Catastrophe bonds offer 10% yields, uncorrelated performance in turbulent times: Stonehage Fleming

As financial markets come to terms with the uncertainty introduced by President Trump's second term in office, a specialised corner of the fixed income universe has emerged as a more predictable place for investors to ride out the storm.

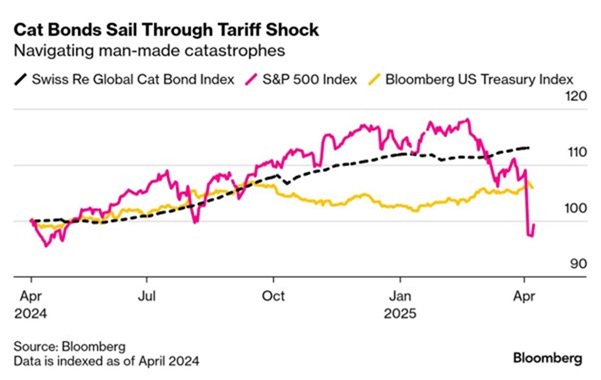

While traditional assets have experienced dramatic selloffs, these insurance-linked securities have been remarkably resilient, highlighting their value as portfolio diversifiers during periods of economic uncertainty.

The uncorrelated advantage

Catastrophe Bonds (Cat Bonds) are insurance-linked securities that allow insurers or reinsurers to transfer the risk of a large-scale disaster, such as a hurricane, earthquake, or pandemic, to investors. Investors receive an agreed yield (premium) to cover these risks.

Cat bonds are one of the few asset classes offering genuine diversification from economic variables that drive traditional equity and bond markets. Stonehage Fleming incorporates these instruments into its clients’ portfolios specifically because the drivers of risk and return for Cat Bonds are not materially tied to financial markets or the economic cycle like other financial instruments.

This fundamental characteristic has been particularly valuable during the recent market turmoil. While the S&P 500 declined roughly 15% at one point in April the Cat Bond market was unmoved, Cat Bonds gained about 0.9% through the end of May, according to the Swiss Re Global Cat Bond Performance Index. At that stage, the S&P 500 had moved sideways by May. Over the 12 months to the end of May, the contrast between returns is even more striking – Cat Bonds have delivered 13% returns compared to a 4% drop in the S&P 500 and a 5% increase in US Treasury bonds.

The diversification case is compelling: a stock market crash doesn't make hurricanes or earthquakes more likely to occur. This disconnect from traditional market forces provides investors with exposure to an entirely different risk-return profile, one dependent on natural catastrophes rather than monetary policy, geopolitical tensions, or corporate earnings cycles.

A fast-growing market

The catastrophe bond market has reached what industry experts describe as an "inflection point." Fermat Capital Management, a specialised hedge fund in this space, predicts 20% growth in 2025, with the market expected to reach some $60 billion by year-end. This expansion reflects not just institutional appetite but also increasing accessibility for retail investors through UCITS funds and the world's first catastrophe bond ETF.

The numbers support this momentum. Catastrophe bond issuance has already surpassed $15 billion in 2025, breaking all previous records with still months remaining in the year. May alone saw nearly $6 billion in new issuance – the largest single month in the market's history. This explosive growth has propelled the outstanding market to over $57 billion, representing a 15.5% increase since the end of 2024.

.jpg)

Source: Artemis.bm Deal Directory

Climate change: the investment risks and opportunities

The expansion of the catastrophe bond market coincides with an increasingly volatile climate landscape. Recent years have witnessed five consecutive years of global insured losses exceeding $100 billion from natural catastrophes, according to Barclays Private Bank, with 2024 marking another active year for weather-related risks globally. Hurricane Beryl became the earliest-forming Category 5 storm on record, while severe convective storms across the US accumulated over $50 billion in insured losses.

However, sophisticated modelling techniques have evolved alongside these challenges. Modern catastrophe loss models, which originated in the late 1980s, now integrate climate change projections and can provide more sophisticated risk assessments, enabling the precise pricing of what were once considered unquantifiable risks. These models combine statistical analysis with physical modelling to create synthetic event sets representing thousands of years of realistic scenarios, for example quantifying the Florida Hurricane risk.

This scientific approach has yielded impressive results. The catastrophe bond market has generated positive returns in all but one year since the start of the century, demonstrating its ability to accurately price and manage natural disaster risk even as the frequency and severity of events have increased.

An inflation hedge in uncertain times

John Seo of Fermat Capital identifies inflation as a key driver of catastrophe bond market growth, noting that rebuilding costs have increased substantially in both Europe and the US. Seo says this inflationary pressure has increased underlying risk exposure by 50% in nominal dollars over the past five years, creating a greater demand for risk transfer mechanisms.

For investors, this dynamic creates a compelling value proposition. Cat Bond yields consist of two components: a risk premium plus the US Treasury rate. With Trump's tariff policies generally considered inflationary, Treasury rates are expected to remain elevated in the medium term, potentially boosting catastrophe bond yields.

Portfolio diversification during market crises

The recent market volatility has provided a real-time demonstration of the benefits of Cat Bonds for portfolios. As Plenum Investments notes, these securities are "currently impressively demonstrating their stabilising effect in portfolios – just as they did during the financial crisis, the Covid shock, and the interest-rate turmoil of 2022."

Stonehage Fleming continues to allocate to Cat Bonds specifically to complement traditional asset classes and generate differentiated returns over time. Our strategy recognises that while declines in market value should be expected during specific catastrophic events, the combination of attractive income compensation and diversification properties supports a constructive long-term outlook.

Looking forward

The regulatory environment continues to support the growth of the catastrophe bond market. The European Central Bank and European Insurance and Occupational Pensions Authority have called for increased use of these instruments in the EU, where only about 25% of climate-related catastrophe losses are currently insured. The UK's Prudential Regulation Authority has proposed cutting approval times for insurance special purpose vehicles to accelerate market development.

Current market conditions – featuring elevated Treasury rates, strong demand for reinsurance, and reduced traditional reinsurance capacity – create a favourable backdrop for catastrophe bond performance. According to Artemis, the Cat Bond Market Yield has risen to 10.43%, as of end-December 2024, reflecting strong demand and seasonal effects, while providing attractive income compensation for investors willing to accept natural disaster risk.