Gold is under-owned by investors ... for now

Mark Lacey, Fund Manager, Equities at global asset manager at Schroders

There could be a great rebalancing from passive ETFs and other traditional investments back towards gold, which would boost demand for gold and gold-related equities for years to come.

Given the recent pick-up in both gold and gold equity prices, it is important to stress that gold as an asset class remains extremely under-owned. The positive investment cycle in this asset class potentially has many years to run. This is according to Mark Lacey, Fund Manager, Equities at global asset manager, Schroders.

What does under-owned mean?

“Despite having a solid track record as a currency of last resort in times of uncertainty, and despite the current global environment being arguably more uncertain than any point since the second world war, current gold ETF holdings as a percentage of global ETF assets are tiny,” says James Luke, Fund Manager, Metal at Schroders.

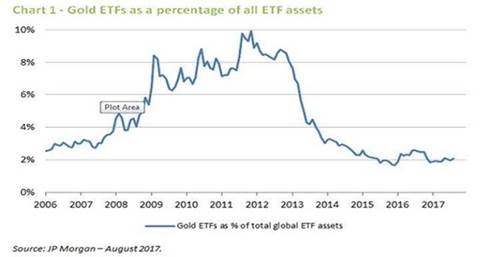

An ETF (short for exchange-traded fund) is a security that tracks an index. Lacey references chart 1 below to show that in 2012 gold was relatively well-owned, with gold ETFs over 10% of all ETF assets (including equities, bonds etc).

“Since then ETFs have expanded across asset classes while we have seen strong bull markets in bonds and equities. At the same time, and partly as a result, gold ETF holdings have fallen from over 85 million ounces in 2012 to around 68 million ounces (in August). Gold ETFs as a percentage of all ETF assets are now closer to 2%,” says Lacey.

According to Luke, “For gold, in a world still awash in liquidity and with financial asset values very high, this is positive.”

Luke continues, “We are not suggesting that ETF holdings in gold are not increasing; we have already seen total ETF holdings of gold increase by 32% in 2016 and by a further 8% year-to-date 2017.

“What we are saying is that around $15 trillion of liquidity has been injected into global financial markets from central banks since 2008. So, when investors start meaningfully allocating to gold again, gold ETF holdings have the potential to grow at significantly higher rates than we saw during the 2004 to 2012 period.”

Gold equities

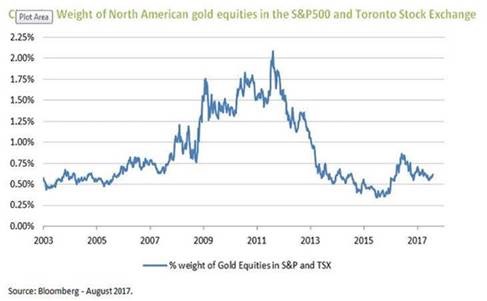

Lacey says, “Now if we look at gold equities, we see a similar picture (see chart 2). The current weighting of North American gold equities in the S&P500 and TSX has fallen to just 0.6% after reaching a peak of over 2% in 2012.”

“To put this low weighting in perspective”, says Luke, “the entire North American (US & Canadian) gold producers have a combined market cap of less than $150 billion. This is tiny and highlights the scarcity value of gold equities if a bull market in gold gets going. Essentially, this extremely low weighting reflects investors’ current low positioning around gold and gold equities, as well as the very high valuations of other more mainstream sub-sectors.”

“This relatively low weighting surprises us given increasing geo-political risk, increasing risk of inflation and therefore negative real rates. Also, given that the majority of the companies we invest in have improving fundamentals and are trading at the lower end of their historical valuation range,” says Luke.

Lacey concludes, “Relative to gold, we believe gold equities still look cheap and we would stress that our equity holdings are currently discounting gold prices of less than $1,200/oz, at a time when the actual gold price is $1327 (as at 12 September),” says Lacey.