Global real estate offers alternative to South African options

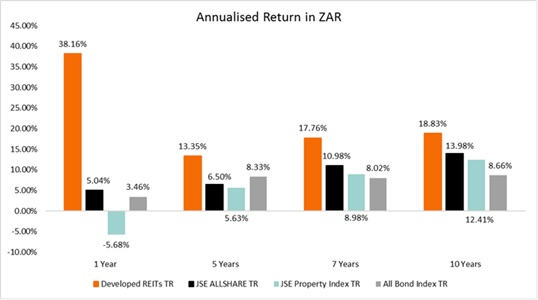

Global real estate has outperformed SA equities, SA bonds, and SA listed property over a 1, 5, 7 and 10 year basis, making it an excellent alternative.

Through global real estate, investors are exposed to multiple developed market economies, which have been growing at healthy levels. With good active management, investors can continue to gain exposure to higher growth regions, and stocks within those regions, which are independent of the weak SA economic and political environment.

South African investors have had a tough time of late: specific landmines have hurt investment returns, which have occurred on the back of a few years of tepid returns from the equity market. Many investors are left scratching their heads, searching for the double digit returns of yesteryear to which they had become accustomed.

According to co-Portfolio Manager of the Fairtree Global Real Estate Prescient Fund (FAIRTREE GLOBAL REAL ESTATE PRESCIENT FUND), Ryan Cloete, South African listed real estate has been an asset class beloved by many investors.

“However, local market fundamentals are looking weak, with an oversupply of space in most sub-sectors, combined with a weak demand outlook on the back of a tough SA macro backdrop. This makes it unlikely for South African real estate to return to its glory days anytime soon,” said Cloete. However, he believes that investors should be looking toward global real estate which exhibits favourable investment characteristics, and stronger fundamentals.

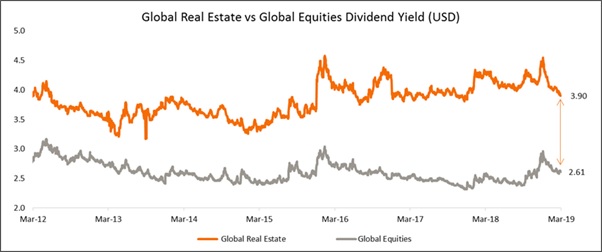

“Global real estate investors have consistently received a high dividend yield from this asset class. This forms an important component of total shareholder return, as many investors may prefer to only draw dividends and leave their capital to grow,” said Cloete.

“Furthermore, the Rand has depreciated against developed market currencies by on average 4% - 6% per annum over the past 20 years. This means that SA investors in global real estate have made 4% - 6% return every year on currency alone, over and above the USD product return,” added Cloete.

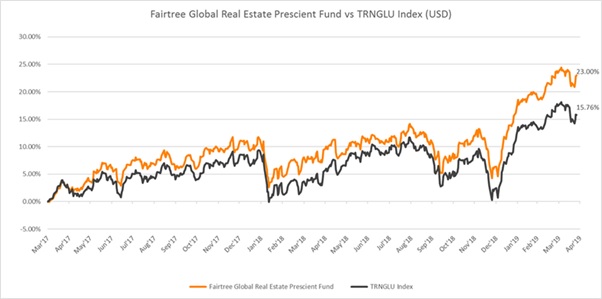

Since the FAIRTREE GLOBAL REAL ESTATE PRESCIENT FUND’s inception, two years ago, the Fund has outperformed its index significantly. During calendar year 2018 it returned 9.4% in ZAR, first amongst its 15 peers, outperforming the index by 144bps*.

“YTD 2019 we have outperformed the index by 158bps*, again ranking highly against our peers,” said co-Portfolio Manager, Rob Hart.

Hart attributes the outperformance to several factors:

1. Three Bites of the Apple. This is a top-down led investment approach where firstly we choose the weighting of the geographical region based on economic, political and other factors. An example of this would be to be underweight Europe as a region because of the weak economic and uncertain political environment.

Secondly, we choose the sector weightings based on global sector thematics, supply/demand and other factors. An example of this would be to overweight industrial stocks globally based largely on increased demand from e-commerce.

Thirdly, we choose the stocks within these regions and sectors based on stock specific characteristics including the quality of the assets and management, valuations and other factors.

2. This process results in a concentrated portfolio of 30-40 names which tick all of our boxes in terms of region, sector and stock. We prefer a concentrated portfolio as we are active managers and do not want to hug the benchmark, and it allows us to keep on top of the stocks and run a best ideas portfolio where new ideas replace dated ones on a regular basis.

3. Another differentiating characteristic is that we have chosen an index with more Asia in it than our competitors, not only because of our expertise in that region, but also because we believe that the global developed market indicies will all have a greater proportion of Asia in them over time as Asia becomes more developed, and we would like to be ahead of that trend.

4. There are also several advantages related to being under the Fairtree Asset Management umbrella. Because of Fairtree’s relatively large size in a South African context, we have excellent sell-side access, which allows us to tap the sellside for information as well as set up meetings with the corporates at various events around the world. We also utilize Fairtree’s comprehensive team of operational and support staff at a significantly lower cost of having to set up that infrastructure ourselves, and we have more efficient trading with lower costs than our peers.

The combination of all these factors has allowed us to outperform our index (see chart below) and our peers since inception - a trend we hope to maintain in future.