Factor-based investing made smarter

Jason Swartz, head of portfolio solutions at Satrix.

Understanding your existing portfolio’s mix of factors and pure alpha, by Jason Swartz, head of portfolio solutions at Satrix.

Factor-based strategies (or smart beta) exploit the returns that come from harvesting specific ‘factors’ or risk premiums. Explicitly targeting these premiums can help improve the risk-return profile of a retirement fund portfolio. But exactly how to choose the right factor strategy (or combination of strategies) and the practical application of these can be a challenge for trustees.

Says Jason Swartz, head of portfolio solutions at Satrix, factor investing is enjoying growing popularity around the world. Factor investing has the ability to empower multi-managers and consultants to build client portfolios simply and efficiently.

From the transparent manner in which factor portfolios are systematically constructed, to the capability of building tailored investment outcomes with greater diversification and predictability, to the low fees, to the reliability in consistently delivering a specific investment philosophy, factor investing is beginning to revolutionise the investment industry.

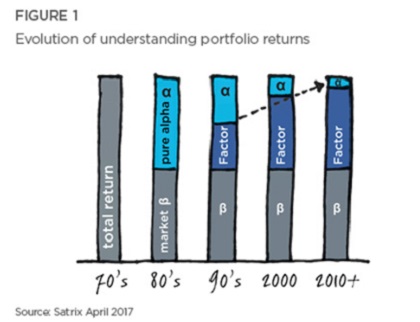

In this article we utilise a mathematical framework to assist an understanding of an active portfolio’s mix of factor exposures, as well as pure alpha. The reason this exercise is meaningful and important, is that many traditional active managers deliver a significant percentage of their active returns via static exposures to factors (see figure 1). This phenomenon has less to do with the fact that factor strategies are implemented in a passive way, but more to do with factor strategies having the same ideology as active managers with respect to exploiting market inefficiencies and aiming to outperform the market.

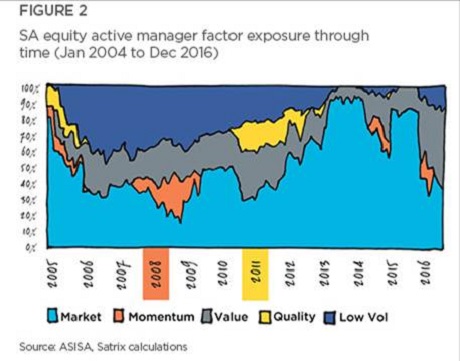

With factors constructed to have characteristics which historically explain excess returns, active managers typically embed these characteristics in their investment process through well-known strategies such as Value, Momentum, Quality, Size and Low Volatility[1]. A useful exercise, and the subject of this article’s application, is to understand which combination of these factors is needed to best replicate an active manager’s return through time (see Figure 2).

This analysis provides valuable insight into whether the active manager incurs style drift though changing exposure (intentionally or inadvertently) to the underlying factors. In our example we see active manager’s apparent drift toward Momentum during 2008 and Quality during 2011; an outcome that would be revealing to the client or asset owner with respect to whether the active manager is being consistently ‘true to label’ versus their claimed investment style.

A constructive variant of this application is performance benchmarking

Given the framework discussed above, one could decompose the expected return of a portfolio into 1) the return to a relevant benchmark, 2) the active return from the portfolio’s exposure to a mix of factors, and 3) the pure alpha, i.e. the active return above and beyond static exposures to factors. By making this distinction when attributing performance, the client is able to properly ascribe the value the active manager is adding relative to their fees charged – and since pure alpha is rare and more expensive, it is important to understand that the active manager is adding return beyond factor exposures.

For more information on this topic please feel free to contact Satrix directly. In our next part of this series, we discuss the concept of ‘portfolio completion’, which is the next logical progression to employing factor investing.