Emerging Markets Remain Resilient in April

Three Things We Are Thinking About Today

1. Although environmental, social and governance (ESG) best practices in China have been improving, China generally lags developed markets in this area. Chinese companies operate according to local norms and requirements from local regulators, but we have found many are doing more than what is required in many areas. As regulation in China evolves, many companies will likely progress in becoming more accountable for the wider stakeholder. Many companies already have very robust reporting, where investors can see exactly how sustainability fits in their overall strategy, and how the company and management teams take account of ESG risks. While China’s capital market has opened and the barriers are coming down for international investors, Chinese regulators are set to improve ESG reporting processes further through mandatory disclosures for listed companies by the end of 2021. We believe these steps will pave the way for Chinese companies to truly be in line with their Western counterparts.

2. A second wave of COVID-19 infections in India led to the implementation of new restrictions including lockdowns (at a regional state level rather than nationwide) to contain the outbreak. While this second wave is expected to impact the country’s economic recovery in the short term, we expect the economy to bounce back as the government accelerates its vaccine rollout and lockdowns are lifted. In the interim, however, the situation remains fluid and we continue to monitor the developments. In the longer-term, we expect India’s economic recovery to continue as economic activity gradually improves. We see corporate earnings on an uptrend toward earnings normalization, following the pandemic-related downturn. The overarching drivers underpinning the Indian market also include low interest rates, high liquidity, and fiscal incentives, all of which currently remain intact. However, we are mindful of the risks, including the ongoing virus pandemic, regional and global geopolitical relations and the path of the recovery and infection rates in other regions globally.

3. The COVID-19 pandemic has accelerated the evolution of globally leading emerging market (EM) companies. Taiwanese and South Korean semiconductor firms dominate the global industry with their strong manufacturing capabilities, allowing them to ramp up investments and widen their competitive advantages amid booming demand for chips from high-performance computing, automobile, and other businesses. South Korean companies have also spearheaded the development of electric vehicle batteries, which have achieved greater penetration worldwide on the back of policy support and technology advancements. In China, biotechnology firms are developing innovative treatments for cancer and other major diseases and have won the confidence of global pharmaceutical groups in licensing these new drugs. India’s internet space also offers huge potential, in our view. Taken together, evidence of EM companies scaling the value chain has increased, and we see durable growth characteristics in many of these firms. We expect a rising number of high-quality companies to emerge as various industries continue to develop and consolidate, leading to attractive investment opportunities for EM investors.

Outlook

It has been more than a year since the initial outbreak of COVID-19, but the global pandemic continues to challenge economies and their health care systems. While new variants of the virus have spread just as countries start to roll out vaccines, we believe EMs will likely show continued resilience in the face of new challenges. Prior to the pandemic, EM fundamentals appeared generally attractive, and we still believe that to be the case.

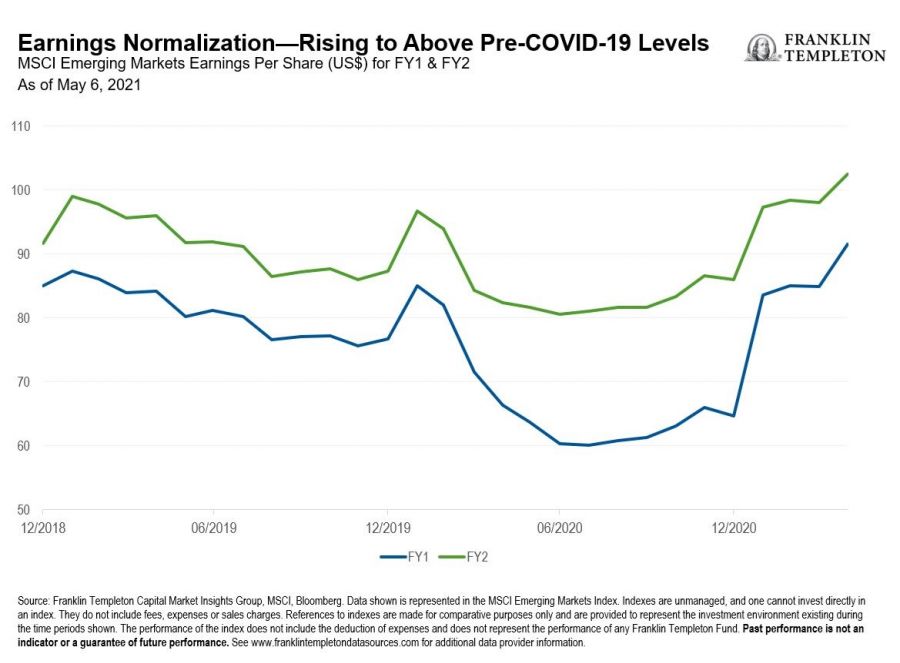

While recovery in economic growth could remain muted this year in many markets, we expect more normalization in 2022. Stress in EM banking systems has been manageable, despite the loan moratoriums and government support policies for borrowers in many EM countries.

Consumerism among the EM population is also a well-told story, but it remains a multi-year growth opportunity. We think there could be new opportunities across a wide range of goods and services in the wake of the pandemic and still see a continued trend of premiumization, where consumers with higher disposable incomes desire higher-quality goods.

Ongoing technological transformation and innovation in EMs, which accelerated as a result of COVID-19, have translated into higher free cash flow generation, relative to developed markets (DMs). This cash flow has helped deleverage balance sheets, but also found its way back to investors through dividends and share buybacks and encouraged companies to adopt improved governance standards and better capital discipline. In our view, this all adds up to a higher-quality earnings story.

Emerging Markets Key Trends and Developments

EM equities rebounded in April but trailed their DM counterparts. Easing US Treasury yields, and a weaker US dollar supported demand for EM stocks, although worsening COVID-19 outbreaks in certain EMs capped the asset class’ advance. In contrast, market optimism centred on the United States and its massive stimulus packages, dovish monetary policy, rapid vaccination progress and strong economic recovery. The MSCI Emerging Markets Index rose 2.5% over the month, while the MSCI World Index returned 4.7%, both in US dollars.1

The Most Important Moves in Emerging Markets in April 2021

Emerging Asian equities rose in April. Among the top regional markets were Taiwan, South Korea, and China, all three of which posted robust first-quarter economic growth. Strong exports from Taiwan and South Korea plus improving consumption in China were bright spots. Conversely, markets in Thailand and India were some of the weakest performers. Both countries tightened COVID-19 restrictions as daily new infections reached new highs, undercutting the outlook for their economies.

Latin American markets recorded diverse performances in April, with Argentina and Brazil among the top performing EM markets, with Chile, Colombia, and Peru among the weakest. Appreciation in the Brazilian real and strength in global markets drove equity prices in Brazil, as investors overlooked COVID-19 and fiscal risks. Political uncertainty and mobility restrictions, however, weighed on market sentiment in Chile, Colombia, and Peru. Although Mexico lagged its regional peers, the equity market ended the month with positive returns, supported by a US-led recovery in manufacturing and exports.

Markets across Europe, Middle East and Africa rose in April, driven by gains in Eastern Europe and the Middle East. An acceleration in vaccine rollouts in Europe and a subsiding COVID-19 wave boosted confidence in Poland, Greece, and the Czech Republic. At the other end of the spectrum, the Russian and South African markets essentially ended the month flat. US sanctions and an increase in interest rates aimed at curbing inflationary pressures hindered returns in Russia, while political uncertainty and a slow inoculation pace held back equity prices in South Africa.