Consumer staples: Should they be portfolio staples?

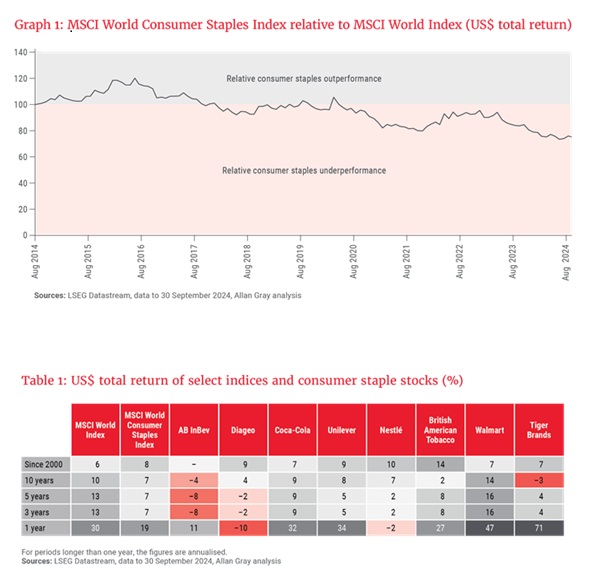

As the adage goes, a good business is not necessarily a good investment. The global consumer staples sector has underperformed the market, represented by the MSCI World Index, over 10 years, as shown in Graph 1. In fact, the performance of many consumer staple stocks has been disappointing over most time periods since the turn of the millennium (see Table 1). Are these companies fundamentally broken, or are there opportunities for contrarian investors?

Characteristics of consumer staple businesses

Investors typically seek out consumer staple stocks because they are considered to be defensive. Some of the important characteristics that underpin this belief are:

• Demand stability: Consumers buy staple products in good times and in bad, meaning that these businesses are less exposed to cyclical changes in demand. This demand inelasticity usually also applies when prices rise in a predictable way. Stable volumes and pricing translate into steady topline growth.

• Brand equity: Consumer staple businesses are not only home to many of the global megabrands, but also many much-loved local brands. Most consumers have some affinity for these brands, and purchasing decisions for these products are made almost subconsciously. Healthy brands create high barriers to switching.

• Pricing power: Strong brands and customer loyalty create pricing power. Good consumer staple businesses nurture their brands by consistently reinvesting in them. This drives sustainable profitability as healthy brands are more robust against changing economic and/or industry conditions.

• Scale: These businesses have mastered the art of managing large and complex manufacturing and distribution networks across the globe. Scale creates significant bargaining power with their suppliers, enabling them to manage product costs effectively and dominate shelf space in our favourite retail outlets.

Stable volumes and pricing translate into steady topline growth.

Relative to the average business, defensive businesses have more consistent earnings streams, which enable them to consistently reward shareholders with dividends. Not only that, but defensive businesses can also support higher debt loads through business cycles. This creates significant option value during difficult economic times.

Of course, all industries face risks and, for consumer staples, some of the noteworthy risks include:

• Absolute price levels: It is important to distinguish between inflation (i.e. the percentage change in price level) and affordability (i.e. the absolute price level). Balancing pricing power and affordability is especially important for those with outsized exposure to mass-market/commodity brands.

• Emerging competition: The fight for consumer attention and share of basket has intensified with the pervasiveness of technology. Private-label brands and smaller, local brands can reach consumers faster and more affordably than in the print-and-television-only era. Dynamic competitive environments may be good for consumers, but brands must have their fingers on the pulse to remain dominant.

• Changing habits: Consumption habits are changing, and this also impacts how brands should be engaging with consumers. Weight-loss drugs, for example, are becoming increasingly popular and are likely to impact products like packaged foods and sugary drinks.

• Complexity: Any business that has exposure to various categories, geographies, currencies and regulations is difficult to manage. A strong culture and attitude towards governance are important considerations.

Shelter from the storm

Consumer staples have historically provided investors with shelter during economic storms. Graph 2, a historical expansion of Graph 1, displays the significant and often-rapid outperformance of consumer staples during periods of significant economic stress.

Click here to read more...