Defence stocks provide diversification opportunities in a war-prone world

Writing about peace and war can be a delicate subject. While the last couple of decades have been relatively peaceful across most of the developed world, many developing countries have not enjoyed a similar era of calm.

Especially hard hit has been the Middle East and Africa, which have both experienced constant bouts of conflict over a prolonged period.

Today, much of the developed world faces the prospect of war again. As grim as this prospect is, and as much as military and defence investments are traditionally viewed poorly from an ESG perspective, they remain relevant and necessary.

Developments in recent years have cast a new light on investments in military and defence stocks, increasing the growth potential of traditional arms manufacturers, like tank and munition producers, and companies that provide auxiliary services, such as radar and electronic systems.

Risks of regional hostilities spreading into a broader conflict

A little over two years ago, war returned to continental Europe as nearly 200 000 Russian soldiers crossed the border from Russia and neighbouring Belarus into Ukraine. They thought it would be a swift march to victory in Kyiv, but the battle still drags on, and hope of a resolution is distant.

While the battle for Ukraine is by far the most dangerous in terms of the risk of it spilling over into a much larger conflict, it is by no means an isolated incident. According to the Geneva Academy of International Law and Human Rights, there are currently more than 100 instances of armed conflict worldwide. This includes both internal and cross-border conflicts.

Aside from actual conflicts, there are also several situations where tensions are simmering below the surface. Front and centre would be Beijing and its increasingly aggressive rhetoric towards Taiwan and its disputed claims over the South China Sea.

While most of these conflicts are unlikely to spill over into large-scale warfare, there is no looking past the fact that today, the world is again facing the prospect of a confrontation between nuclear-armed superpowers, with Vladimir Putin warning that its nuclear forces are in “full readiness” a few weeks ago.

Structural Underinvestment

Since the end of the Cold War, the West experienced an era referred to as the “Long Peace” or “New Peace”. This might have instilled a false sense of security in many countries, swiftly exposed when regional powers had to start delivering aid to Ukraine. The thought of a large-scale ground war had become so distant that many members of NATO realized they were not well equipped to fight one.

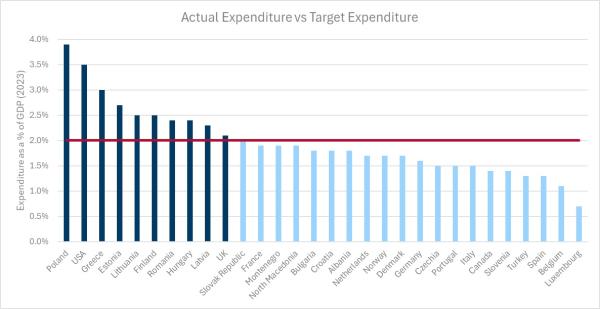

To ensure that it is sufficiently armed to defend members when required, NATO put spending guidelines in place nearly two decades ago. This guideline is 2% of each country’s respective GDP. The rationale makes sense. Countries with stronger economies would contribute a larger nominal amount, but the contributions would be fair proportionally. The problem with this guideline is that it was not being met – not even close – to gear up for a far riskier geopolitical landscape. In 2014, only three NATO members met the contribution requirement, despite NATO Defense Ministers pledging bigger contributions as far back as 2006.

2014 proved to be a pivotal year in NATO’s history, as the “Long Peace” came to an abrupt halt when Russia illegally annexed the Crimean Peninsula. Understandably, this served as a wake-up call. Two years later, there was another equally unexpected wake-up call. His name was Donald Trump.

Increased Defense Spend

The results of Russia’s invasion and Trump’s hardline stance have been noteworthy. While only three NATO members reached the target spend level in 2014, this increased six-fold to an expected 18 countries in 2024.

While this is a massive improvement, a lot of work (and investment) still needs to be done. After the ascension of Finland in 2023 and Sweden in 2024 to fully fledged members of NATO, the organization now has 32 member states, more than 40% of whom will not have met their spending targets yet.

Source: NATO

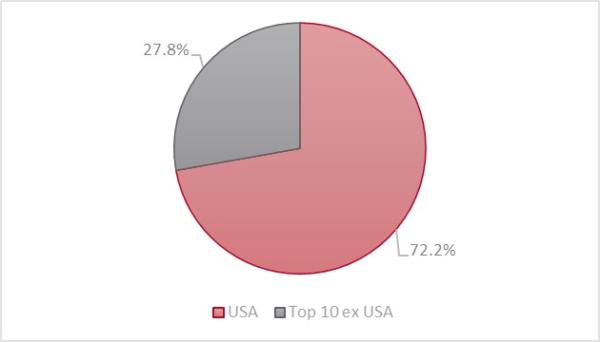

And while the above chart gives the impression that the US is not that far ahead of peers in terms of military expenditure, it comprises 72.2% of military spend compared with the spend of the top 10 countries excluding the US.

Investment Implications

As grim as the prospect of war is, and as much as military and defence investments are traditionally viewed in a poor light from an ESG perspective, they remain relevant and necessary. Developments in recent years have cast a new light on investments in military and defence stocks. So much so that some ESG investors have even started viewing defence stocks more favourably, choosing not to exclude them based on ESG sentiment alone anymore, as they do play a role in protecting the S – the very fabric of society.

Exposure to the structural growth story behind this theme can come in several different forms. One can either invest in traditional arms manufacturers or take a more subtle approach by investing in companies that provide auxiliary services, such as radar and electronic systems. Lastly, there is also the option to invest in companies that have segmental exposure to the industry without being dependent on it.

Examples of the more traditional arms manufacturers would be German manufacturer Rheinmetall and British-based BAE Systems. Both manufacture traditional warfare weapons like tanks and munitions. Investors can consider German-based Hensoldt or French-based Thales in the auxiliary services segment. Both provide “senses” to military platforms like tanks, helicopters, aeroplanes, and other fighting vehicles. They specialize in optics systems, radars, and other surveillance equipment.

Lastly, investors can also consider companies like Airbus or Rolls Royce. Both are familiar names in the commercial aerospace industry but have significant defence segments. All these companies have seen and should continue to see, an increase in military spending, supported by a world with simmering geopolitical tensions.

Last year, global equities delivered stellar returns, and equities have continued to provide some blockbuster returns so far this year. Once markets inevitably cool down and the effect of a prolonged period of high borrowing costs starts to bite, investors will have to look outside of the well-trodden IT sector for good returns. That job certainly becomes easier when you look for investment opportunities outside South Africa that are set to benefit from structural tailwinds, even in times of geopolitical tensions and uncertainty.