Greenbacks, green shoots and greener pastures

Global investor sentiment has turned positive. Fears of a global recession that pushed $17 trillion of bonds into negative-yielding territory mid-year are abating.

The US benchmark equity index, the S&P 500, hit a fresh record high last week, as did the global benchmark MSCI All Countries World Index (ACWI) if dividends are included. Gold is down almost $100 from its September peak of $1548 per ounce, a six-year high.

Global fund manager surveys showing higher equity allocations in balanced funds and retail investor flows into equity products have started increasing. The flows don’t cause higher prices, since for every buyer there has to be a seller, but they do point to an improved sentiment among many investors. It is not unusual for investors to turn bullish after the market has rallied, as chasing performance is unfortunately all too common. Many investors cannot resist piling into the share, asset class or fund that has delivered good recent returns. This tends to lead to buying high and selling low, a recipe for mediocre longer-term returns.

Missing out

In fact, the same can be said not just of the past month, but the past decade. Following the trauma of the Global Financial Crisis, and the 60% peak-to-trough decline in global stocks in 2008/2009, investors continuously looked over their shoulders for the next crisis, crash or calamity. Granted, there were three nasty pull-backs (2011, 2015 and late 2018), but the market continued to grind higher, delivering what has often been termed the most unloved bull market ever.

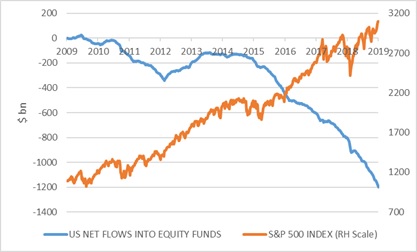

If you were clever or lucky enough to buy right at the bottom in March 2009, you would have tripled your money in dollar terms in the ACWI (with dividends reinvested). If you’d waited only six months for the dust to settle, the return would still be respectable, but much lower at 150%. Yet, the past decade has seen net outflows from equity funds and net inflows into bond funds. To use the US example, industry data shows a cumulative $1.3 trillion inflow to bond funds and a $1.1 trillion net outflow from equity funds over the past ten years. US equities outperformed bonds fivefold over this period. Talk about missing out.

Chart 1: S&P 500 and equity fund net flows

Source: Refinitiv Datastream and Investment Company Institute

Is it justified?

Whether this turn in optimism is justified is another question. The world still awaits confirmation of a trade deal between the US and China. Last week, US President Trump told an audience of Wall Street heavyweights that the deal is still coming, but also that he would not hesitate to hike tariffs further should the negotiations fail. With equity markets having rallied on the expectation of a deal, the latter outcome would be very negative. But that would also hurt Trump’s re-election chances, since he has nominated the stock market as the main barometer of his presidency. The market knows this.

Though the Chinese do not have to contend with such niceties as elections and other democratic processes – just ask the residents of Hong Kong, battling it out on the streets - they also face pressure to agree to a trade deal that brings interim relief. The latest round of Chinese data releases were below expectations and point to a continued slowing of the world’s number two economy. Retail sales growth slowed to 7.2% and industrial production to 4.7% year-on-year. The stimulus measures implemented thus far have not had a huge impact yet, but there is more that can be done. Clearly, the Chinese also have a strong incentive to make a deal.

Elsewhere though, the data is improving. IHS Markit’s Global Manufacturing Purchasing Manager’s Index rose for the third consecutive month in October and is back in positive territory. This is significant, since it was the slump in manufacturing that pulled global growth rates down. It doesn’t mean that we’re off to the races, just that things are not as bad as feared a few months ago.

Even Germany, more exposed to the manufacturing contraction than most countries, posted a surprise positive third quarter growth. Most economists expected a second consecutive negative quarter and hence a technical recession. Closely watched sentiment indicators from the Ifo and ZEW institutes have also tentatively turned for the better, but the outlook is not rosy. Daimler, parent company of Mercedes Benz, announced that it would need to cut costs by €1.3 billion to adjust to a new global landscape. Importantly, if all else fails, there are still the central banks. Monetary policymakers are doing what they can to prevent the slowdown from becoming something nastier, even if their ability to raise growth and inflation is limited.

Lower interest rates already have a positive impact, at least in the US. The housing market, the most important interest rate-sensitive sector, is picking up momentum. Sales of new homes are posting double digit growth rates in the past few months, after declining from late last year as a result of the earlier increase in interest rates (now largely reversed). The Fed’s holdings of bonds also increased above $4 trillion due to interventions to provide liquidity to short-term money markets and thereby ensuring that the healthy flow of credit to the broader economy is not impeded.

An upbeat Jerome Powell, Chair of the Federal Reserve (the Fed), told Congress last week that after three ‘insurance’ rate cuts, he saw no reason to fear that the US economy might fall into recession. The economy remains supported by consumer spending and there are few signs of dangerous imbalances building up. It also means that markets should not expect further cuts from the Fed – unless of course the outlook changes

Strong dollar

One indicator that has not given a bullish signal yet is the US dollar. The dollar dipped in October (leading to a firmer rand), but has picked up again over the past two weeks. Its broad firming trend still seems intact. In theory, the Fed’s cuts should weigh on the dollar, but of course other central banks have also cut rates, and US economic growth of around 2% is ahead of other developed markets.

A strong dollar is both a cause and symptom of the world’s problems. A cause, because an expensive dollar constrains activity in other parts of the world, particularly emerging markets whose weaker currencies put upward pressure on interest rates and inflation. A strong dollar also tends to put downward pressure on commodity prices. The strong dollar is also a symptom of nervous markets and a weak economy, since it tends to reflect risk appetite. Skittish investors tend to flee to the safety of the greenback. If they become comfortable with taking risks outside the US, the dollar tends to weaken.

Still looking for green shoots

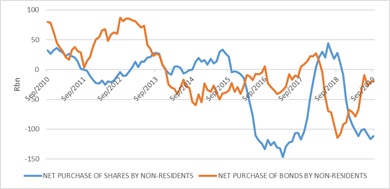

While the green shoots of recovery are sprouting globally, and market optimism has seized on this, there are no similar indicators locally. Both the local equity and bond market foreign inflows remain negative. Again, this does not imply lower prices, but does imply poor sentiment. Foreign investors are, on a net basis, not excited about South Africa. (In other words, although foreign investors have made substantial purchases of bonds and equities over the past year, there were more sales.)

Chart 2: Rolling 12-month sum of net foreign purchases

Source: South African Reserve Bank

Locally, the economic news has not been good. With the release of third quarter sector data by Stats SA, one can get a good idea of what the overall GDP print is likely to be. The official growth number will be released on 3 December. Unfortunately, the chances are that it will be negative again, following a 3.1% contraction in the first quarter and a 3.1% rebound in the second.

Mining production contracted 1.8% on a seasonally adjusted basis in the three months to September from the three months to June. Manufacturing and electricity production also declined in the quarter. Retail sales growth was flat in real terms in the quarter, and barely positive over one year. In nominal terms (adding back inflation) growth was only 3.1%. Therefore, inflation across the retail industry was less than 3% in the year to September. This reflects companies’ lack of pricing power in a tough economic environment. Push up your prices too much and your customers will desert you.

Under different conditions, this would result in an interest rate cut this week. However, the Reserve Bank is likely to remain on pause, wary of negative investor sentiment towards South Africa in light of our fiscal problems and the possibility of further downgrades. Like many commentators, the Reserve Bank probably overstates these risks. But the fact that the Fed has shifted from a cutting to a holding stance also means the window might have closed (and an opportunity to provide relief missed).

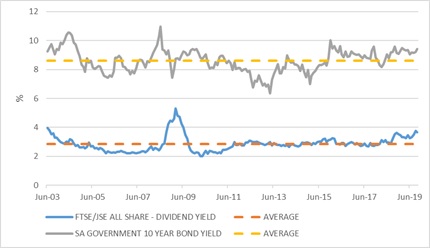

Chart 3: 10-year government bond yield and dividend yield on the FTSE/JSE All Share

Index

Source: Refinitiv Datastream

If foreigners have been selling bonds and equities, it implies that locals have been buying, perhaps recognising that these assets offer value. For investors to get really excited about South African bonds and equities will probably require indications that economic growth is improving, supported by the right policy reforms from government. This will have to include steps to reduce the unsustainable rise in government debt.

However, we also need a supportive global environment. South African assets are not going to rally if global investors become risk-averse. But decent returns might not need a rally. The dividend yield on local equities is close to a 10-year high at 3.7%, and not far behind the current inflation rate. Long-bond yields are 4% to 5% above inflation. So while there is still no widespread optimism in South Africa, it doesn’t mean local investors should assume the grass is greener on the other side. An appropriately diversified portfolio should have exposure to local and global assets.