Global economy is experiencing rapid growth, but things are still clearly far from normal

Thousands of learners celebrated Spring Day last week, even though purists will insist that the season only turns officially on the equinox on the 22nd. Mother Nature, of course, doesn’t care two hoots about human timetables. It was still freezing across large parts of the country, Spring Day or not.

Today’s 24/7 financial markets also don’t really care where we are on the calendar. Still, month-end always provides a convenient point to pause and take stock of market returns and the major economic developments that drive them.

Starting with economic matters, at the end of August, the global economy was experiencing rapid growth as it recovered from last year’s record collapse. But things are still clearly far from normal. Offices are still very empty in the world’s major business and financial centres. Global demand for goods is well above long-term trends, while spending on services is still below those trends, especially services such as travel, leisure and hospitality. The supply of many key inputs, including labour, is not yet back to normal and businesses continue to complain of delays, shortages and elevated input prices.

And of course, the pandemic itself is far from over. Total global business activity has not been interrupted as much by the Delta variant as feared earlier, but in some places the impact has been notable, including in China and elsewhere in Asia.

Cooling China

Chinese business activity seems to be cooling more than expected, partly because of the impact of the Delta wave that sent the official services purchasing managers’ index into contractionary territory in August for the first time since March 2020. But it also appears that Chinese policymakers tapped the brakes too hard earlier in the year. They are now easing up on macro-policy measures, but there is no sign yet of easing the tightening of restrictions on technology use. The People’s Bank of China cut banks’ reserve requirement ratio (RRR), a move that should allow for more lending. Further RRR cuts are likely.

But the most important central bank remains the US Federal Reserve (the Fed). The Fed currently has a policy interest rate near zero, and also buys $120 billion in Treasuries and mortgage-backed securities each month. With the US economy making progress towards the Fed’s twin objectives of maximum employment and inflation that stabilises at 2% over time, a number of Fed officials have argued that it is time to start reducing or “tapering” the asset purchases.

Fed Chair Jerome Powell used the annual Jackson Hole central banking symposium to note that he was in the camp that favoured a reduction in asset purchases later this year as long as economic conditions continued to evolve as expected. However, he emphasised that this should not be seen as a prelude to interest rate increases. The latter does not depend on mere progress towards achieving the Fed’s goals; it requires those goals to actually be reached. This is a much tougher hurdle. Investors cheered this outcome, and a feared rerun of the 2013 “taper tantrum” has not materialised.

In fact, global equities were positive for the seventh consecutive month in August with the MSCI All Country World Index closing at an all-time high. It returned 2.5% in the month in US dollars, lifting the year-to-date gain to 16%. The 12-month return was 28%. A string of seven straight positive months is rather unusual. Markets don’t move up in a straight line, and no-one should be surprised if there is a negative month or two in our near future. However, the overall macro backdrop of positive economic growth and policy support remains reassuring to equity investors.

In terms of regions, the US S&P 500 returned 3% in August and an impressive 31% over one year. The Eurostoxx 600 Index returned 2.2% in the month and 31.8% over one year in euros. Japanese equities bounced back from a big drop in July, with the Nikkei 225 returning 3% in yen in August. The 12-month performance of 23.4% lags the other major developed markets.

Emerging market equities also rebounded from sharp losses in July caused by the regulatory crackdown on China’s technology sector. The MSCI Emerging Market Index returned 2.6% in August in dollars but still lags developed markets by some distance on a year-to-date basis with a return of only 3%. Over one year, the index return was 21%.

Global bond yields have increased somewhat, leading to negative returns in August (bond yields and prices move in opposite directions). However, the losses in the bond market were nowhere near as bad as in 2013 or even earlier this year. The benchmark US 10-year Treasury yield inched up from 1.2% to 1.3%, but remains extremely low in historical terms.

Chart 1: 10-year US Treasury yield, %

Source: Refinitiv Datastream

Softer commodities

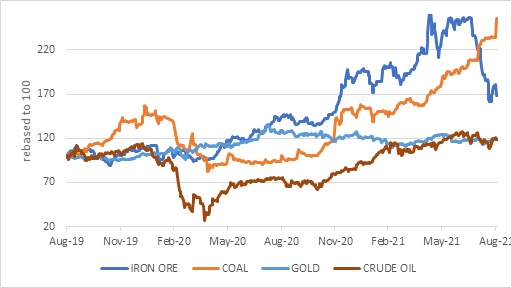

Commodity prices were generally weaker in August. Although brent crude oil was 4% lower in the month, at $72 per barre it was still up 62% from a year ago. Gold closed marginally lower at $1811 per ounce and lost 8% over the past year despite global inflation fears. Platinum and palladium were also negative in the month. Among industrial metals, iron ore fell 18% in August and is now down a third from its recent elevated peak. Copper was also 1% lower in the month.

The notable exception is coal. Coal prices jumped another 12% in the month and are 134% higher than a year ago due to supply concerns. Among other things, China closed its border with Mongolia to prevent the spread of the coronavirus, and this disrupted coal supplies. Ironically, the increased focus of investors on environmental, social and governance (ESG) issues also seems to be a factor. Banks and investors are increasingly (and rightly) refusing to fund coal mine expansions. But coal will still be needed even as the world transitions to greener energy forms. Demand exceed supply for some time before it eventually (hopefully) drops to zero.

Chart 2: Commodity prices in US dollars

Source: Refinitiv Datastream

As South Africa is a major coal exporter, the higher price offsets the declines in iron ore and platinum group metals to an extent. So while South Africa’s overall commodity export price has declined from its recent peak, it is still elevated compared to where it was on the eve of the pandemic.

This should continue to support a strong export performance. July’s trade numbers were negatively impacted by the unrest in Durban and the cyber-attack that forced the country’s major ports to turn to manual processing. However, the R36 billion surplus was still robust by any standard, and the R290 billion surplus for the first seven months of 2021 is three times larger than it was for the corresponding period in 2020.

The Absa Manufacturing Purchasing Managers’ Index for August showed a strong bounce-back from the disruption caused by the unrest and looting. The PMI jumped to 57.9 points in August from 43.5 points in July, with 50 points the dividing line between growth and contraction.

The decline in commodity prices did not seem to have much of an impact on the rand. While the local currency has been volatile in the past three months, strengthening to R13.50 per dollar in early June and then falling all the way to R15.31, it ended the month slightly stronger at R14.47 per dollar once investors gained confidence in the Fed’s policy plans. Over the past year, the rand gained 14% against the dollar, detracting from the dollar returns from global equities and property from the point of view of local investors.

Bigger but not better

One bit of good news is that the local economy is about 11% or R550 billion larger in nominal terms than previously thought. Every few years, Stats SA undertakes a benchmarking and rebasing exercise, incorporating new sources of data and also ensuring that we remain in line with global best practice. It turns out that the estimate of household consumption is much larger than previously thought, and much more skewed towards services and less towards food. This typically happens as societies become richer over time.

However, the growth profile of the economy is basically unchanged. It still grew disappointingly slowly in the five years before the pandemic, and then crashed 6.4% in 2020. The main positive is that the debt-to-GDP and deficit-to-GDP ratios are now somewhat lower.

Clearly the rand amount of government debt is unchanged and still growing too quickly, but it is now being seen in relation to a larger economy and will seem a bit more manageable to investors. Indeed, South African government bonds rallied in August and took the Fed’s taper talk in its stride. The All Bond Index returned 1.7% in August and 14.8% over one year, well ahead of the 3.5% money market return. However, the bond market clearly still reflects a huge degree of concern over the country’s fiscal trajectory. Long bond yields are still elevated compared to most of our peer countries, even though the domestic inflation outlook is quite benign.

Local equities were positive in August as measured by the FTSE/JSE Capped SWIX. The FTSE/JSE Capped SWIX returned 2% in the month, which lifted the return for the first eight months of the year to 18.6% and the 12-month return to 30%. Starting points matter in any return calculation: from the bear market trough in late March 2020, FTSE/JSE Capped SWIX returned 88%. The two-year cumulative return, covering both the crash and the rebound, was 26%.

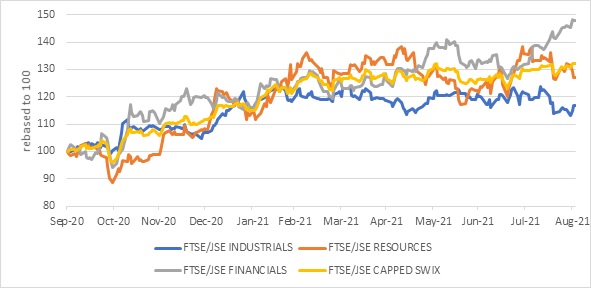

Strikingly, and perhaps unexpectedly, over the last year the returns from local equities have been driven primarily by domestically focused companies. The ‘local local’ shares like banks, insurers and retailers instead of the ‘global local’ shares like Naspers and the miners.

Chart 3: JSE sectors over the past year

Source: Refinitiv Datastream

Weaker commodity prices pulled down the shares of mining companies in the month of August, though Sasol was positive. The resources index lost 4.8% in the month but has still given investors a 25.5% return over 12 months. The industrials index was also deeply negative in August due to double digit losses from Richemont and Naspers. It lost 4.5% in August, dragging year-to-date returns down to 9.8% and 12-month returns to 16%.

On the other hand, financials were strongly positive in August, gaining 12%. Banks and life insurers, sectors mostly exposed to the domestic economy, both delivered double digit returns. This means the financials index returned 51% over 12 months,

Listed property was also up strongly in August. The FTSE/JSE All Property Index returned 7% in the month and 28% so far this year to lift 12-month returns to 52%. Despite this impressive recent performance, the index has yet to return to pre-pandemic levels.

More of the same

Spring is traditionally associated with rebirth, rejuvenation and new beginnings. Given the difficult period we’ve been through in terms of illness and loss of life, as well as the disruption to the economy and many people’s livelihoods, we may indeed hope that spring brings renewal and positive change. From an investment point of view, however, it should be a case of more of the same: remain invested, remain diversified and remain patient.