Considering the impact of rising regulatory risk in China

All businesses operate under a regulatory regime, in many cases involving multiple regulators and great complexity. While this makes regulatory risk important for investors, the impact of very adverse regulatory changes is often hard to anticipate. This is because they are often ‘tail events’, with a low probability of happening. However, should they occur, the impact can be severe.

Once regulatory risk is public, markets can try to price it in. For example, Glencore has several ongoing investigations by regulators into their trading business, and is valued at a significant discount to peers as a result. We can look at historic fines levied for similar cases and then adjust our estimate of intrinsic value for a conservatively estimated (i.e. large) payment.

Regulatory changes and actions can derail an investment thesis

The regulatory risks that hurt are those that were not considered by the broader investment community, and which have not been priced in by markets as a result. This risk is elevated where those with vested interests often have the loudest voice, and the views of those offering a differentiated perspective or more cautionary outlook are overlooked.

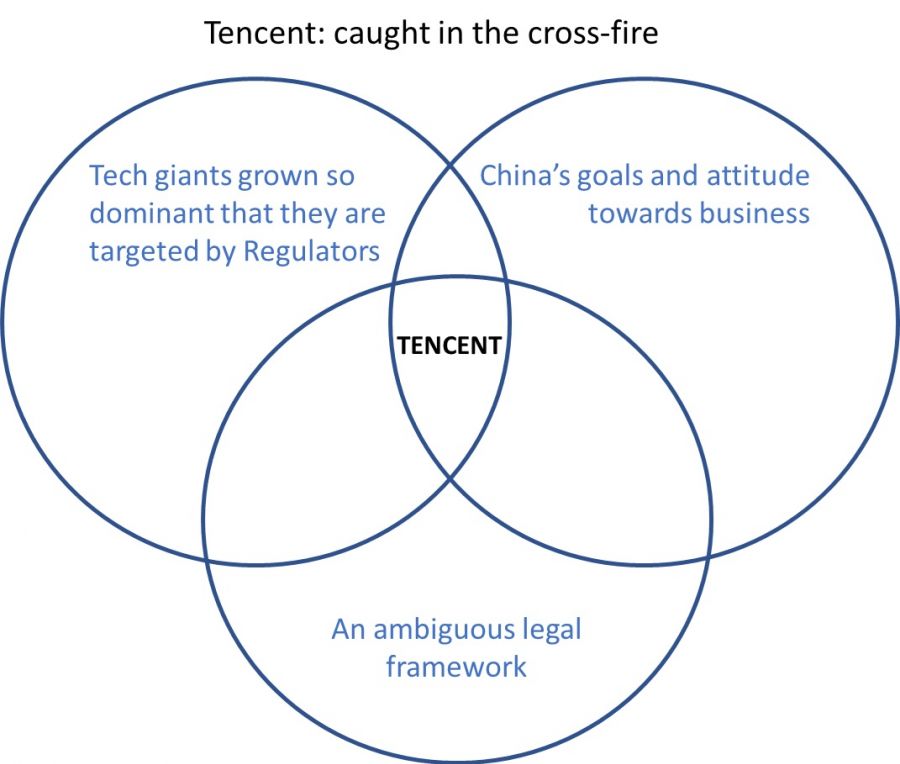

Regulatory risks are higher in some sectors and emerging markets

The large US technology companies (FANGS) have a myriad of regulatory actions pending, and must now be regarded as carrying elevated risks. Similarly, a characteristic of many emerging markets is high regulatory uncertainty, and China is no exception. However, so far the view has been that to attract the capital it needs for growth, China will be pragmatic when dealing with large businesses, offsetting these risks.

Recent actions by the Chinese authorities seem to contradict this view. These include preventing the listing of Ant Financial, launching an investigation into ride-hailing group DiDi Global soon after its listing in New York - as well as requiring it to delete its apps from Chinese app stores - and severely constraining the private education tutoring sector, causing massive declines in market capitalisation.

For example, there are three US-listed China education stocks. Gaotu Techedu’s value has dropped from $26bn in February to $800m; and TAL Education and New Oriental Education now have market caps of less than $4bn, having peaked this year at $46bn and $32bn respectively. Most commentators tend to focus on the specific sector or company impacted, but this overlooks the broad message: China’s willingness to prioritise societal and social goals ahead of the interest of private businesses.

Stewart Paterson, author of the Capital Dialectics publication, has some 30 years’ experience in capital markets, 18 of which are in Asia. Last November he made some crucial points about investing in China. These include that the Communist Party of China remains central to all things societal, economic and political, and that discussion about the pros and cons of investing in China tend to ignore this role of the Party. He argues that this can lead investors to ignore the rising jurisdictional risks that are best crystalised by asking three questions:

· What will investors be allowed to do? (Regulatory risk)

· What ought they to do? (Reputational Risk & ESG)

· Who or what could impact the profitability of what investors will actually do? (geopolitical and economic risk)

A second aspect that is often overlooked, is that investors may not always receive of level of corporate governance they expect. The US-China Economic and Security Review Commission report to Congress published in November 2019 highlighted a number of concerns with investing in the securities of Chinese companies. Their recommendations included prohibiting Chinese companies issuing securities on US exchanges if:

· The Public Company Accounting Oversight Board is denied timely access to audit work papers relating to Chinese operations.

· Company disclosure practices are not consistent with best practices on US and European exchanges.

· The Company uses a Variable Interest Entity (VIE) structure.

· The Company does not comply with regulation fair disclosure.

There are risks to how investment in many Chinese firms is structured

Many investors are not aware that foreign ownership of Chinese firms is restricted, or that shell companies and VIEs have been used to circumvent these restrictions and facilitate foreign investment. Chair of the US Securities and Exchange Commission (SEC), Gary Gensler, issued a statement on July 30 in which he says that “I worry that average investors may not realise that they hold stock in a shell company rather than a Chinese operating company.”

Bringing it home: Chinese regulation and Tencent

Assessing these risks for Tencent is crucial for South African investors given the massive weighting of Naspers and Prosus on the JSE and the benchmark-hugging investment style many managers favour.

The average South African investor may not realise that the Naspers/Prosus group is in a similar position, not owning the key Tencent operating companies. Tencent has, until recently avoided the limelight. Founder and Chief Executive Ma Hutong is a delegate of the National Peoples’ Congress of the Chinese Communist Party, and in contrast to former Alibaba CEO Jack Ma, has appeared to avoid publicity or voicing strong opinions. The consensus was that Tencent would keep out of trouble. However, it is no longer clear that this is the case.

· In late July, Tencent announced it would halt new registrations on messaging ecosystem WeChat while their security was improved to “align with all relevant laws and regulations”.

· Early in August state news agency-run “Economic Information Daily” published an article decrying the “spiritual opium” and “electronic drugs” of online games that fuel widespread internet addiction amongst China’s youth, with children playing Tencent’s blockbuster “Honour of Kings” for up to eight hours a day. Online gaming is over 30% of Tencent’s revenues.

Have South African investors adequately priced in the risk?

While the Bloomberg consensus earnings forecast has Tencent on a forward PE of 25x, careful consideration of the impact of regulatory censures on future earnings power is necessary before concluding on an appropriate valuation. The regulatory risk for Tencent, and hence Naspers and Prosus, must be a significant consideration when evaluating the investment case – and it may be one that many investors are currently overlooking.