China confronts contradictions

“A land of contrasts” is probably the most tired cliché in travel writing. It also happens to be true of most countries. When it comes to economic matters, there are few places in the world today where contrasts are as noticeable as in China.

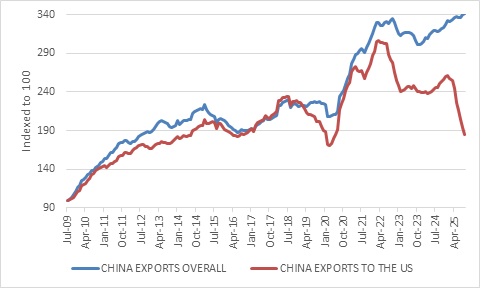

To name but a few: exports to the US have plunged in the face of steep import tariffs, yet the overall Chinese export performance is stellar. China has among the lowest interest rates among major economies, but borrowing growth is stalling. Though officially a communist country, competition in some industries is fiercer than anywhere else. Even as it astounds the rest of us with its technological capabilities, sentiment among ordinary Chinese seems depressed. In contrast to that despondent mood, Chinese equities have put in one of the strongest performances in the world this year. Despite maintaining economic growth rates South Africa can only dream of, there is consensus that a new growth model is needed. Let’s tackle these apparent contradictions and the underlying themes that unite them.

Starting with trade, tensions recently resurfaced with Beijing announcing export restrictions on rare earth elements and US President Trump threatening massive new tariffs on China, before things calmed down. Negotiations are underway again and Trump and Chinese leader Xi Jinping are still scheduled for a face-to-face meeting in Korea this week. Stepping back from this to and from, two points stand out: both countries are trying to reduce dependence on one another and increase self-reliance. And it won’t happen overnight, if ever. Each country has pain points that the other can exploit, such as the fact that China is by far the biggest source of rare earths, which are low-cost but essential ingredients for electronics, planes and defence systems. China meanwhile needs US high-end semiconductors. Ultimately, an uneasy truce is likely where the two giants continue to trade but also keep looking for alternative sources of supply and demand.

Chart 1: China export values

Source: LSEG Datastream

China is making strides in both fronts. On the demand side, its exports to other countries have more than offset lost sales to the US, though this is likely to include a fair degree of exports rerouted through other countries to avoid US tariffs.

The country continues to move up the technological ladder, including developing its own supply of homegrown semiconductors. Gone are the days of China only producing plastics, toys and textiles. Today it leads in drones, robots, solar panels and more. It became the biggest car exporter in the world in 2023, driven not by manufacturing on behalf of US, European and Japanese brands, but its own homegrown brands. Similarly, though Chinese factories still produce the iPhone on behalf of Apple, Chinese cell phone brands are growing in global reach. This is significant, since being an outsourced producer for a foreign company means basically only manufacturing jobs are created in China. On the other hand, Chinese brands like Huawei and Xiaomi employ many white-collar workers in design, engineering, marketing, finance, legal and more on top of factory jobs.

Involution

Yet, despite these achievements – and they are truly impressive – one can have too much of a good thing. In many product lines, there are too many firms, leading to excess capacity and cut-throat competition. The government calls this problem “involution” and is looking for ways to address it. Ironically, the overzealous expansion of these firms is often due to government directives in the first place, usually driven by local or regional officials. The net result is razor- thin profit margins and price cuts to eke out sales. It means the wait for dividends and bonuses by shareholders and employees respectively is very long. Eventually, there must be consolidation, and Beijing is urging this, though it will include bankruptcies and lay-offs, making it a far from a painless process. Faced with domestic oversupply, these firms also have no alternative but to look for export markets.

Click here to read more...