Concerns About Europe Can Hide Credit Fundamentals of Individual Countries

10 October 2013 | Investments | General | David Zahn, Franklin Templeton

Given that the eurozone finally returned to slightly positive growth in the second quarter of 2013, and that the chances of a breakup of the single currency bloc seem to have faded, it would be tempting to conclude that sentiment about the outlook for the eurozone had also changed. And yet concerns about economic conditions in Europe remain widespread, with few observers believing that the resumption of growth over a single quarter heralds the start of a full recovery. Though several countries outside of the currency bloc emerged from recession earlier, often (as in the case of the UK) their economies have stayed weak, underlining the slowdown that has affected the entire region. Indeed, the International Monetary Fund (IMF) sees economic activity in the eurozone shrinking 0.2% in 2013 as a whole, before recovering to 0.8% growth in 2014. Many observers believe that the more troubled economies—such as Spain, Italy and, to a certain extent, France—will continue to hold back the euro bloc.

But the prevalence of this view tends to obscure the actual and potential discrepancies in growth between European countries. At its most extreme, such variation saw Germany grow by 3% in 2011, while Greece contracted by 7.2% in the same year. The latest forecasts from the IMF do predict that economies in France, Italy and Spain will more or less flatline for some time; however, often overlooked is that from Germany eastwards, the picture generally looks brighter (see Chart 1).

Chart 1: Unbalanced European Growth

IMF 2013 GDP Growth Forecasts

Source: © 2013 International Monetary Fund (IMF), World Economic Outlook as at April 2013. There is no assurance any forecast will be realised.

Widespread doubts also remain over the structural adjustments necessary in many of the eurozone countries and in the institutions that oversee the single currency bloc and the European Union (EU). The magnitude of the required changes lends itself to pessimism, with progress frequently described as "paralysed” or "glacial,” and the imbalances in and between eurozone members—in current account balances, debt levels and labour markets—which built up over a decade or longer, still only at an early stage of being corrected. There are no "quick-fix” solutions in what will inevitably be a multiyear adjustment process, and periodic pressure from financial markets is probably unavoidable. Nevertheless, such negative sentiment can mask the steady, if unspectacular, stepsmade in implementing reforms.

An IMF working paper published at the start of 2013 that examined the macroeconomic impact of structural reforms in Italy, found that important steps were underway across a wide range of key sectors, designed to address the country’s problems of limited competition, labour market rigidities and weak public services.1 Examples included not only changes to employment laws to encourage employers to hire new full-time workers, partly by lowering the cost of firing existing employees, but also less heralded measures such as tackling Italy‘s energy prices, among the highest in Europe, by opening up the sector to greater competition and facilitating investment in infrastructure. Given that liberalising economic activity and enhancing competition are the main objectives of such reforms, their likely impact on GDP (gross domestic product) and productivity in countries where they are successfully implemented could be significant.

Fixed income investors need to bear in mind these two broadly contrarian perspectives on the prevailing negative consensus, given that the pace of change in the eurozone may remain sluggish, helping to sustain concerns. We believe current policies in Europe emphasising austerity could continue, albeit at a slower pace, to keep budget deficits under control; growth in Europe as a whole will most likely be slow, though not that far below potential, given the constraining effects of high debt levels across much of the region; and continued rebalancing is likely within the eurozone.

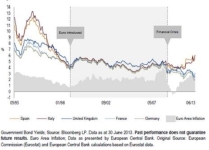

When considering investment allocations in Europe, the risks of assuming uniformity in the prospects for growth and structural reforms in the region are underlined by the past performance of sovereign bond returns. Historically, dispersion within Europe has been high, even in the years following the euro’s introduction, when for a while risk premiums seemed almost to vanish, leaving Greek 10-year government debt trading only 7 basis points higher than similar German Bunds at one time. Significantly, in the dozen largest European sovereign bond markets, double-digit ranges between the best and worst performers were the norm from 2003 to 2012, with several years seeing dispersion greater than 20% (see Chart 2 and Table 1 below).

Chart 2: Country Selection Is Vital in the Search for Real Yield

10-Year Government Bond Yields May 1993 to June 2013

Table 1: Europe Is Not a Homogenous Region

Calendar Year Sovereign Bond Performance (2003–2012)

© 2013 FactSet Research Systems Inc. All Rights Reserved. The information contained herein: (1) is proprietary to FactSet Research Systems Inc. and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither FactSet Research Systems Inc. nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Sovereign bond performance

Two conclusions can be drawn from this wide variation in returns. First, an active approach to managing country allocations within European sovereign bond markets appears crucial to improving return potential. The second is that, regardless of how the fundamentals of the eurozone, the EU or Europe are presented, investors should avoid viewing these units as homogenous or a combination of groupings (for example, core and periphery), and instead focus on pinpointing the individual countries whose debt potentially offers the most attractive risk/return profiles.

Assessing each country’s credit fundamentals over the medium term is a key part of our approach to evaluating relative spreads between European sovereign bond markets. For example, we believe the case for Italian sovereign debt remains broadly positive for a number of reasons. Our initial investment view was taken as the deepening of the eurozone crisis from late 2011 onwards underlined to the region’s policymakers how difficult it would be for the monetary union to function without Italy. This deterioration of the crisis seemed to us to increase the chances that eurozone policies would be oriented towards helping Italy to service its debt obligations. With the appointment of the Monti technocrat government, the prospects for meaningful fiscal consolidation and structural reform looked encouraging, and though subsequent progress has been halting, our view about the potentially positive spin-offs for debt reduction and economic growth is still broadly upbeat. In addition, while much attention has focused on the indebtedness of the Italian public sector, far less has been paid to levels of borrowing among Italian households, which remain among the lowest in the euro area.

Of course, Italian sovereign yields have come down a long way, with 10-year bonds falling from over 7% at the start of 2012 to trade in a range between 4% and 5% so far in 2013. Although much of that decline can be attributed to the reduced stresses in the eurozone, we believe that Italian yields have continued to offer attractive value potential, particularly when compared to the returns on offer from German Bunds. In our view, Bunds still contain a perceived "safe-haven” premium that is not merited, despite the significant narrowing of spreads between Italian and German sovereign bonds that has occurred since the start of 2012.

More broadly, we would urge investors to focus on the growth and debt metrics of individual European countries, rather than fall into the habit (or trap, as we would argue) of viewing Europe through a prism of pessimism. We believe the volatility in European markets seen during the eurozone crisis has sometimes caused sovereign yields to become detached from underlying credit fundamentals, presenting plenty of attractive investment opportunities. It seems likely that periods of such volatility could reoccur, as European policymakers attempt to balance progress on reforms, austerity and a return to growth. In our view, investors would do well to develop their views of countries’ distinct credit fundamentals, and how they compare, to prepare for such eventualities.