Fuel to the fire

Hurricane Michael smashed into the US Gulf Coast last week, leaving a trail of destruction in its wake. It unexpectedly and rapidly developed from a tropical storm into one of the most powerful Category 4 hurricanes in decades.

Similarly, it seemed like a storm tore through global markets over the past two weeks, also with little warning.

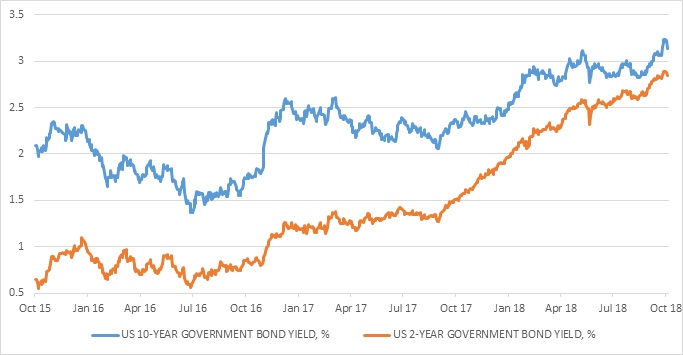

In very simple terms, the market is worried about rising US interest rates. Even President Trump asked if the Federal Reserve (the Fed) had gone crazy. In fact, the Fed has been very clear for a while that rates would be rising, but at a gradual pace, as it has been since 2015. What has changed is that investors increasingly believe the Fed, having until recently doubted it. The Fed’s so-called dot plot – a summary of the forecasts of its various policymakers – points to its policy rate hitting 3.4% by the end of 2020 from 2.25% currently. The 2-year government bond yield, which should closely reflect these expected rate increases, was only 1.9% at the start of the year. It is now a full percentage point higher. However, five years ago, it was only 0.6%, so much of the adjustment is already behind us. The benchmark 10-year bond yield spent most of the year hovering around 3%, but shot up to 3.2% recently, before pulling back somewhat.

Strong, but not overheating

Fed Chair Jerome Powell has vowed to follow a pragmatic approach of considering the incoming data, rather than being guided by the largely theoretical constructs of “natural” unemployment and interest rates. But the incoming data has been particularly strong for the US, with the unemployment rate declining to 3.9%, a level last seen when Neil Armstrong set foot on the moon. Therefore higher interest rates are warranted.

Importantly, despite the strong economy, there is no sign of overheating in the US, with inflation still well-behaved and wage growth still below 3%. In fact, the latest consumer price reading showed inflation coming in below expectations at 2.3%, the lowest inflation rate in seven months. Therefore, there is still no reason to expect that Powell and company will have to, or will want to, hike rates aggressively.

Markets are re-pricing interest rate expectations, rather than questioning the strong underlying economic growth and the profit-generating ability of US companies.

For the world economy as a whole, the outlook is still good, but somewhat less rosy. The latest World Economic Outlook by the International Monetary Fund (IMF) shows that global growth in 2018 and 2019 is likely to be slightly below the April prediction. But the 3.8% real growth expected in both years is still solid compared to the preceding years. Europe and several non-oil producing emerging markets have seen their forecasts cut. While the IMF warned about high global debt levels, interest rates remain historically low (even in the US) and borrowers are generally still in a position to service debts, outside isolated cases like Turkey.

Tech wrecked

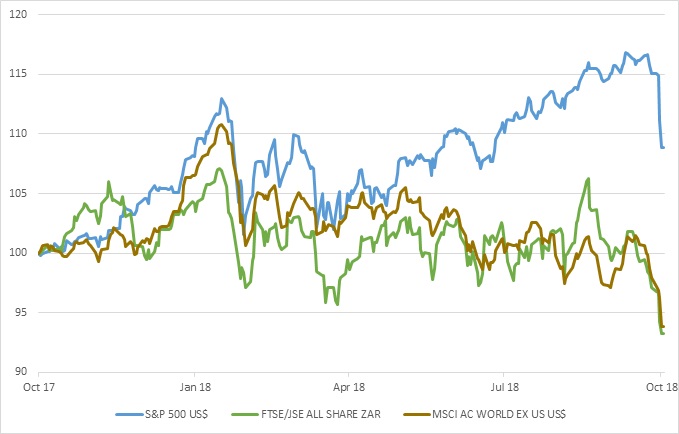

The consensus view of Donald Trump’s trade wars is also shifting. Having settled with Europe and his North American neighbours, he has focused his attention on China. And while he has railed against China’s trade surplus with the US and intellectual property theft, there is a camp in the White House that clearly wants to limit China’s rise as a superpower, especially in the arena of technology and given growing cybersecurity concerns. Currently however, most US technology companies rely heavily on China for manufacturing computer chips and other components. Apart from the prospect of higher interest rates, which should lower the price-earnings multiples shares trade on, tensions with China have weighed on the high-flying tech sector particularly heavily. The NYSE FANG+ shares (including many market-darlings like Apple, Amazon and Google) have fallen 9% in October alone, versus 5% for the broader US market. China’s biggest tech stock, Tencent – and also South Africa’s, due to the Naspers shareholding - has declined by 30% this year.

Collateral damage

We thankfully don’t have hurricanes in South Africa, but our markets almost never escape global financial storms. The JSE has therefore taken blows from all sides. Local economic growth has been disappointing this year and political uncertainty returned after a brief spell of ‘Ramaphoria’. The negative sentiment towards emerging markets has seen capital outflows from many of these markets. And of course, when the American market stumbles, other markets tend to fall over. Finally, there have also been a number of stock-specific issues that have little to do with the macroeconomic environment but relate to governance (MTN, Steinhoff and Resilient), industry disruption (British American Tobacco) and offshore acquisitions that have not worked out (Mediclinic, Woolworths and Aspen). Literally only a handful of shares have not seen losses this year, and some share prices have fallen as if it is a repeat of the 2008 crash.

The FTSE/JSE All Share Index is therefore down 7.5% year-to-date, and longer-term returns have been dragged down. However, a lot of bad news is now being priced into the market, and the current forward price-earnings ratio is at a five-year low, suggesting decent real return prospects going forward.

Bonds also struggled

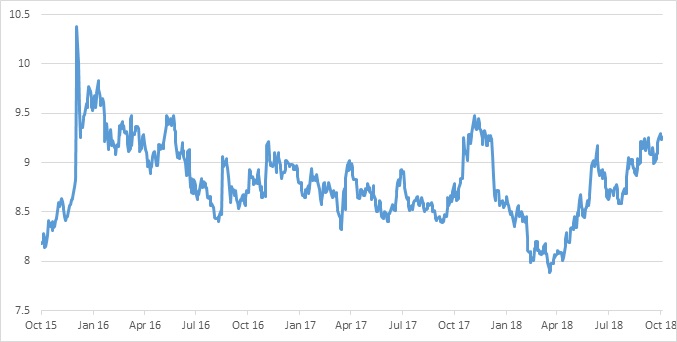

Local bonds have also struggled in the face of outflows from emerging markets and rising US bond yields (bond prices and yields move in opposite directions). The local 10-year government bond yield has increased from 8.6% at the start of the year to 9.26% at the end of last week. Unlike in the US, the yield is high enough to offset the decline in bond prices this year and the All Bond Index is still in positive territory year-to-date.

At current levels, bond yields are still very attractive, and appear to price in Reserve Bank interest rate hikes. Though inflation is likely to rise in the face of the higher oil price, it is unlikely to result in a sustained breach of the inflation target range, and the medium-term inflation outlook is still bond-friendly. Meanwhile, the appointment of the highly regarded Tito Mboweni as finance minister clears up a source of uncertainty ahead of next week’s Medium Term Budget Policy Statement. (MTBPS). The MTBPS will be largely finalised already, and if Minister Mboweni introduces changes to the fiscal policy it will only plausibly be felt in next year’s Budget. Longer term, he can be expected to place emphasis on continued fiscal consolidation and steer the mix of spending to better support economic growth (more capital spending relative to wages).

As the economy has performed much worse than expected this year, the MTBPS is likely to see the 3.6% of GDP deficit target missed for the current fiscal year, and deficit projections for the following years also raised slightly. This will largely be priced in already.

The final risk factor for bonds is credit ratings. Moody’s, the only agency that rates South African local currency government debt (90% of the total) as investment grade, postponed its expected rating announcement, without providing a new date. South Africa therefore remains a member of the FTSE World Government Bond Index. Removal would have resulted in index-tracking funds pulling more capital from the bond market. Most foreign investors, however, care more about returns than credit ratings, and as sentiment towards emerging markets soured, they pulled out R50 billion from the local bond market this year, according to JSE data. This money can easily return once the dust has settled.

Riders of the storm

Meteorologists are often teased for their varying forecasting record, but forecasting markets is even more difficult. Storms are complex natural occurrences, but are still the result of physical forces. Markets are shaped by human psychology, the sentiment changes of millions of individual decision-makers. In the short term, anything can happen. Over time though, market prices do converge on underlying economic realities. Our role is to assess which asset classes have diverged too far from the economic reality, increase exposure to the cheap ones and avoid the over-priced ones, while ensuring appropriate diversification.

At risk of stretching the hurricane metaphor too far, unlike a real hurricane, the damage from stormy market conditions is not permanent. It is only when they sell out that investors lock in any losses. Sitting out a hurricane in your house can be dangerous, but riding out market volatility is usually the best approach.

Chart 1: US 2-year and 10-year government bond yields, %

Chart 2: Global equity indices over one year, rebased to 100

Chart 3: South African 10-year government bond yield, %

Source: Thomson Reuters Datastream