Central banks still in focus

Izak Odendaal, Investment Analyst at Old Mutual Wealth.

Equity markets ended the month of October strongly. It is unclear why exactly. Macroeconomic data has not given many new clues over the past month. Corporate earnings reports have been mixed but slightly better than expected. Perhaps equities were just oversold in August and September. The intentions of central banks, stated and inferred, have also played a role.

The People’s Bank of China cut interest rates

The world’s major central banks came to the fore over the last week with monetary policy decisions. The People’s Bank of China (PBOC) acted on deflationary pressures by cutting both its key lending rate and the reserve requirement ratio (RRR), the amount Reserve Banks need to hold against loans. While the recent third quarter economic growth numbers were better than expected, real growth was higher than nominal growth, pointing to falling prices. The PBOC still has plenty of room to cut lending rates and the RRR, but its challenge is to give relief to borrowers who face high real interest rates without further stoking the credit bubble that has resulted in so much wasteful investment since 2009, particularly in real estate and manufacturing.

European Central Bank thinks about cutting

In the case of the European Central Bank (ECB), it was not what was done but what was said that caught the attention. The ECB kept rates unchanged, but noted its concern that inflation might take longer to reach its 2% target, and that it would consider “all options” to push inflation back to target. Its overnight deposit rate is already at -0.2% and its main policy rate at 0.05%. The ECB is also purchasing €60 billion in bonds every month until “at least” September 2016. It could cut its deposit rate further into negative territory, expand its bond purchases or extend the programme beyond September. Inflation fell to -0.1% in October. The cue for further stimulus will be when it updates its forecasts for the December policy meeting.

Sweden’s Riksbank doesn’t count as one of the majors, but it is the oldest existing central bank. It had to reverse earlier rate hikes when it became clear thatthat inflation would turn negative. The Riksbank expanded its Quantitative Easing (QE) programme last week for the fourth time since February while keeping its main lending rate negative, partly to prevent the krone from strengthening should the ECB decide to expand its QE programme.

Leaving the door open for December

In the case of the US Federal Reserve’s Open Markets Committee, it was not what was said but what was not said that caused a market reaction. It continues to see US growth as decent (gross domestic product (GDP) growth was 2% year-on-year in the third quarter), but its September statement showed concern that weak global growth could spill over to US shores. Last week’s statement removed the comment that global economic developments “may restrain economic activity somewhat and put further downward pressure on inflation.” Again, not much has changed since the September meeting, but the equity market rally and narrowing corporate borrowing bond spreads means financial conditions have eased somewhat. Interest rates and RRR cuts in China and the likelihood of more action by the ECB will probably also have given the Federal Reserve some comfort that global economic conditions would improve.

The Fed therefore left the door open to a December hike, but it will still base its decision on data between now and then. Stability in oil markets will give greater confidence that inflation will eventually reach 2%, while the two employment reports before the next meeting will be key. The pace of jobs growth has weakened in recent months, but we are not at alarming levels yet. The Fed continues to believe that low unemployment will eventually give rise to higher inflation – a historic relationship known to economists as the Philips Curve. However, the Philips Curve relationship appears to have broken down in recent years and the debate within the Fed on its relevance appears to be heating up. Inflation has undershot the Fed’s 2% target for three years. Even excluding volatile oil and food prices, the Fed’s preferred inflation measure is 1.3%.

The one snag is that the US dollar has rallied again with the ECB hinting at further stimulus and the Fed at a rate hike. If the dollar strengthens much further it will again raise the question of whether the Fed can act, given that a stronger dollar dampens growth and reduces inflation. Rather than a slow-end to the year, December will be the key month for both the Fed and the ECB.

The Bank of Japan (BoJ) also had its monetary policy meeting last week, but did not expand its QE programme as some economists thought it might. As a percentage of GDP, BoJ QE already dwarfs the ECB’s ongoing and the Fed’s now-ended programme. So far, the BoJ has succeeded in pushing down the yen which has helped the profitability of exporters, but has not revived domestic spending.

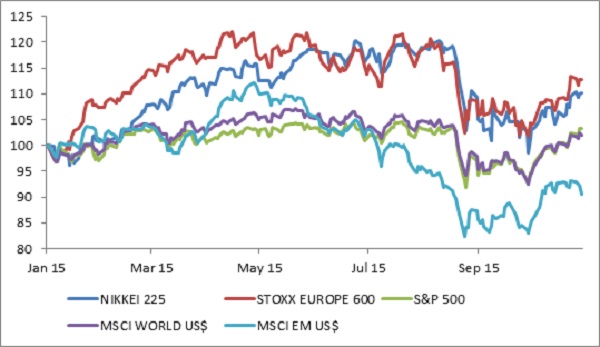

Chart 1: Major global equity indices in 2015. Local currency, rebased to 100

Source: Datastream

Not enough jobs

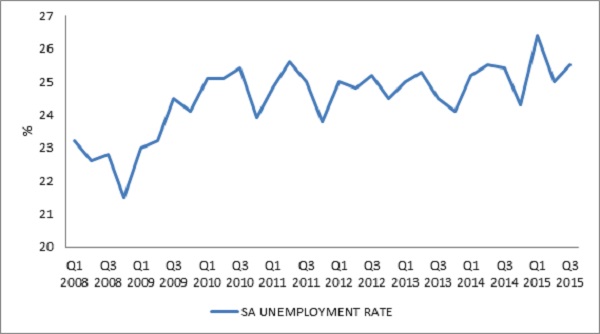

While the nation-wide student protests have shown that democracy is alive and well in South Africa, they emphasise both the long-running structural inequalities in the economy, and the general sense of unease over the current state of the local economy as shown by the latest employment numbers. Unemployment in South Africa increased to 25.5% in the third quarter according to StatsSA’s quarterly labour force survey. According to StatsSA, the economy added 171 000 jobs in the quarter, 95 000 of which in the formal sector. This is somewhat surprising, but StatsSA notes that the mining sector numbers - which were unchanged - need to be interpreted with caution. Several mining companies have announced the intention to cut jobs. The trade sector added 81 000 jobs, while the construction sector added 59 000 jobs in the quarter. However, the labour force grew by 359 000, hence the increase in the unemployment rate.

South Africa’s jobs crisis

These numbers are based on household surveys, and while the accuracy is always up for debate, StatsSA does make continual improvements. It also publishes a separate employment survey of business, which can sometimes yield different results. Nonetheless, the household survey does give the broad outline of the local employment situation. Of a total working-age population of 36 million individuals between the ages of 15 and 64, 21.2 million are counted as part of the labour force. The labour force consists of 15.9 million employed individuals, and 5.4 million unemployed people. Of the employed individuals, 10.9 million are formally employed and 2.7 million informally. 847 000 work on farms and 1.3 million in private households. Not counted as part of the labour force are 2.2 million “discouraged” individuals who were not actively looking for work in the four weeks prior to the survey. Including them in an “expanded” unemployment definition raises the unemployment rate to 34.4%. A further 12.6 million people between the ages of 15 and 64 are not economically active. These include pensioners, learners, students and prisoners.

The unemployment rate is highest for people who are young, black, female or uneducated. To be all four is to have only a small chance of having a job. The unemployment rate for 15-24 year-olds is 50%, and 30.3% for those aged between 25 and 34 years. White unemployment is 5.9%, while the unemployment rate for black Africans is 28.8%. Only 9% of whites have less than a matric, compared to 54% of black Africans. Only 5% of black Africans have a degree, compared to 27% of whites. The absorption rate (employment/ population) for graduates is double that of the population as a whole. This highlights the importance of tertiary education and partly explains the student protests over the past few weeks.

Where the money will come from to replace the planned university fee increases is still unclear. Finance Minister Nene made it clear during the recent mini-Budget that the fiscal cupboard is pretty bare, especially after the government largely used its contingency reserve (its rainy day fund) to finance above-inflation wage increases to public sector workers. At least this will provide a short-term boost to the economy. Indeed, while unemployment is high and jobs growth minimal, employed persons are still getting salary or wage increases, partly thanks to strong unions (though only 20% of workers’ salary increases are negotiated through unions, and union membership declined by 200 000 over the past four quarters). The economy-wide wage bill grew by 7.6% in the four quarters to June.

Low inflation a saving grace

The other main factor keeping the economy from falling over is that the weakness of the rand is providing support to export revenues (and other incomes linked to the exchange rate), but has not as yet stoked sustained upward pressure on prices.

Last week’s producer prices illustrate this. Producer inflation remains subdued, even as food prices are accelerating at factory level, following earlier increases at farm level. Producer inflation was 5.4% in September, but excluding food, it was 2.7%. Despite the weakening of the rand, import prices fell 6.4% in the year to August. Excluding oil, prices only rose 0.5%, pointing to downward pressures on global prices.

Low inflation, despite the currency weakness is one of the few things that are keeping the economy afloat. It means incomes are still rising in real terms, while crucially giving the Reserve Bank the room to moderate interest rate increases. Interest rates remain low by historical standards, but this has not resulted in households borrowing more. In fact, relative to income growth, households have been deleveraging and as the Reserve Bank has pointed out, cutting rates won’t do much to support the economy constrained by infrastructure bottlenecks and the commodity price slump. However, interest rate hikes could do serious damage, given the indebtedness in the economy. Further weakness in the economy could in turn lead to the government’s debt ratios deteriorating and the Minister of Finance being forced to hike taxes. Policymakers at all levels have their work cut out for them.

Chart 2: South African unemployment rate

Source: Datastream