Cash trending towards trash

During the mid to late 2000s and then more recently from January 2015 to date, South African investors could invest in the money market and earn an attractive real return with little risk to their capital.

The more recent period of positive real money market returns coincided with a period of disappointing returns from growth assets (equities and property), with the result that more and more investors switched their growth asset exposure to cash. This action has only accelerated post the recent equity market collapse.

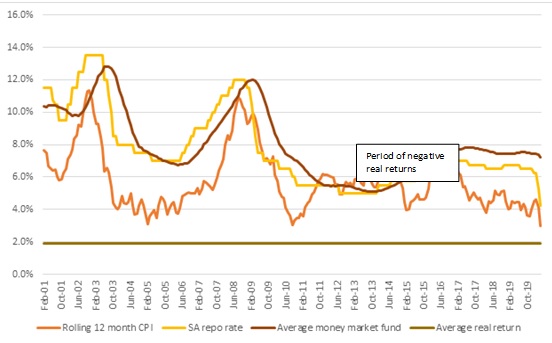

Figure 1: South African inflation, interest rates and money market returns

Source: Ninety One Benchmark database

Some observations:

• It is evident that the SA repurchase (“repo”) rate is the key monetary policy tool used by the South African Reserve Bank (SARB) to control inflation.

o As inflation rises (or is predicted to), so the SARB responds by increasing the repo rate, and as inflation falls (again, or is predicted to) so the SARB responds by cutting the repo rate.

• As the repo rate rises, so returns from money market investments also rise, and vice versa. Note that the average money market fund return lags that of the repo rate.

o Importantly, the most recent 250 basis point cut in the repo rate is yet to reflect in the performance of the average money market fund. This means that money market returns will fall from here.

• The average money market fund return peaks where the repo rate peaks and bottoms where the repo rate bottoms.

o We can therefore expect annualized money market fund returns to trend down towards the current repo rate of 3.75%.

• Over the full period for which the SARB has implemented inflation targeting, the money market has delivered an average real return of 1.9%.

It is instructive to consider what happened in the period post the Global Financial Crisis (GFC), which introduced a lengthy period (approximately 5 years) of negative real returns for money market fund investors. Could it serve as a warning for the likely path of real money market fund returns? We think so.

To re-stimulate economies post the GFC, central banks around the world, including the SARB, anchored interest rates at record low levels. In the subsequent years, money market returns fell to levels where investors were guaranteed negative real returns, encompassing the first half of the last decade. This was because policy makers were more concerned about stimulating economic growth at the expense of wanting to contain inflation, which interestingly never materialised.

And now history is repeating itself. In response to the devasting consequences of COVID-19, Central banks around the world are once again responding by cutting interest rates to record lows (in some countries interest rates are at zero or negative). The Monetary Policy Committee (MPC) of the South African Reserve Bank has acted similarly, by announcing two 100 basis points cuts and a 50-basis point cut in the repo rate in the recent past. These actions have reduced the repo rate to 3.75%. They were also the first moves of more than 25 basis points by the MPC in many years, illustrating the seriousness with which they view the current crisis.

Given what we have observed above, we can expect the average money market fund return to trend towards 3.75%.

Deciding what matters most

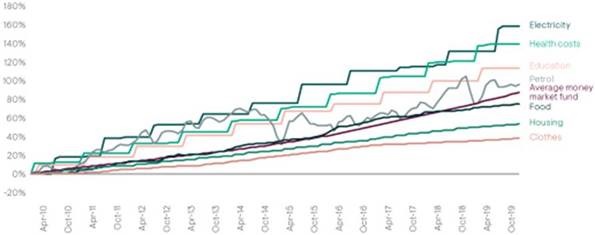

This will mean that financial advisors and investors will need to look beyond the perceived safety of money market funds to deliver attractive real returns. I say “perceived safety” because cash will increasingly prove to be a poor investment in preserving the purchasing power of your money over the longer term. Over the last 10 years many components of inflation (electricity, health costs, education and petrol) have increased by more than the return achieved by the average money market fund. So, anyone invested in the average money market fund would have been spending a greater portion of their income on these necessities, which they would have had to subsidise from other sources (if possible) as their money market fund investment has not kept pace with these increases.

Figure 2: Hiding in cash does not protect you from inflation over the longer term

However, conservative investors will face a dilemma, as higher real returns will come at a price, including capital security and recommended investment term. Investors must therefore satisfy themselves that the trade-off is worthwhile.

Conservative investors with an investment time horizon of greater than a year could consider a fund where the portfolio managers have a far broader investment universe from which to choose, such as the Ninety One Diversified Income Fund. It means they can diversify risk while potentially earning returns in excess of money market rates – in essence, seek to generate real returns (participate) while managing downside risk (protect).

To date the Fund has:

• Provided a consistent total return in excess of cash / inflation over time, with some correlation to the bond market when the bond market outperforms cash, and little to negative correlation to the bond market when it underperforms. Since the Fund’s inception in 2008 it has outperformed the average money market fund by approximately 2% per annum

• Avoided quarterly drawdowns and eliminated 6-monthly drawdowns completely. In what proved to be the most difficult quarter in many years, the Ninety One Diversified Income Fund was one of the very few flexible fixed income funds that delivered a positive return over the quarter, further validating the Fund’s unique “participate and protect” structure.