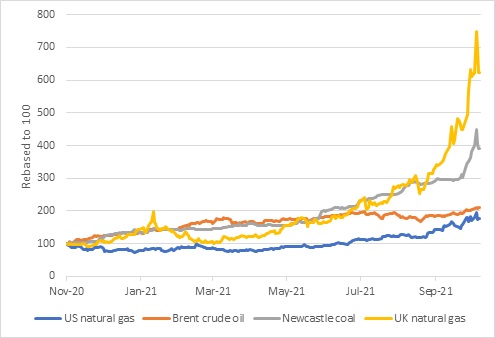

Fossil fuels on fire

These strange times have become even more unusual. Despite the enormous efforts to reduce the demand for carbon-emitting fossil fuels, their prices have shot up in recent weeks.

The upcoming COP26 Glasgow Climate Summit could ironically take place against the backdrop of coal and natural gas prices at record levels and oil at multi-year highs even though the share of renewables in the global energy mix has thankfully risen steadily.

Source: Refinitiv Datastream

A perfect storm

It is a perfect storm of events that got us here. On a positive note, demand for energy has increased from the lockdown-induced lows. For instance, IATA estimates a 26% growth in airline passenger numbers between 2020 and 2021, though they are still more than 40% below 2019 levels. However, this improvement in demand has not been met by rising supply. On the contrary, several factors have constrained supply.

One is simply the weather. Northern Europe relies heavily on electricity from wind, but it has been less windy than usual. Droughts in Brazil, China and the US mean hydro-electrical production has also been lower than normal. This has led to increased demand for natural gas and coal. However, natural gas inventory levels have been lower than usual at storage depots across Europe. This has created an opportunity for Russia, Europe’s main gas provider, to flex its geopolitical muscles and go slow on deliveries, although it has indicated a willingness to stabilise the market recently. With winter looming, natural gas prices in Europe have gone stratospheric, pulling up prices in other parts of the world.

In China, flooding has disrupted domestic coal production. China is already the biggest consumer of coal in the world, but demand has increased recently, and with it, its price. Geopolitics play a role here too. China blocked Australian coal imports, about a tenth of its total last year, after Australia questioned the origins of the coronavirus. Imports from Mongolia have also been disrupted by Covid.

Chinese electricity prices are heavily regulated, and utilities cannot freely pass on the cost of higher coal prices to customers. Many have opted to cut back on production, rather than sell at a loss. Beijing has now announced that selling prices will be allowed to rise somewhat. All this has happened at a time when local governments were already reducing electricity production from coal to curb air pollution and carbon emissions. The net result is something South Africans know well: widespread load-shedding.

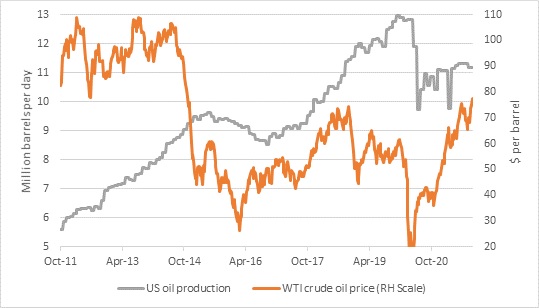

Finally, in terms of oil, OPEC (along with Russia) has largely maintained the production cuts it put in place last year to prop up the oil price. In other words, there is no fundamental shortage of oil. Supply is being deliberately held back. OPEC can increase supply if it worries that high prices will choke off demand, but for now its members seem comfortable with the revenues flowing in. Importantly, the price increase has not yet led to the associated increases in American shale oil production as has been the case over the past decade. Shale producers have largely abandoned the old production-at-all-costs mind-set in favour of maintaining profitability and shareholder returns.

Chart 2: US oil prices and production

Source: Refinitiv Datastream

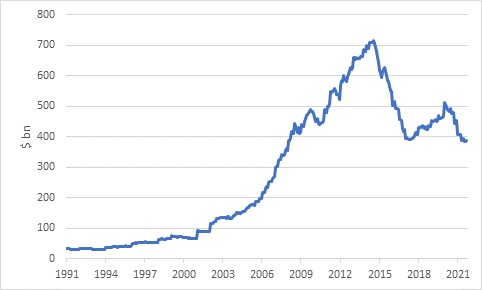

An associated factor is that these companies and their peers face increased difficulty in accessing the funding needed to increase short-term (in the case of shale) and long-term production (in the case of the oil majors). Banks and asset managers across the world are phasing out exposure to fossil fuels and some have already cut all ties. This has contributed to steep declines in capital expenditure by fossil fuel producers.

In other words, the big move among global investors towards embracing environmental, social and governance (ESG) principles might have the unintended consequences of higher fossil fuel prices until such time as renewable sources reach critical mass.

Chart 3: Capital expenditure by listed oil, gas and coal companies

Source: Refinitiv Datastream

The good news is that elevated fossil fuel prices do create a strong incentive to increase investment in alternatives. This is where ESG can play a big role to make sure the alternatives are green, not brown. Economists have long argued that the best way to tackle climate change is to put a tax on carbon emissions. This is because the price we pay for a tank of petrol, for instance, covers the cost of production and distribution but not the cost of the associated air pollution. Since the cost of this externality is not included, petrol is too cheap. This leads to excessive demand. A carbon tax raises the price to its “correct” level and lower demand. The recent price increases could therefore achieve a similar effect.

A tax on your houses

Increased energy prices act as a tax for most consumers. Most of us have no choice but to fill up our car. If you live in the snowy Northern Hemisphere, you have little choice but to heat your home with gas.

In other words, this will be a drag on global consumer spending, the question is just for how long will prices remain elevated. It is somewhat compensated for by the excess savings that households in the rich world have built up, but it also appears that most of the excess savings are concentrated in the hands of more affluent households. Meanwhile, it is lower income households that are most exposed to increases in energy prices and associated rises in food prices. Nonetheless, it is worth pointing out that at around $80/barrel, the oil price is nowhere near the $150/barrel record set in 2008 on the eve of the global financial crisis, or the $100+ levels that prevailed between 2011 and 2014, especially adjusted for inflation or growth in incomes.

The other complication is that these price increase come at a time when inflation rates are already elevated. The global production and delivery of goods is already severely constrained by Covid-related disruptions, shortages of inputs and labour, and logistical bottlenecks. But now production in China, the world’s factory, has to contend with electricity blackouts. This is likely to worsen the supply chain problems already besetting the world economy.

People often confuse higher fuel prices with inflation. Fuel prices are very visible since most motorists have to fill up at least once a month. But inflation refers to sustained price increases in a broad range of consumer goods and services. Energy is a component in consumer price indices and therefore higher energy prices do have a direct short-term impact. But the big question is whether firms can raise their selling prices to compensate for higher input costs. In this way, higher energy costs ripple through the economy. If workers then demand higher wages to compensate, we have the beginnings of a wage-price spiral. This clearly requires pricing power on the part of firms and bargaining power on the part of workers that have been absent for many years. However, in the current Covid-distorted global economy, there have been signs of both.

Winners and losers

There are clear winners from this energy crunch. Net exporters of coal, gas and oil are clearly smiling, particularly countries such as Nigeria that have really struggled until recently.

In contrast, many countries are energy importers and face not only higher inflation rates, but also potentially balance of payments problems as they need to cough up more of their scarce dollars for each barrel of oil. Compounding matters, this comes at a time when the US Federal Reserve is planning to scale back its monetary stimulus, which has put upward pressure on the dollar. Some developing countries therefore face a triple whammy of higher energy costs, a weaker currency, and domestic central bank interest rate hikes aimed at stabilising exchange rates and inflation.

South Africa has one leg in this camp as an importer of petroleum products. The rand has been on the back foot in recent weeks, and this means a big petrol price increase is on the cards for next month.

However, we are also the world’s fifth largest coal exporter (behind Australia, Indonesia, Russia and the US) and the rising export revenues limit downward pressure on the rand. Coal exports would be even higher if not for the capacity constraints on the Transnet rail corridor from the Highveld to the coal terminal at Richards Bay.

It also helps that inflation has been relatively stable in South Africa, with price increases excluding food and energy costs running at only around 3%. The SA Reserve Bank’s latest forecasts suggest that inflation should stay close to the 4.5% midpoint of the target range over the next two years. However, the risks are clearly to the upside. A gradual interest rate hiking cycle is therefore likely to commence in the next few months. How gradual will depend on where energy prices settle and how the rand responds. The Reserve Bank will also keep a close eye on what other central banks are doing, particularly the US Fed.

Oils well that ends well?

In summary, it is a delicate moment for the global economy, and could end up being a long, cold winter for people in the Northern Hemisphere. The big risks are a slowdown in consumer spending, further disruptions to production and persistent inflation that forces central banks to tighten monetary policy sooner than they’d like. None of this is good for markets.

However, it is worth repeating that the underlying cause is the strong recovery in demand as the world gradually puts the pandemic behind it. This is good. Moreover, energy prices are notoriously volatile. In April last year, a key oil futures contract briefly traded at a negative price. Traders were willing to pay to get rid of the oil rather than take delivery. The most recent price moves in gas and coal also have all the hallmarks of panic-driven trading, and therefore are unlikely to be sustained over time. Investors in diversified portfolios should similarly avoid making panicky moves in response to the recent dramatic headlines. The current situation is the result of a nasty confluence of events, and some of the contributing factors on the supply side could ease.

Finally, in the current context it might be worth remembering that 13 years or so ago, “Peak Oil” was a dominant investment narrative. It was believed that the global supply of oil would peak and this justified prices surging to $150/barrel and beyond. The opposite turned out to be the case. Today, we’ve probably already passed the point of peak oil demand due to the rise of electric vehicles. Demand for coal could prove stickier, while natural gas could increase in importance as a “bridging fuel” while the world transitions to renewable sources. However, short-term price movements are clearly going to remain unpredictable.

This is relevant when thinking about investments more broadly. Dominant narratives can lead you astray. Just because you read about a “megatrend” or “structural change”, whether it is ESG, clean energy, blockchain, biotechnology, or demographic shifts, doesn’t mean that there is easy money to be made. It could be priced on already, or simply overhyped. You could be way too soon or too late already. Maintaining appropriate diversification across different asset classes and within each asset class remains the best way of investing, even if it sounds boring.