Global growth downgraded

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

Once again, global growth is disappointing. For the fourth year in a row, the optimism felt at the start of the year has proven to be misplaced. The title of the International Monetary Fund’s (IMF’s) January report was a hopeful “Is the tide rising?” The title for the latest October report is more circumspect, “Legacies, clouds and uncertainties”. The IMF’s updated forecasts are for global growth to average 3.3% in 2014, rising to 3.8% in 2015. This is slightly lower than the IMF’s forecasts in July and 0.4% lower than the January forecast. The only major economy to see its growth forecasts upgraded significantly was the US. The world’s largest economy is expected to grow by 2.2% this year and 3.1% next year. The forecast for the Eurozone and Japan has been cut for both 2014 and 2015 to around 1% per year. The IMF attaches a 40% probability to a triple-dip recession in the Eurozone, a concern amplified by the release of weak German industrial production numbers for August on Monday. China’s growth outlook remains the same at 7.4%.

US carrying the load

The growth momentum in the developed world is being provided almost entirely by the US, as confirmed by recent strong labour market data (unemployment has now fallen to 5.9%). Lower unemployment, lower levels of household debt, a profitable corporate sector and reduced fiscal austerity point to sustainable growth in the US. Nonetheless, it is worth remembering that this remains the weakest post-recession recovery since World War II. Wage and price inflation and credit growth remain low, giving the Federal Reserve (the Fed) scope to leave interest rates unchanged until next year.

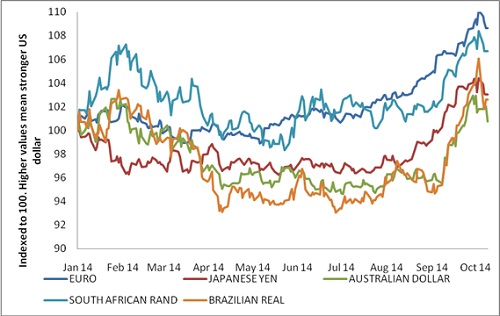

But when rates do start rising, it will pose a threat to the US and the world economy. We’ve already seen the dollar rallying in anticipation of higher rates. This has contributed to plunging commodity prices as well as widespread havoc in emerging market currencies.

The IMF also warns that developed countries face ‘secular stagnation’, low growth due to aging populations and excess savings relative to investment, despite low interest rates. Its suggested cure is to ramp up infrastructure spending, but the main advanced economies remain reluctant to loosen fiscal policy. In the Eurozone, the threat of outright deflation is real with inflation at 0.3%, growth slowing and commodity prices falling.

Emerging markets growing slower

Emerging markets are still expected to provide the bulk of global economic growth, but while they should still grow faster than developed economies, they are growing at lower rates than in the past, and also at lower rates than what was generally expected by investors. Hence the four-year long relative underperformance of emerging market equities. Brazil, Russia and the Middle East have seen growth forecasts cut. Since 2011, the BRICs - Brazil, India, China and Russia - account for half the IMF’s forecast misses.

Market reaction

Markets responded negatively to the IMF’s report, perhaps also because the IMF specifically warned that markets were not pricing in all the risks to the global economy. (The IMF itself might be pricing in too much risk, warning of the impact of an oil price spike at the time when oil prices are plunging).

Later in the week, the mood on world markets perked up temporarily when minutes from the Fed’s September monetary policy meeting revealed a concern that weak growth outside the US and a strengthening dollar will harm export earnings and keep inflation low, justifying low interest rates. The stronger dollar reflects the view that interest rates will rise, but a stronger dollar also does some of the work of higher rates, thus possibly postponing or limiting the actual rate increases. The dollar came off its highs by the end of the week, taking some pressure of the rand. The timing and nature of US interest rate hikes will nonetheless dominate how investors worldwide allocate capital over the next few months. The Fed itself is likely to be very careful to avoid hiking before the US economy is healthy enough to absorb positive real interest rates. But at no stage in the six years after the financial crisis has the Fed taken action to mitigate the impact of its actions outside US borders (not that there was much it could do). Other economies will have to fend for themselves, a lesson incoming SA Reserve Bank Governor Lesetja Kganyago has likely taken to heart.

Chart 1: Currencies against the US dollar in 2014

Source: Datastream

SA outlook still bleak

The IMF cut South Africa’s growth outlook to 1.4% in 2014 and 2.3% in 2015. This is down from the July set of forecasts (for 1.7% and 2.7% respectively) and below the most recent forecasts of the South African Reserve Bank (SARB). With most of the year behind us, there is not much hope for improving on 2013’s 1.9% growth rate.

The pertinent question is whether there will be a rebound next year. Bear in mind that 2014 was supposed to be the rebound year after 2013’s disappointing growth. The SARB’s forecast this time last year was for 2014 to deliver 3% growth. A repeat of the damaging five-month platinum strike is unlikely, but the other conditions that led to disappointing growth in 2014 are set to remain in place next year: tighter monetary policy, poor consumer and business confidence, lower commodity prices, and relatively high inflation. Fiscal policy is also set to get tighter as the pressure grows on government to close the budget deficit. Government is running behind its targets for the current fiscal year, making the targets for the following years even more ambitious, and tax hikes a real possibility. The IMF’s improved outlook for 2015 compared to 2014 is largely due to an improvement in exports.

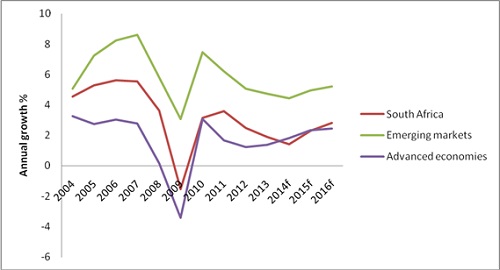

As the chart below shows, South Africa’s growth profile appears to be closer to a mature developed economy than a fast-growing (relatively) emerging market. Unfortunately, we need emerging market rates of growth to deal with emerging market levels of poverty. President Zuma’s target of 5% growth by 2019 seems unrealistic with the IMF expecting growth to only be around 2.8% (though any forecast that far into the future is suspect). One silver lining is that growth rates in the rest of Africa are expected to remain robust, and it is no surprise that South African companies continue to expand into the rest of the continent out of their slow-growing home market. If things go as planned, South African shareholders (and the taxman) will benefit but not necessarily South African workers.

Mining and manufacturing still weak

Turning to the latest local economic data, mining production fell 10.1% year-on-year in August, with platinum output levels still 45% lower than a year ago as the sector recovers from the five-month long strike. (Lonmin announced this week that its mines had returned to full production ahead of schedule, but still four months after the end of the strike.) Seasonally-adjusted mining production decreased by 1.1% in the three months ending August 2014 compared with the previous three months. Apart from platinum, coal, gold and chromium output fell over the three-month period. Production of iron ore remains healthy despite the plunging dollar prices, growing 4.7% over the three-month period.

Manufacturing production decreased by 1.2% year-on-year in August, up from -8% in July. Seasonally-adjusted manufacturing production fell by 1.4% in the three months to end August compared with the previous three months. Both mining and manufacturing appear to be on track for a negative performance in the third quarter. The big drivers for August’s manufacturing decline were the11% slump in the wood, paper and publishing industry and a 4% decline in petroleum and chemical production.

The IMF specifically pointed to South Africa’s infrastructure constraints, especially the availability of electricity. The mining and manufacturing sectors are the most energy intensive in the local economy, and thus exposed to electricity supply interruptions, as well as the 12% tariff increase granted to Eskom as of next year.

Chart 2: Economic growth: SA, emerging markets and developed economies

Source: International Monetary Fund, forecasts from 2014 onwards