Clients can invest up to 100% of their investment assets offshore, but should they?

Hymne Landman

Many living annuity providers across South Africa can no longer offer investors unlimited offshore exposure when they retire. This is because investment companies may have reached their offshore investment limit.

Investment companies may not invest more than 45% of their total assets under management offshore. Once they have reached that limit, which many have, they cannot allow their existing clients to increase the offshore exposure in their investment portfolios for them to stay within the 45% offshore allocation limit overall. For the same reason, new clients may only be allowed to invest up to a maximum in offshore assets for their investment portfolios. These offshore investment restrictions do not only apply to living annuities, but also to other products (like endowments and tax-free savings investments).

Momentum Wealth will not have to impose maximum offshore limits for new investment portfolios or restrict our living annuity clients’ offshore exposure in the foreseeable future. This is based on Momentum Metropolitan Holdings’ balance sheet asset allocation and our experience and expectations of new investments’ investing in offshore assets.

Even though living annuity clients can invest all their assets offshore, the question is: “Should they?”

For some investors it is a resounding “Yes”. These investors typically have expenses based in foreign currency. Their capital and investment return must protect the rand purchase power of their income. They use their living annuity income to pay for foreign currency and foreign currency-based expenses, like maintenance of property outside South Africa, or lifestyle choices that include travel or spending on imported products.

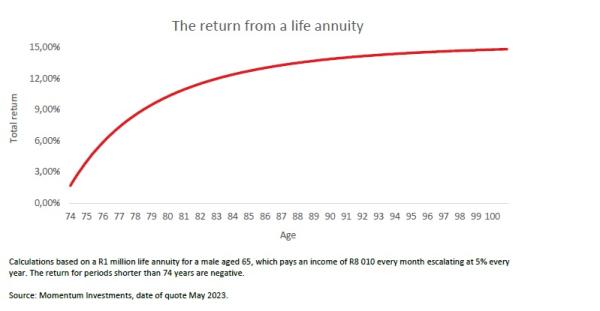

For the rest, the decision of how much to invest offshore is not as clear-cut. In these cases, investors must ask themselves “Why do I want to invest that much offshore?”. Do they believe that offshore asset classes will consistently outperform the local market, either due to the weakening of the South African rand or due to limited local investment options that won’t be able to provide them with the required investment return. If it is the case, the Momentum Retirement Income Option is the investment product solution you must consider. It offers you and your clients the option of using a rand return-guarantee for part of the living annuity’s investment portfolio. Our Guaranteed Annuity Portfolio (GAP) offers a guaranteed rand-return in your investment portfolio for as long as your client lives. It can deliver a total return of more than 14% a year as your client lives longer (see graph).

The GAP is an option for selection as part of your client’s living annuity investment portfolio. It offers the same features as a traditional life annuity in that it guarantees a rand income for your client’s life.

For clients that live longer, the like-for-like total return that they would need from another asset to match our GAP’s guaranteed income stream can be calculated by looking at the present value of all expected income returns from the GAP for expected age reached. The total return profile looks as follows:

The income return of the GAP is not affected by exchange rate changes. It may be the perfect fit for your clients’ retirement income capital growth needs, especially if their expenses are mainly rand based.

When you use the GAP, you can still allocate part of the remaining capital (as needed) to offshore assets. This gives your clients the opportunity to build an investment portfolio inside their Momentum Retirement Income Option that suits their personal needs and preferences. An investment portfolio with a guaranteed income for life and no restrictions on their offshore allocation.

While the allure of offshore investments is undeniable, careful deliberation is essential. By leveraging the comprehensive offerings of Momentum Wealth, clients can craft their own resilient and balanced investment strategy, with the aim to safeguard their financial well-being in retirement.