Central banks riding the storm

There is no question that central banks have had a disproportionate impact on financial markets in recent years. This trend has only accelerated since the pandemic.

The nature of monetary policy itself has changed, including the decision-making framework and the goals. Central banks have a tendency to “fight the last war”, partly because they are conservative and bureaucratic institutions, partly because our understanding of the economy has evolved, and partly because economies themselves keep changing.

The core challenge facing monetary policy has therefore shifted several times over the decades. In the Bretton Woods era that followed World War II, economies and particularly financial systems were tightly regulated. The 1970s saw the start of a great freeing up of finance, but, almost simultaneously, also the start of a surge in inflation. Combating inflation was the main challenge of the 1980s and 1990s, and this culminated in the widespread adoption of inflation targeting, the idea being that independent central banks (many newly so) would commit to keeping inflation low.

By the early 2000s, low inflation was entrenched and central banks patted themselves on the back. However, they largely ignored the dangerous build-up of private sector debt and risk in the banking system. This left them with the task of cleaning up after the Great Financial Crisis (GFC) of 2008.

The one challenge of the post-GFC era has therefore been to ensure the resilience of the banking system, partly by introducing tighter regulations. The second challenge has been that inflation was running too low in the major developed economies. This necessitated the turn to quantitative easing and (in some cases) negative interest rates to forestall ‘Japanification’, the permanent submergence of inflation and inflation expectations.

Strange days

The challenge of the present moment is of course the global Covid-19 pandemic and its fresh deflationary impulse. Central banks acted swiftly to ensure the smooth functioning of the financial system and lower borrowing costs where they could. What they can’t do is develop a vaccine, reopen borders, and get people back into restaurants.

This is not the only challenge that some central banks are taking on. In May, the European Central Bank (ECB) launched a public consultation on how to integrate climate change risks into the scope of its work. Similar work is happening at the Bank of England. Meanwhile, the recent shift in the Federal Reserve’s policymaking framework was partly informed by the need to address rising inequality in the US.

Broadly speaking, climate change, inequality and the fracturing of the US-led rules-based global order are probably the three biggest challenges of our times (this is assuming the pandemic doesn’t worsen). However, when it comes down to it, central banks have only three tools: setting interest rates; changing the size and composition of their balance sheets through asset purchases and sales; and changing regulations in the financial systems they supervise. There is only so much they can do.

The past two weeks have seen monetary policy meetings from four of the five central banks most important to South African investors (the fifth, the People’s Bank of China does not operate according to a fixed schedule of meetings). Apart from the broad challenges referred to above, each of these banks has to contend with a different set of pressing domestic issues.

Starting with the most important of them all, the US Fed’s task was to put some flesh on the bones of the new policy framework announced recently. To briefly recap, this involves adopting a flexible average inflation target, which means it wants inflation to average 2% over an unspecified period.

Since inflation has long been below 2%, a period of inflation rising above 2% will be needed to lift the average. The Fed will also not hike interest rates at the first sign of the jobs market heating up. It has come to the conclusion that low unemployment does not result in accelerating inflation. For now, though, that would be a nice problem to have. Almost 28 million Americans were still receiving some form of unemployment benefit as of last week, compared with 2 million on the eve of the pandemic. There is clearly a way to go.

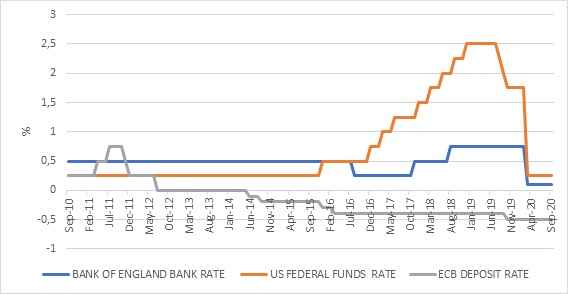

Chart 1: Policy interest rates in the US, UK and Eurozone

Source: Refinitiv Datastream

In practical terms however, the Fed’s current monetary policy stance remains unchanged. Its policy interest rate range remains at 0% to 0.25%, though it indicated that rates would likely stay there until at least 2023. It will also maintain its current pace of bond purchases of $120 billion per month. The market’s immediate response was negative. Clearly investors expected the Fed to step on the pedal. The Fed’s message, meanwhile, is that it is engaged in an endurance race, not a sprint.

Across the Atlantic, the ECB also did not change its policy stance. The deposit rate remains at -0.5%, while the €1.35 trillion bond-buying programme will continue “as long as necessary to reinforce the accommodative impact of policy rates”.

Like the Fed, the ECB also launched a review of its policy framework. It has been even less successful in meeting its inflation target in the past decade. Its more immediate worry is that a relatively strong euro will put even more downward pressure on inflation.

Another difficulty facing the ECB is that some Eurozone countries, notably Germany, have emerged from the coronavirus pandemic relatively unscathed, while the likes of Spain and Italy suffered serious damage.

A May ruling from the German Constitutional Court also cast some doubt over its ability to continue its bond-buying programme, an added complexity other central banks don’t face.

Across the English Channel, the Bank of England has not had to contend with quite the same inflation shortfall as on the Continent. Two significant bouts of pound weakness contributed to higher average inflation over the past decade. Not that inflation is currently anywhere near on target.

The bigger issue is that the rising possibility of a no-deal Brexit, a recent spike in coronavirus infections and the reintroduction of some social distancing measures means the outlook for the economy remains “unusually uncertain”. One of the steps it is taking is exploring the use of negative interest rates.

The BoE recently came under criticism from Gordon Brown for not doing enough to raise employment levels, focusing only on inflation. Brown was the Chancellor of the Exchequer in 1997 and gave the BoE independence to set interest rates.

Central bank independence

The issue of central bank independence seemed to be settled by the 1990s and the SA Reserve Bank’s operational independence was written into the 1996 Constitution in that climate. But central bank independence may one day be seen as a casualty of the pandemic. The coming years could well see the blurring of the lines between fiscal and monetary policy in some developed countries. In emerging markets, with higher rates of inflation and lower levels of policy credibility, central bank independence remains important.

The local debate about nationalising the SA Reserve Bank is a red herring. Though it is one of the last few privately owned central banks, its private shareholders have no say in monetary policy. As the ANC’s treasurer-general acknowledged last week, government has more pressing demands on its limited resources, and nationalisation has been put on the backburner.

The challenge for the SA Reserve Bank at this stage is not inflation, which is well under control. Its worry now is the prospect of a rand blow-out as investors panic over rising government debt levels. Fiscal policy is creating problems for monetary policy. Meanwhile, economic growth is constrained by structural bottlenecks such as electricity supply. Cutting interest rates cannot generate more electricity, nor can they attract more foreign tourists to South Africa.

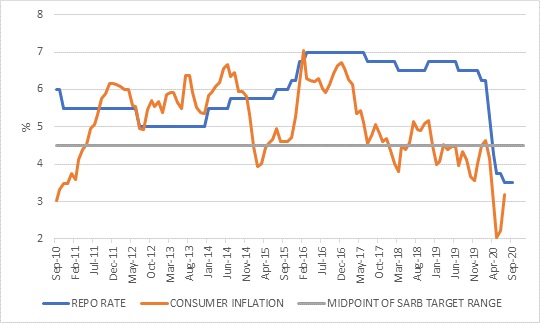

Chart 2: South Africa repo rate and inflation

This is the end

Lower interest rates still help consumer finances on the margin, however, and it is disappointing that the Monetary Policy Committee kept the repo rate unchanged last week. Though the decision was not unanimous with two of the five members voting for another cut, it appears to signal the end of the cutting cycle.

This is despite a lower growth and inflation forecast. The SARB changed its forecast for the economic contraction this year to 8.2% from 7.2% at the time of the previous meeting. The rebound next year is expected to be 3.8%, with 2.6% growth the following year. This means that the economy will not be back to its pre-pandemic size (in real terms) by the end of 2022.

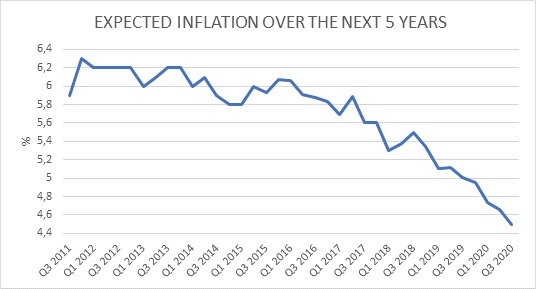

Inflation is expected to average 3.3% this year and remain below the 4.5% mid-point of the target range for the following two years. The Bureau for Economic Research’s survey data also shows a decline to 4.5% in inflation expectations over the next five years for the first time. The survey covers unions, households, analysts and businesses, so gives a broad view of how South Africans expect inflation to behave. This should be cause for celebration at the SARB, but the champagne remained firmly corked.

Chart 3: Expected inflation over the next five years

Source: Bureau for Economic Research

Take-outs

There are four broad take-outs for investors. We are clearly in a lower-for-longer global interest rate environment. This should support risk assets like equities. Central banks cannot and will not remove all volatility, so corrections can still occur, but lower interest rates create an attractive backdrop for equities.

In its latest quarterly review, the Bank for International Settlements, the central banks’ central bank argues that the drop in interest rates provided a “significant boost” to share prices in recent months. Its calculations suggest US stock prices would be 18% lower had rates remained at pre-pandemic levels. However, it also highlighted the wide dispersion of changes in equity valuation across sectors was consistent with underlying economic reality, given how unevenly Covid-19 hit different industries.

Importantly though, interest rates cannot fall much further from here, and therefore future equity returns will depend on earnings growth rebounding.

Secondly, the search for yield is also likely to extend to emerging market bonds and equities, a trend that should benefit South Africa even though we are by no means the favourite within the emerging market universe in either asset class. But a rising tide lifts even the most battered of dinghies.

Thirdly, the SARB has received a major gift from the Fed’s lower-for-longer interest rate stance. Between 2013 and late 2018, the MPC had to continuously look over its shoulder at what the Fed was doing, or planning on doing.

The SARB and other emerging market central banks have room for a few years to set policy with a greater eye on domestic considerations, without having to worry that an overly aggressive Fed could result in massive capital outflows and sharply weaker currencies. The SARB is clearly focused on fiscal risks. The MPC’s next meeting will be after the October Medium Term Budget when the path of fiscal policy will be clearer. The quicker the government tries to close the deficit, which will drain demand from the economy, the more the SARB might still be forced to cut rates.

Finally, moving up the risk curve is also something South African investors are forced to think about. The first half of the year has seen near-record inflows into money market funds, even as the repo rate fell to a record low. It will take some time for money market yields to roll down, but it is inevitable that they will. Money market returns are unlikely to beat inflation after tax, so investors will have to weigh up the stability of money markets against the prospect of declining purchasing power over time.