times rather than lower cost. The trade wars are likely to accelerate this process. Another factor is the persistent strength of the dollar since 2011. Research from the Bank of International Settlements shows that financing these value chains is expensive when the dollar is strong, even when interest rates are low. This is because 80% of trade financing is denominated in US dollars, and lending in dollars is subdued when the dollar is strong.

Chart 1: US trade weighted dollar index

Source: Refinitiv

Consumer spending is still robust in the major economies, supported by jobs growth, modest wage increases and low inflation. This means that either the production of goods should rise to meet consumer demand (manufacturing output is dragged up) or the weakness in manufacturing leads to job losses and downward pressure on wages, dragging consumer spending down (with a vicious cycle ensuing). This is more likely in a country like Germany where manufacturing is a bigger part of the economy than in the US, where it is a small sector.

On the way down: central bank policy

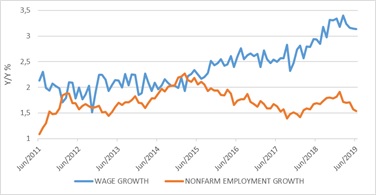

Interest rate and inflation expectations remain extremely low, judging from the bond market. The global benchmark US 10-year Treasury (government bond) yield briefly fell under 2% last week, well below the Federal Reserve’s policy interest rate. The bond market is therefore pricing in a series of Fed rate cuts. Friday’s US employment numbers showed that this expectation might be somewhat exaggerated, with 224 000 new jobs created in June, more than expected. However, the year-on-year growth in job creation had slowed to 1.5%, while wage growth remains muted at 3.1%. The Fed has reason to reduce rates, but no obvious need to slash them.

Chart 2: Monthly non-farm job creation and wage growth in the US

Source: Refinitiv

Elsewhere, the nomination of former French finance minister and current International Monetary Fund (IMF) head, Christine Lagarde, as Mario Draghi’s successor in the role of European Central Bank (ECB) President is an interesting but welcome development. Although she has no direct experience in monetary policy, she has proven herself to be a pragmatic leader at the IMF. In many respects the ECB’s challenge is political and not technical. It will need the buy-in of Germany and other conservative countries to launch any further rounds of unconventional stimulus. Inflation is running at around 1% against a 2% target and the risk is that consumer and business expectation of future inflation will became anchored at these low levels, influencing price-setting behaviour accordingly. The Reserve Bank of Australia cut rates for the second time in many months last week, taking its policy interest rate to a record low 1%. Our own Reserve Bank’s Monetary Policy Committee meets later this month, and a rate cut is on the cards. With a global cutting cycle now firmly underway, inflation under control and the rand a bit firmer, it has a window of opportunity to give the consumer a small, but much-needed boost. With central bank support, the global economy, though bending, is unlikely to break.

You can check out, but you can’t leave

One approaches the topic of Brexit with trepidation, given the shambolic state of British politics. But the deadline for leaving the European Union is 31 October (which somewhat ominously coincides with Halloween), and key decisions will have to be made soon. The UK’s likely new Prime Minister, Boris Johnson, has indicated he is prepared to take the country out of the EU (its largest trading partner by far) without an exit agreement if acceptable terms cannot be agreed on. Most economists believe this will be a shock to the economies on both sides of the English Channel, but will impact the UK more. However, in the UK political system Parliament has the final say, and it’s not clear that a majority of MPs will allow a no-deal Brexit. It might instead lead to a new election and yet another new Prime Minister. Exactly how this movie will end is anyone’s guess at this stage. As bad as a no-deal Brexit could be, the biggest risk in Europe remains Italy, where a toxic combination of a depressed and uncompetitive economy, a highly indebted inefficient state and populist politics could still result in the country leaving the Eurozone in coming years. While the UK kept its own currency, and can therefore leave the EU with minimal disruption to its financial system (trade in goods is another matter), Italy would need to adopt a new currency and rewire its entire financial system. The new currency would be worth less than the euro, meaning the burden of euro-denominated debt including the €2.3 trillion the government has borrowed. In other words, financial chaos would ensue. (Scottish independence from the UK, which will be increasingly called for in a no-deal Brexit scenario, faces the same obstacle.)

South Africa: fiscal risks, high yields

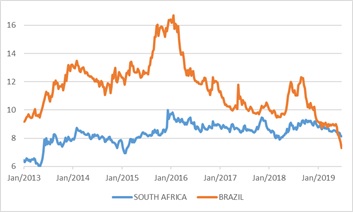

The local tax season has just kicked off and SARS is already lowering expectations on meeting its ambitious R1.5 trillion revenue target. On the spending side, President Ramaphosa has committed to fast-tracking a R230 billion bailout for Eskom, which will add to the long list of spending needs. (Hopefully details on Eskom’s unbundling will be shared soon.) The October Medium Term budget is therefore likely to adjust the budget deficit estimate (the difference between expected revenue and spending) from 4.5% of GDP to closer to 6% for the current fiscal year. Fiscal consolidation remains a pipe-dream for the foreseeable future, unless the economy picks up speed (which should boost tax revenue) or bond yields decline significantly (reducing borrowing costs). Tax rate increases and spending cuts would also be required. This will be very unpopular but potentially also counterproductive, as it would weaken the economy. So why would anyone touch South African government bonds? The simple answer is that yields are already high (bond prices low), pricing in the worst case of a ratings downgrade. South Africa’s government bond yields are now higher than Brazil’s both in dollar and local currency terms, even though Brazil’s credit ratings are lower. South Africa still clings on to a single investment grade rating from Moody’s on its local currency government debt (which is 90% of the total). Losing this last stamp of approval would see local bonds excluded from the FTSE World Government Bond Index. Funds that track this index would be forced to sell, but no one is sure exactly how large this group of investors is, since South Africa constitutes less than 1% of the index. South Africa saw billions of net selling by foreign investors last year, and the bond market did not collapse. Most investors care more about the yield than the rating.

Chart 3: South African and Brazilian 10-year local currency government bond yields

Source: Refinitiv

Food for thought

So there is lots to think about and keep an eye on in the coming months. The trick is not to overreact to developments, but to always ask how much the market has priced in. By the time something hits the front page, it is usually old news as far as the market price is concerned. But from time to time there are genuine surprises and shocks. The best defensive against these is to maintain an appropriate level of diversification.