Credit Chronicle: A welcome rally but beware over enthusiasm

A strong quarter means high-yield markets are now pricing a fairly benign economic outlook, but with a more testing environment ahead, current valuations warrant a closer look.

Despite the rise in many developed market sovereign yields, credit markets performed well during the second quarter. In the high-yield (HY) market, spreads tightened in both the US and Europe, helping to drive positive total returns. By quarter end, high-yield credit spreads were approaching their tightest levels in 18-months. But with clouds looming on the macro horizon, investors should reassess high-yield valuations in the context of rising default risks.

Darpan Harar, Multi Asset Credit Portfolio Manager, Ninety One: “Following the recent rally, a common question we are asked is whether high-yield credit investors are still being compensated fairly for default risk as companies face a more testing operating environment.”

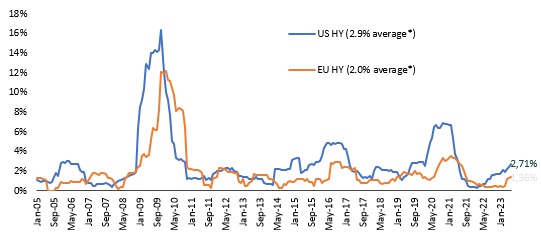

After dropping to historically low levels amid significant COVID-related stimulus, default rates are still below their long-term averages, but they are increasing to more ‘normal’ levels, as shown in the figure below. While traditional cyclical peaks see default rates in the range of 10-12%, the key question is how high are they likely to rise in this cycle, and what’s being priced into the market?

Figure 1. Rolling 12-month high-yield default rate

Source: JP Morgan. *Average of monthly data. January 2005 to June 2023.

Harar explains: “To inform their default expectations, credit market participants typically look at a mix of bottom-up and top-down indicators. Focusing on these most commonly followed data points, we see mixed signals.“

On one hand, distress ratios remain fairly low, painting a relatively benign picture; considering the proportion of the US high-yield index trading above a spread of 1000, the current level of distress suggests that the market currently sees relatively few clear default candidates. In contrast, one of the more reliable leading indicators paints a bleaker picture. Trends in bank lending standards have historically proven dependable bellwethers for default rates. Key among these, survey results from the Federal Reserve’s Senior Loan Officer Opinion Survey on Bank Lending Practices have tended to provide useful information on the direction and magnitude of corporate defaults over subsequent quarters; this indicator now points to a rise in defaults in coming months.

Harar notes: “While the exact path of defaults will depend on how various regional macroeconomic scenarios play out, default rates look set to return to at least long-term averages in the near term, and given the magnitude of the macroeconomic forces at play, we think it is likely they continue to rise above those averages.”

However, given a starting point of comparative corporate balance sheet health, default rates may not hit traditional cyclical peaks, even in the event of a recession and full default cycle. But a rise from current levels seems inevitable. What, then, of current valuations? Following a strong spread rally, are investors still being compensated well enough for default risks?

An analysis of what default assumptions are baked into current spread levels leads one to conclude that current valuations leave little margin for error. For US high yield, the implied default rate is 1.8%, below the long-run average of around 2.9% and below JP Morgan’s latest trailing 12-month estimate of 2.7% (including distressed exchanges). For Euro high yield, the implied default rate is 2.4%, slightly above the long run average of around 2%. While this analysis is only indicative and sensitive to assumptions (in particular, that the additional compensation investors currently demand over expected credit losses is in line with historical averages), it is clear both markets are trading to a relatively benign default outlook.

Harar concludes: The speed and scale of monetary policy tightening means negative surprises are likely. And while we think it is unlikely that cyclical peak default rates will be reached over the coming year, our analysis suggests that a reversion of default rates into even the mid-single digits (5-6%) would indicate spreads widening back to somewhere around 600bps. This supports a bias towards higher quality credits at current valuations.

To read the Credit Chronicle in full, click here.