Exceptional risk-adjusted long-term returns start with careful stock selection

Following three years of strong global equity performance, a key question for investors is whether markets will continue to power ahead in 2026.

With distinctly different outcomes possible, sitting on the sidelines is not a viable option, but ideally investors need to construct portfolios that can deliver appropriate client outcomes even in challenging market environments.

At PSG Asset Management, we believe that the best investment opportunities are generally found in uncrowded areas that have been neglected by the rest of the market. These out-of-favour areas generally offer fertile hunting grounds for mispriced investment opportunities. However, to achieve long-term investment success, these mispriced assets need to possess an inherent quality that the market is overlooking. This may be due to, for example, the market having an excessive focus on short-term addressable issues; focusing on risks fully captured in the asset price; or mis-assessing the evolving supply-demand dynamics.

We firmly believe that the price paid for an asset is a key determinant of both the returns generated from that asset over time, and the risk associated with investing in that asset. Thus, our approach tilts the odds of earning exceptional risk-adjusted returns over the long term in our clients’ favour.

We pride ourselves on our independent and in-depth research, which helps us to find these opportunities wherever they may reside. Our investment decisions are driven by the attractiveness of the individual investments, not by their index weight or by a rigid strategic asset allocation framework. As a result, our portfolios can often look different to those of most of our competitors, offering our clients valuable diversification benefits as part of a blended portfolio.

Out-of-favour stocks can deliver returns that rival those of the market darlings

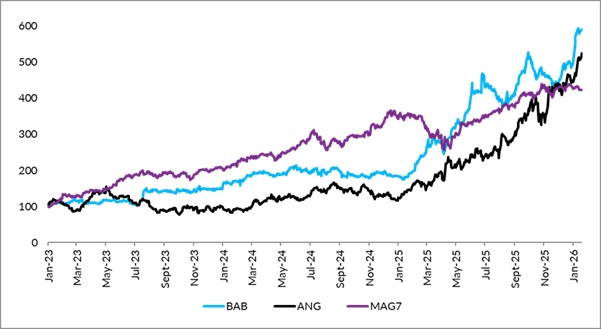

While the artificial intelligence (AI) rally has undoubtedly captured the public imagination, what is less well telegraphed is that other select stocks have delivered returns that outshine even those of the AI leaders. From January 2023 to December 2025 (a period that captures the AI frenzy), Mag7 shares delivered an incredible price return of 329%. Over the same period, Babcock International plc delivered 393%, while AngloGold Ashanti rose 347% (both in US dollars).

Babcock and AngloGold vs the Magnificent 7

Sources: Bloomberg and PSG Asset Management

In 2025, the Mag7 gained a relatively muted 23%, while we held numerous shares that increased between 100% and 355% in US dollars. Fear of missing out (FOMO) can cause investors to forget that less popular alternatives can frequently outperform market darlings. Our investment process excels at finding opportunities such as these.

|

Case study: Telkom Telkom is a classic example of our investment approach in practice. When we initiated our investment, the inherent quality was obscured by the market’s focus on historically poor management and capital allocation decisions. The business appeared to be in structural decline with the legacy copper business going backwards and the business generating low levels of free cash flow. Our research identified substantial hidden value in the form of a leading fibre asset (Openserve) and a very competitive and well-run mobile asset (Telkom Mobile) that was rapidly taking share from the large incumbents through a low-cost data-led strategy. The company had spent almost three times its market capitalisation on investing in these fibre and mobile businesses over the prior decade. However, the declining legacy copper business was obscuring the value of the growing businesses. We initiated an investment, buying at share prices in the R25 to R30 per share range in 2023 and 2024. After about a year, the first signs of inflection became visible as the growth from the new businesses started to more than offset the drag of the legacy assets (which were declining in the revenue mix). The market was positively surprised by the return to growth, higher margins and dramatically improved free cash flow, resulting in a material rerating of the share to its current level of over R60 per share. |

|

Case study: Platinum producers: Gold and resources were the story of 2025, with gold rallying 64.5% and platinum 127%. We have written extensively about our investment theses on these sectors (including their role within differentiated portfolios) since we moved to meaningful exposures in 2023/24. Platinum group metal (PGM) prices were depressed for a number of years, primarily due to an expected decline in demand, which was based on significant electric vehicle adoption forecasts (that we viewed as optimistic). South Africa supplies 70% - 80% of the world’s platinum, and the supply side of this industry is highly forecastable due to high depletion rates, known capex and long timeframes between investments and production. When future supply is expected to be below conservative future demand estimates, the outlook for prices is excellent but timing is unclear, and patience and a longer-term perspective are required. In periods of strong underlying commodity price performance, platinum mining companies provide geared exposure to the PGM basket price. |

Look beyond the obvious areas to secure future returns

After several years of excellent stock market returns, investors have valid concerns whether current trends can continue, especially given high valuations for the popular AI-focused stocks, high levels of index concentration, and a challenging geopolitical situation. In such an environment, investors would do well to consider investments outside the popular winners of the recent past, diversifying their portfolios into investment positions that can perform in many different market environments.