From bad to worse to better

The performance of the local equity market this year has been dire, to say the least. After 2017 delivered a 20% return and 2018 kicked off with the promise of positive political and policy change in South Africa, the local market stormed ahead in the first three weeks of January to an all-time high on the FTSE/JSE All Share Index of 61 686 points. But since then everything seems to have gone wrong.

The market is down 16% from that high point, and the index is back where it was in July 2017. The second half of last year saw very strong returns, so year-on-year return numbers will probably be bleak for another few months, even if things stabilise now.

The headwinds

The headwinds for local equities this year can be categorised as global, local and idiosyncratic. Starting with global, because global markets will always set the tone for the JSE, there has been no shortage of macro factors weighing on investors’ minds this year. Top of the list is the path of US interest rate hikes, but also Donald Trump’s trade wars, Italy’s budget stand-off with the European Union, and the ongoing uncertainty around Brexit. Most recently, relations between the West and Saudi Arabia have come under the spotlight following the apparent murder of a US-based Saudi journalist. This comes at a time when the oil price is already uncomfortably high, though it has pulled back the last few days, partly because of strong US shale production.

It has been a particularly tough environment for emerging markets (EM) with global investors pulling capital out of EM bonds and equities. The dollar has strengthened since March, putting pressure on EM that borrowed in hard currency. The combination of higher US bond yields and volatile currencies has made the carry trade – searching for yield in EM – unpopular. Concerns over China’s slowing growth and the additional impact of US tariffs on its economy have not helped. China’s economy expanded by 6.5% in the four quarters to end September, the slowest growth rate in a decade, but still staggeringly fast for an economy of its size. However, it is not just EM that have struggled. Among major global equity markets, the US stands head and shoulders above the others. European shares have also struggled.

As for the local headwinds, there have been plenty. The economy experienced negative growth in the first and second quarters leading to a technical recession. While Cyril Ramaphosa’s ascendency to the presidency caused a jump in sentiment, uncertainty around land expropriation soon dominated the agenda, weighing on business confidence. Record high petrol prices and a VAT increase cut into consumer disposable incomes. Furthermore, the Reserve Bank has continuously warned that it might have to increase rates – already high in real terms – further. Unsurprisingly, it is difficult for companies to grow revenues in this environment. The nominal growth rate for the economy as a whole is only around 6%.

Idiosyncratic or stock-specific issues are largely unconnected to the macro environment and have contributed to the disappointing returns of the non-mining rand hedges in particular this year, despite the weaker rand. These include corporate governance issues (Resilient), run-ins with regulators (MTN and Tencent, which accounts for most of Naspers’s value), and an industry under pressure from changing consumer behaviour (British American Tobacco). A number of companies have also struggled with offshore acquisitions. Mediclinic shares dropped by more than 20% last week, joining Woolworths, Brait, Famous Brands and others who appear to have bitten off more than they could chew in the rush to diversify and escape South Africa’s tepid economy and persistent political uncertainty. Many of these acquisitions were made between 2011 and 2015, when the currency seemed to be a one-way bet.

Not all doom and gloom

Shares that have done well this year include Sasol, unsurprising given the surge in the rand oil price, and the paper companies. The diversified mining heavyweights continue to do well, having turned a corner in early 2016 after deep declines in the prior years. They have continued rallying - Anglo American is up 21% and BHP 16% this year - despite sluggish commodity prices. These companies have streamlined operations, cut costs and reduced debt to such an extent that investors now expect solid earnings growth even if top line growth is modest.

This process of restructuring is playing out across corporate South Africa. Of course cost-cutting contributes to the weak economy in the short term and delayed capital spending can harm growth in the longer term. However, companies are becoming leaner and meaner, and at some point the slightest increase in sales can improve profits substantially.

So what are the latest signals on the state of the local economy? Stats SA data from the last two weeks show that activity has bounced in some sectors. Mining output remains extremely volatile, and fell sharply in August. But retail sales, wholesale sales, manufacturing and building activity have all grown in July and August relative to the three months to September. It is too soon to tell if this is the start of a trend, but it does point to positive economic growth in the third quarter, which would take us out of a technical recession. (In fact, it would mean that the economy was already out of the recession by the time it was announced that it was in a recession.)

Together with the widely lauded appointment of Tito Mboweni as finance minister and President Ramaphosa’s various policy interventions (including this week’s Investment Conference), exiting the technical recession could add to improved business confidence. If that sounds like grasping at straws, remember that sentiment plays an outsized role in business decisions, even though we like to think of corporate leaders as highly rational.

Sentiment plays an even bigger role in financial market investments. Corporate decisions tend to be made in board meetings and committees, but panicked investors can sell at the click of a mouse. Sentiment can turn very quickly and history has shown that the best time to buy is when pessimism is at its highest. The opposite is also true.

Valuation has improved

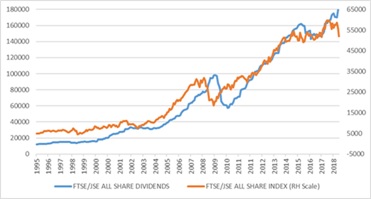

Last year, markets were flat for the first half and sentiment was poor (weak economy, cabinet reshuffles, political uncertainty, credit ratings downgrades). Things quickly turned around without warning and the market shot up 17% in the second half. These turning points cannot be predicted, and you have to be invested to benefit. Valuation rather than forecasting is the best signal and the local market now trades at the lowest forward price: earnings ratio in five years. The dividend yield at 3.5% is the highest since 2009. And while the overall index is below the all-time high, the level of dividends paid has hit a new record, up 14% from a year ago.

The prospects

South African equities remains the main growth asset for most local investors, since regulations limit the global exposure in retirement funds. This means that most balanced funds have material exposure to an asset class that delivered a total return (price movement plus dividends) of -3% over the past year. Investors are rightly concerned. While an unusual set of circumstances contributed to this poor performance, the performance itself is not unusual if we look at history. It is a volatile asset class, but has delivered world-beating real returns for long-term investors. We have no way of knowing when it will turn around, and things might get worse before they get better, but ironically, the worse the recent performance, the better the prospects for future returns.

Chart 1: FTSE/JSE All Share Index dividends paid and price level

Source: Thomson Reuters Datastream

Chart 2: Local equities valuation

Source: Thomson Reuters Datastream

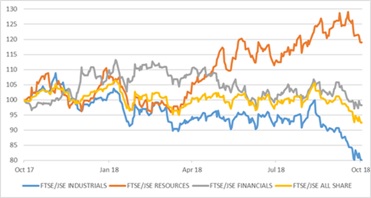

Chart 3: Local equity sectors over the past year

Source: Thomson Reuters Datastream