Could global growth this year be the fastest this century?

Global asset manager Schroders substantially upgrades its growth forecasts for 2021.

The world economy is set for its fastest year of growth in the 21st century this year, according to our latest forecasts. Schroders economists now think global GDP is set to expand by 5.9% in 2021, having upgraded our previous forecast of 5.3%.

As lockdowns ease, the service sector - which includes businesses such as restaurants and hotels - is driving the recovery in economic growth. Developed economies are at the forefront of recovery compared to emerging markets, thanks to the greater availability of vaccines and government support.

What about inflation?

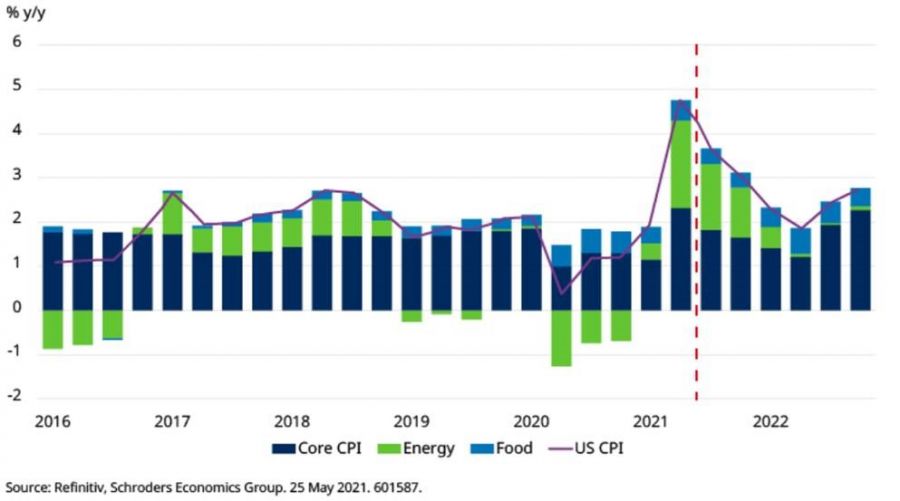

2021 is also set for an increase in inflation, with global CPI (Consumer Price Index) expected to be running at 2.9% this year, an increase from our previous forecast of 2.6%.

This is largely due to the rise in commodity prices and the rapid pace of recovery which has created shortages of key goods such as computer chips.

Why the increase in inflation may only be temporary

However, Schroders believe that the current inflation spike will be temporary.

The US headline CPI hit 4.2% year-on-year in April, its highest since 2008, but should fall back. Schroders believe the demand that comes with recovery can be absorbed by the economy without causing another round of price increases as a result of higher wages.

Inflation tends to decline during economic recoveries as businesses get back to work. Productivity strengthens, allowing companies to keep prices competitive and containing any spike in inflation.

What about further down the line in 2022 and 2023?

Inflation could rise again further down the line following the full reopening of the service sector and an increase in people returning to work. According to Schroders projections, headline inflation will creep back towards 3% in the next two to three years.

Inflation could continue to rise in 2023 and beyond unless action is taken to cool increasing demand following the recovery from the pandemic. This means that central banks will need to consider a firmer policy stance.

US inflation – breakdown and forecast

More decisive action may have to be taken

The US Federal Reserve (Fed) is focussed on a wide range of targets, particularly employment. However, the risk is that other aims such as stable inflation and financial stability get ignored.

The Fed will need to act to make sure the pick-up in inflation at the end of 2022 does not get out of hand.

In their new forecast, Schroders now see the Fed beginning to take pre-emptive action by reducing the pace of asset purchases in Q4 this year (previously they thought this would happen in Q2 2022). On interest rates, the Fed may be able to stay on the side-lines for now, but will be forced into action next year. Schroders forecast a rate rise at the end of 2022 (previously 2023).

Globally, the pressure on capacity caused by the increase in demand is less than in the US because of deeper downturns and slower recoveries. However, other economies are not far behind and investors will be asking the same questions of policymakers in the UK and eurozone.

What else could affect growth and inflation?

The above refers to Schroders baseline forecast, but there are other scenarios that could play out. They have added two new scenarios where inflation is higher than the baseline: “boom and bust” and “supply side inflation”.

“Boom and bust” captures the risk of a stronger-than-expected recovery in growth as demand is unleashed following the success of the vaccine. Economic support is tightened and interest rates are raised resulting in a bust, curbing both growth and inflation.

“Supply side inflation” is where supply struggles to keep up with the rise in demand. People are slow to return to work resulting in a greater acceleration in wages and supply shortages. This would mean persistent high inflation, causing interest rates to be raised.

On a more optimistic note Schroders introduce a “creative destruction” scenario. This is where there is a permanent increase in the adoption of technology by businesses resulting in greater efficiency. Growth increases with higher productivity, which keeps inflation contained.

We have kept our “vaccines fail” scenario, where a high degree of normalisation this year allows the service sector to return and drive recovery. However, the recovery path is vulnerable to the emergence of new variants and greater consumer caution.